A Theory of Information Overload Simon P. Anderson and André de Palma∗ January 2005 PRELIMINARY AND INCOMPLETE - COMMENTS WELCOME

Abstract Advertising must compete for the attention of prospective consumers, and attention is a scarce resource. "Junk" mail, "spam" e-mail, telemarketing ’phone calls, and advertising messages generally have the common feature that both sides of the market (advertisers and prospective customers) need to apply effort to generate a transaction. Message recipients supply attention according to expected consumer surplus, which depends on the average benefits across messages received. Senders are motivated by expected profits. The equilibrium number of messages transmitted depends on the profit of the marginal firm along with the communication probability induced from the receiver attention decision. In equilibrium, the wrong messages may be sent, or too many may be sent. A higher cost of message transmission may improve message quality and raise the number of messages examined and the optimal message rate reflects this. Endogenizing the number of messages per sender causes another "lottery ticket" dimension for profit dissipation. Product class competition also dissipates rents. An opt-out option (e.g. the Federal Do-Not-Call list) is better than an outright ban, but too many individuals opt out. Jel Classification: D11, D60, L13. Keywords: information overload, congestion, advertising, common property resource, overfishing, lottery, two-sided markets, junk mail, email, telemarketing, Do Not Call List, message pricing.

∗ Simon P. Anderson: Department of Economics, University of Virginia, PO Box 400182, Charlottesville VA 22904-4128, USA,

[email protected]. André de Palma: Senior Member of the Institut Universitaire de France, ThEMA, Université de Cergy-Pontoise, 33 Bd. du Port, 95011, Cergy Cedex, FRANCE.

[email protected]; Institut Universitaire de France. The first author gratefully acknowledges research funding from the NSF under grant SES-0137001. We thank seminar participants at Cincinatti and the European Institute in Florence, and conference participants at EARIE 2004 (Berlin), and the 2004 Chinese IO Society meeting (Beijing).

1

1

Introduction

One in every six pieces of mail sent in the world is US “junk” mail. This adds up to a tree’s worth of paper per US household. The rate charged by the US post office for bulk mailing is 8.8 cents per item, way below the current rate of 37 cents for first class mail.1 Nations are still looking for an appropriate way to deal with “spam” (junk email).2 A spammer can send 650,000 messages in an hour, at virtually no cost: spam filters cause people to lose possibly important messages, or even valid commercial offers that they might have taken up had they not been lost in a swamp of other propositions. Telemarketing (junk telephone calling) in the US has seen a dramatic decline since the recent advent of the FTC-sponsored Do-Not-Call list. More generally, people see thousands of advertising messages a day. An average of one message is remembered. Advertising technology (for unsolicited advertising) is therefore characterized by a huge degree of congestion in the competition for a consumer’s attention. The purpose of this research is to consider the economics of such unsolicited advertising.3 The model builds on two strands of research. The first is the model of parking in Anderson and de Palma (2003), which treats parking as a common property problem. A novel feature of the analysis is to treat multiple locations prone to congestion; locations are ranked by intrinsic quality (closeness to the CBD). The common property problem is greatest at locations of highest quality. The analogue is that advertisers must compete for the consumer’s attention by sending them messages. The quality aspect is that consumers differ by how responsive they are to advertisements. The second research antecedent is work by Anderson and Coate (2004) on advertising-financed media, which contributes to the nascent literature on "two-sided" markets with bilateral network externalities. The message transmission (advertising) side of the model is drawn from here. We consider two groups of economic agents, senders and receivers of messages. For concreteness here, think of them as firms and consumers. On the one side, the firms need to communicate their wares. They do so by sending messages (bulk mail, etc.) to prospective consumers on the other side. Firms (message senders) differ by the profitability conditional on reaching potential 1 This lowest rate applies to non-profit organizations. The rate is up to 7 cents higher for private firms. For USPS rate information, see http://pe.usps.gov/text/dmm/R600.htm#Xgc81619 2 The term spam comes from an early anecdote in the annals of computer geekdom. Someone sent his friends a message which contained just the word "spam" (after the Monty Python Flying Circus song) repeated hundreds of times: htpp://www.templetons.com/brad/spamterm.html describes the "origin of the term spam to mean net abuse". Spam can be around 55% of email, or even rise to 80%: see http://www.eprivacygroup.com/pdfs/SpamByTheNumbers.pdf See also: http://cobb.com/spam/numbers.html 3 Of course, other advertising is unsolicited: think of billboards and radio/television for examples. Classified ads, and ads in specialist magazines, may be more sought after. TV ads finance the programs they run on, and so are bundled commodities. The distinguishing feature we consider is the crowding of attention. This arguably applies to billboards and TV ads too.

2

consumers (message receivers). Sending messages is costly. To communicate successfully with a consumer, the firm must first send the consumer the message and then she must examine the message (open the particular mail containing the advertisement, for example). Both sides of the market need to exert effort to arrive at transactions. Clearly, firms with higher profitability have a larger benefit from sending ads. We can then find a critical sender type such that all superior sender types send messages to receivers, while all other potential senders do not. In equilibrium the cost of sending a message should equal the expected benefit for the marginal sender type. This process leads to three types of outcome: recipients receive more messages than they examine, they examine all messages received, or they receive no messages (although they would examine everything they got if they got any!)4 We also deal with the consumer choice of how many messages to examine (envelopes to open, say). This issue is an important feature of the junk message phenomenon because it explicitly treats the joint input nature of information production. Specifically, both receiver inputs and sender inputs are needed in order for a sale to be made. The sender must send the message at some cost and the receiver must examine it (open the envelope and process the information therein), also at some cost. The interesting economics of this market interaction are that the number of messages sent depends on expected profit of the marginal sender, which in turn depends on the number of messages read by the receiver. However, the number of messages the receiver examines depends on the benefit that the receiver expects, which in turn depends on the composition in terms of average quality of the messages sent. In this regard, we shall see below that a higher cost of sending messages will increase the number of messages examined because the expected quality rises. Consider the effects of raising the costs of sending messages. If the recipients are examining all messages received, they will receive fewer messages. There is a social loss on this account due to a reduction in socially beneficial transactions. However, if receivers do not examine all messages, they continue to receive messages now receive better quality messages in the sense that the average quality they receive increases.5 This is a source of welfare improvement. The outline of the paper is as follows. The next section gives the background in terms of the behavior of the agents on the two sides of the potential transaction. Section 3 characterizes the optimum. Section 4 derives the building blocks of the equilibrium analysis, namely the sender transmission function and the receiver examination function. Section 5 puts these together to derive equilibrium behavior. Section 6 then provides welfare analysis and finds conditions under which the optimum can be decentralized through choice of the transmission price. Section 7 allows for intrinsic nuisance costs and looks at the 4 A similar situation occurs for referee reports: some only respond to some requests, others do all they are asked, and some would do them but are never asked. 5 A similar finding (though in the opposite direction) arises in Engers and Gans (1998): paying referees is not as effective as might be thought since referees may be more likely to refuse knowing that other referees are induced by payments.

3

possibility of receivers opting out completely (for example, the federal Do Not Call list in the US), and the pros and cons of outright bans. Section 8 allows senders to transmit more than one message, while section 9 addresses the solution chosen by a monopoly information gatekeeper. Section 10 discusses the effects of allowing for competition between senders in the product market, and section 11 concludes.

2

Congestible information

In order for a (mutually beneficial) transaction to be consummated, information must be transmitted by a sender, and the receiver must both process it and react positively (by purchasing an advertised good, say, or joining a club). In this case, a successful transaction occurs. The size of the conditional surpluses to each party (following a positively processed message) depends only on the sender type. We suppose that there is a single receiver and a continuum of senders. Initially, we assume that each sender can send at most one message to the receiver. The basic idea of the model is the following. Senders transmit costly messages that may result in positive profits if the receiver is aware of the opportunity communicated in the message. That is, the receiver needs to examine the message and wish to act on it. Senders have different expected profits from communicating with the receiver. For example, senders may have different mark-ups, and/or the probability that the receiver is interested in buying a product may differ across products. The receiver chooses how many messages to examine, bearing in mind the average expected surplus from a message. Congestion arises when the receiver chooses not to examine all the messages received. Even though congestion is not optimal at the first best solution, it may arise in equilibrium because a sender may transmit a message that is not examined with certainty if it has a high enough profitability if examined. The expected receiver surplus from any particular message can reflect the probability of buying (being interested in an advertised product), as well as different conditional surpluses from buying, as noted above. Expected surpluses are assumed independent across messages. This means that there is no "business stealing", so that messages are only in competition with each other insofar as they compete for a receiver’s attention in examining them. Thus, the senders decide whether or not to send a message, and the receiver decides how many of the messages received to examine. In the junk mail context, households decide how many letters to examine. For telemarketing calls, they decide how often to answer the telephone. For spam e-mail, recipients determine how much mail to read (or perhaps, how tight to set the spam filter setting). The equilibrium concept requires agents on each side of the market to rationally anticipate the actions of those on the other side. In equilibrium, senders know how many messages receivers will examine, and the receiver knows the number and distribution of types of senders’ messages received.

4

2.1

Information senders

There is a mass of senders of size M . As noted above, for the moment we assume that at most one message can be sent by each sender to the receiver. This assumption will be relaxed below. We order the sender types by θ ∈ [0, 1] such that higher θ implies higher conditional expected sender benefits. The distribution of sender types is denoted by F (θ), with associated density f (.) > 0. Let π (θ) denote the conditional expected sender benefit from the match with the receiver. Assumption 1: π (θ) ≥ 0 is strictly increasing and continuous in θ. We assume the profit function is strictly increasing in θ in order to avoid dealing with ties: nothing really rides on this except for simplicity of presentation. We assume that the unit cost to a sender for transmitting a message is constant and denoted by γ, and throughout the relevant range of values that γ may take, we assume the following. Assumption 2: π (0) < γ < π (1). We make this assumption to avoid a couple of rather trivial cases. If γ ≥ π (1), no sender will serve the market, while if γ < π (0) all senders will serve the market if the receiver examines a large enough number of messages (so each message has a high enough probability of being examined). This latter part of Assumption 2 will also imply that there are always some senders "waiting in the wings" in equilibrium: not all transmission options are exhausted.6 Assumption 1 implies that we seek allocations at which all senders above a critical threshold are transmitting. The threshold is denoted θ∗ . In such cases, the number of messages sent is the same as the number of active senders, and is denoted n (θ∗ ) = M [1 − F (θ∗ )].

2.2

The information receiver

Let s (θ) denote the conditional receiver expected benefit (or surplus), conditional on the receiver examining the message. Thus, s (θ) allows for the probability that the receiver wishes to act upon the message (buy the advertised good, say) or not, and that sender types may entail different probabilities that the receiver is interested and/or different surpluses when interested. Any product pricing information is included in the message. Assumption 3: s (θ) ≥ 0 is continuous in θ. Clearly the expected surplus should be non-negative since the receiver always has the option of ignoring the information received. In the sequel, we shall make more specific assumptions about the function s (θ). On the receiver side, suppose that it costs the receiver C (φ) to examine φ messages. 6 For what follows we could equally well suppose that π (0) = 0 to reflect the idea that there are many potential opportunities running the gamut from positive through negative profitability, and we can clearly censor those with negative profits.

5

Assumption 4: C (.) is a twice continuously differentiable, non-negative, increasing, and strictly convex function. If the receiver chooses not to examine all the messages received, then each is equally likely to be examined. If n messages are received, from which φ are examined, with φ ≤ n, then the probability that the receiver examines any one is φ/n ≤ 1. Examination is a necessary precursor to a consummated message (a sale).

2.3

Market clearing

In order to address welfare issues, we denote by b (θ) the expected social benefit (or gross expected social surplus) of a message that is transmitted and processed with b (θ) = s (θ)+π (θ). An unsuccessful message is not processed and therefore has zero social benefit. We use the following technical assumption to avoid unnecessary ties: Assumption 5: The expected social benefit of a successfully transmitted message, b (θ) = s (θ) + π (θ), is only constant on a non-measurable set.

3

First-best optimal allocation

The first-best optimal allocation is a description of the θ-types that transmit messages, and the mass of messages that receivers examine. As noted above, the expected gross social surplus b (θ) of a message sent by a sender of type θ and examined by the receiver is b (θ) = s (θ) + π (θ). Let Ψ (y) be the measure of senders who generate a social benefit (joint gross surplus of the two sides of the market) b (θ) of at least y, with y ∈ [0, bmax ], where bmax = max [b (θ)]. Thus Ψ (bmax ) = 0 and Ψ (0) = M . By construction, θ

Ψ (y) is strictly decreasing in y. By Assumption 5, Ψ (y) is continuous. We further assume: Assumption 6: Ψ (y) is differentiable. Note for example that this assumption is satisfied if b (θ) is differentiable and quasi-concave in θ. At the first-best optimum, all messages sent should be examined (otherwise, examination costs can be reduced) and the only messages that are sent and examined are those that yield benefit at least as large as the social marginal cost. The latter comprises marginal transmission cost, denoted by γ¯ , plus examination cost, C 0 (Ψ (y)). At the optimum, this marginal cost equals the marginal benefit, y o . The optimal level of this marginal benefit solves: γ¯ + C 0 (Ψ (y o )) = y o .

(1)

The first-best optimum is characterized as follows. Proposition 1 There is a unique first-best optimum allocation. If γ¯ + C 0 (0) ≥ bmax , no messages are sent. If γ¯ + C 0 (0) < bmax , all messages with b (θ) ≥ y o are sent and examined, where y o solves γ¯ + C 0 (Ψ (y o )) = y o . 6

Proof. Refer to (1) and first note that the left-hand side, γ¯ + C 0 (Ψ (y)), is decreasing in y since C” (.) > 0 (by A4) and Ψ0 (.) < 0. We also know that γ¯ + C 0 (Ψ(0)) = γ¯ + C 0 (M ) > 0. If γ¯ + C 0 (Ψ(bmax )) = γ¯ + C 0 (0)≥ bmax then no messages are examined.since the least costly message (i.e., the first message that is sent) costs no less than the maximal benefit. If γ¯ + C 0 (0) < bmax , by monotonicity of C 0 (Ψ (y)), there exists a unique interior solution y o to (1), and all messages sent are examined. As we shall see below, equilibrium will often be characterized by congestion of messages (not all messages sent are examined), which is clearly inefficient. A further characterization of the first-best optimum is possible when b (.) is monotonic. Corollary 1 h Let bi(.) be increasing and γ¯ + C 0 (0) < b (1). Then all messages with type θ ∈ θh , 1 are sent, where θh ∈ [0, 1] solves ³ h ³ ´i´ ³ ´ = b θh . γ¯ + C 0 M 1 − F θh

Let hb (.) ibe decreasing and γ¯ + C 0 (0) < b (0). Then all messages with type θ ∈ 0, θl are sent, where θl ∈ [0, 1] solves ³ ³ ´´ ³ ´ = b θl . γ¯ + C 0 M F θl

The corollary indicates that all messages above a critical threshold ought to be sent if b is increasing.7 Since π is increasing, then (as we shall see) the equilibrium also entails senders transmitting above a threshold value. However, the market typically will not provide the socially optimal level of messages. If, though, b is decreasing, then the optimum stipulates that all messages below a threshold will be sent. The market cannot deliver this configuration since senders sort according to the profitability of the messages which is instead increasing in θ and so involves all the sender types above a threshold level. In this case, not only may there be too many senders, but they also may be the wrong ones.

4

Equilibrium conditions

Senders take the number of messages, φ, examined by the receiver as given. In sub-section 4.1 we look at the mass of messages sent and the associated sender types as a function of φ. As we show, this yields a threshold value, θ∗ , such that all higher θ’s transmit, with an associated mass of messages sent. The number of messages sent, as a function of φ, is the sender transmission function (or transmission function, for short), which is denoted N (φ). Since only the highest profit messages are sent in equilibrium, N (φ) is a sufficient statistic for describing the threshold message, θ∗ . 7 If

b (0) < γ ¯ + C 0 (M), then θh ∈ (0, 1).

7

Similarly, on the other side of the market, the receiver takes the mass and composition of the messages sent as given. In sub-section 4.2 we determine the examination condition (choice of φ) as a function of the number of messages sent, n (where it is also understood that they are the highest profit ones). This yields the receiver examination function (or reception function, for short), which is denoted Φ (n). Equilibrium is then a market clearing (or consistency) condition that the agents on each side rationally and correctly anticipate the actions of the agents on the other side of the market. This is simply the intersection of the sender transmission and receiver examination functions. Thus, an equilibrium will be described by a pair (φe , ne ) such that N (φe ) = ne and Φ (ne ) = φe .

4.1

Information senders

The sender transmission function, N (φ), describes the number of messages sent as a function of the receiver examination level, φ. Senders maximize profits for a given receiver examination level. Assumption 1 (that the ranking of π is strictly increasing) leads to a preliminary characterization of a sender transmission function: Lemma 1 For any given φ, all sender types θ above a threshold θ∗ send messages. Proof. Suppose instead that the support of the messages sent is not the interval from a critical θ to 1. Indeed, suppose there exists some positive measure of senders with θ ∈ [θ3 , θ4 ] that do not send messages, and another positive measure of senders with θ ∈ [θ1 , θ2 ] that do send messages, with θ2 ≤ θ3 . Let the mass of messages sent at the purported sender transmission relation be n. Then, for all θ ∈ (θ1 , θ2 ), it must be that nφ π(θ) > γ. However, π (θ) is strictly higher for all θ ∈ [θ3 , θ4 ] than for any θ ∈ (θ1 , θ2 ). Therefore there exists some positive measure, µ, of senders from the interval [θ3 , θ4 ] that can transmit φ messages and earn profits n+µ π (θ) > γ. This latter statement contradicts the starting position that excludes senders in [θ3 , θ4 ]. Lemma 1 indicates that the most profitable senders are active, so the messages sent are those in [θ∗ , 1]. Higher profit senders crowd out lower profit ones. The threshold θ∗ induces a mass of messages n = M [1 − F (θ∗ )], so there is an inverse and monotonic relation between θ∗ and n since we assumed F (θ) is strictly increasing. Lemma 2 There is a one-to-one between the mass of messages sent, ¡ relation ¢ ∗ n −1 , and dθ n and the threshold, θ∗ = F −1 1 − M dn = Mf (θ∗ ) < 0.

dn Proof. This follows directly from Lemma 1, since n = M [1 − F (θ∗ )], so dθ ∗ = ∗ −M f (θ ). Q.E.D. In the sequel, for notational convenience we shall not explicitly denote the functional dependence of θ∗ on n. However, this relation be recalled ¡shouldn ¢¢ ¡ , etc. whenever a θ∗ is encountered: for example, π (θ∗ ) = π F −1 1 − M

8

The sender transmission function N (φ) maps values of φ into numbers of senders transmitting, n. Any value of φ is interpreted as a number of messages that will be examined if available. Thus if the value of φ exceeds (or equals) the actual number of messages sent, n, the probability is one that a message sent is examined. Conversely, for φ < n, the probability that a sent message is examined is φ/n < 1. Since π (0) < γ < π (1) (by Assumption 2), the least profitable sender earns zero profit, and so N (φ) is implicitly defined by n the fact o that least profitable φ sender that transmits makes zero profit, i.e., min n , 1 π (θ∗ ) = γ. Note that all messages sent (and received) are examined (i.e. N (φ) = φ) when γ = π (θ∗ ) min or, hequivalently, = π −1 (γ) or nmax = ´iwhen the threshold value satisfies θ ³ min c max = φ . Thus N (φ) = n M 1−F θ for φ ≥ φc . Thus θmin is the lowest possible threshold for θ∗ and is attained when a large enough number of messages is examined that each message sent is examined. Then the profit on the marginal message just equals the transmission cost, γ. The corresponding mass of messages sent is nmax . For φ ≤ φc , the sender transmission function is given implicitly by N (φ) =

φ π (θ∗ ) , γ

(2)

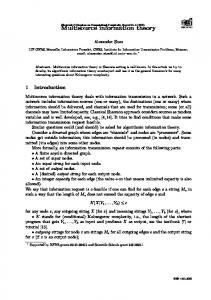

or, in inverse form, φ = γ π(θn∗ ) . The transmission function is sketched in Figure 1, in (φ, n) space. INSERT FIGURE 1. The Sender Transmission Function N (φ) . The properties of the sender transmission function, N (φ), are described in the next Proposition. Proposition 2 The sender transmission function is given by ½ ¾ φ N (φ) = min , 1 π (θ∗ ) = γ. n The sender transmission function and increasing over the domain ´i h ³is continuous φ ∈ [0, φc ] where φc = M 1 − F θmin = nmax and θmin = π−1 (γ). On this domain, the inverse of N (φ) is φ = γ π(θn∗ ) . For φ ≥ φc , N (φ) = nmax . Then N (φ) > φ for n ∈ (0, φc ), and N (φ) = φ for φ ∈ {0, φc }. Proof. It remains to prove that N (φ) is increasing over the domain φ ∈ [0, φc ], that N (φ) > φ for n ∈ (0, φc ), and that N (φ) = φ for φ ∈ {0, φc }. First note that N (φ) is given by (2) for φ ∈ [0, φc ]. The first property then follows simply from writing (2) in inverse form as φ = γ π(θn∗ ) and then noting the RHS is

9

increasing in n (the denominator is decreasing since π (.) is increasing in θ∗ and θ∗ is decreasing in n). To prove the second, note that for φ ∈ (0, φc ), γ=

¢ φ φ φ ¡ π (θ∗ ) > π π −1 (γ) = γ, n n n

where we recall that π −1 (γ) = θmin . The third property follows from setting the solution on the LHS of (2) as N (φ) = φ. One solution is φ = 0; the other has γ = π (θ∗ ), which defines θmin (and hence nmax and φc ). Q.E.D. In summary, the sender transmission function is increasing from (0, 0) to (nc , φmax ). Receivers do not examine all messages received except at the end points where either no messages or else the maximum number of messages nc are sent. The sender transmission relationship N (φ) is thus a number of messages sent that increases with the number of messages examined. In that sense it is like a supply relation, although one that depends on the quantity demanded. Equivalently, there is a critical sender type, θ∗ , that is decreasing in the number of messages examined by the receiver. There is no consistent solution where receivers examine more messages than senders want to transmit. The important economic problem on this side of the market is the common property problem. The receiver’s attention is "over-fished" by the sender. As we just showed, for only two levels of φ do the senders respond by sending exactly the number of messages that the receiver examines - and one of these is the zero level! At all other feasible levels, the senders are creating information congestion by sending more messages than the receiver examines. We now need to determine receiver behavior.

4.2

The information receiver

The receiver faces the decision of how many messages to examine given the profile of messages received. Lemma 1 implies that only the highest θ-types transmit, so if the critical θ value is θ∗ , the number of messages sent is n = M [1 − F (θ∗ )]. Since n is inversely related to θ∗ , we shall analyze the receiver examination function, which is denoted Φ (n), by determining the receiver’s actions (choice of how many messages to examine, φ) as a function of θ∗ . Each time an expression involves θ∗ , the reader should remember that this is a decreasing function of n. The receiver’s calculus depends on the benefits she expects to get, and the cost of examination. Given she cannot tell a priori which messages contain which offers, she examines them at random.8 If all senders with θ ≥ θ∗ are transmitting, the average expected surplus per message scrutinized by the receiver is9 : Z 1 f (θ) s (θ) sav (θ∗ ) = dθ. (3) ∗ 1 − F (θ∗ ) θ

8 In the sequel, we allow for different media, that may differ by transmission cost. The fact that the sender has paid a higher price provides information before the letter is opened. A related example concerns two types of letter (with different postage costs, like registered and bulk mail). 9 Here s (θ) is the expected surplus from a message from sender θ.

10

The integral term is the expected surplus per message examined from the total set of messages received, where f (θ) / (1 − F (θ∗ )) is the density of message types conditional on the set of messages sent by senders in [θ∗ , 1]. If the receiver examines φ ≤ n messages, her expected benefits are then ½ if φ < n φ sav (θ∗ ) S (φ; n) = , n sav (θ∗ ) if φ = n which is the number of messages examined times average expected surplus. The cost of examining φ messages is given by C(φ), where C (.) is increasing, strictly convex, and twice continuously differentiable (by Assumption 4). The receiver’s problem is then max {S (φ; n) − C(φ)} .

φ∈[0,n]

The solution to this problem yields the receiver examination function, Φ (n). If sav (θ∗ ) ≤ C 0 (0), no messages are examined, so the receiver’s solution is to set Φ (n) = 0. If some but not all messages are examined, 0 < φ < n, the first-order condition is sav (θ∗ ) = C 0 (φ), where the LHS is simply the average surplus over the messages received. This is an important principle in the problem: average benefit equals marginal cost on the sender side if the sender is at an interior solution of not examining all messages received. Otherwise (if sav (θ∗ ) > C 0 (n)) the receiver is supply constrained in the sense that she would examine more messages if she received them, and Φ (n) = n. To summarize: Proposition 3 The receiver examination function Φ (n) is given by © ª Φ (n) = min n, C 0−1 (sav (θ∗ )) ¡ ¢ n . It is a strictly increasing function of n if sav (θ∗ ) is where θ∗ = F −1 1 − M ∗ strictly decreasing in θ .

Proof. The last statement follows directly since θ∗ is decreasing in n and C 0 (.) is an increasing function. Q.E.D. Consider first the simple case when s (θ) = s¯ (so s (θ) is constant at level s¯). This means that for any given θ∗ , the surplus per message examined is the same, up to an examination level equal to the number of messages sent. The resulting receiver examination function is given in Figure 2. INSERT FIGURE 2. Receiver Examination Function Φ (n) when s (θ) = s¯. The optimal examination decision is simply described as a value for φ equal to C 0−1 (¯ s) as long as this level is below n, and n otherwise. That is, the receiver’s examination choice is (see Figure 2): ½ 0−1 (¯ s) if n > C 0−1 (¯ s) C Φ (n) = . n if n ≤ C 0−1 (¯ s) 11

Hence the receiver’s response is to examine a constant number of messages: when θ is so high that this number is no longer attainable, the receiver examines as many messages as possible, which is the number sent. The response curve therefore follows the constraint φ = n for high enough θ (i.e., for low enough n ≤ C 0−1 (¯ s)). The case of non-constant s is described in more detail in the equilibrium section below.

5 5.1

Equilibrium configurations Equilibrium with constant receiver benefits

We first determine the full equilibrium to the model when s (θ) is constant. As previously noted, there is always the trivial equilibrium at which no messages are sent and none are examined. Otherwise (see Figure 3), there is one other equilibrium, and in the sequel we discuss that equilibrium at the intersection of the Sender Transmission Function and the Receiver Examination Function. Depending on parameter values, either all messages are examined, or else only a subset of those sent are. Three cases are illustrated in Figure 3.

INSERT FIGURE 3. Equilibrium with constant receiver surplus, s¯. The first case, with Sender Transmission Function STF1 and high γ, involves all messages examined, and receivers would be willing to examine more if more were sent. However, the senders wish to send no more even though they are examined with probability one. In the second case, with Sender Transmission Function STF2 and intermediate γ, senders examine all messages, but would not examine more if more were sent. Again, the senders wish to send no more even c though they are examined ³ with probability one. This ³case arises ´ ´´ φ2 and ³ when = γ 2 , and φc2 = M 1 − F θmin = nmax θmin satisfy C 0 (φc2 ) = s¯, π θmin . 2 2 2 2 ³ ´´ ³ 0−1 Hence γ 2 is defined by γ 2 = π F −1 1 − C M (¯s) . In the third case, with Sender Transmission Function STF3 and low γ, senders examine fewer messages than the number sent. Here, the senders would wish to send more messages if more were examined, and there is message congestion at equilibrium. Note that an increase in γ has no effect on the receiver examination function. The sender transmission function shifts back though. Therefore, γ 1 > γ 2 > γ 3 in Figure 3. Proposition³ 4 Suppose that receiver surplus is constant, s (θ) = s¯. Let γ 2 be ³ ´´ C 0−1 (¯ s) −1 1− M = γ 2 . Then for γ > γ 2 , all messages sent are defined by π F examined. For γ < γ 2 , only a fraction of the messages sent are examined. As we discuss further below, if there is over-fishing (γ < γ 2 ), then this will be diminished: there will be less rent dissipation by senders, and better θ types 12

will transmit. There is a clear welfare gain here to the “better” senders from eliminating the worse rivals. The receiver though is unaffected because the examination decision is unchanged. As we shall see below, when sender surplus rises with θ, there is an additional social benefit on the receiver side, stemming from improved quality of messages received.

5.2

Equilibrium with increasing receiver benefits

Consider now the case where s (θ) is increasing with sender type θ. In this case, Z 1 f (θ) s (θ) 1−F the average benefit increases with θ∗ , and, since sav (θ∗ ) = (θ∗ ) dθ θ∗

(see (3)), then

dsav (θ∗ ) = dθ∗

µ

f (θ∗ ) 1 − F (θ∗ )

¶

[sav (θ∗ ) − s (θ∗ )] > 0.

An interior solution to the receiver’s problem is given by: sav (θ∗ ) = C 0 (φ). Consider the Receiver Examination Function, starting with high n. As n falls, θ∗ rises, and so φ rises. However, as the number of messages sent falls sufficiently, the constraint φ = n (= M [1 − F (θ∗ )]) is reached. Thereafter, a lower n (higher θ∗ ) leads to a smaller φ. Thus (still using reading from right to left), the receiver’s choice relation traces out an increasing curve until the constraint φ = n is attained, and then it follows a declining path with φ = n (see Figure 4).

INSERT FIGURE 4. Equilibrium with increasing surplus, s0 (θ) > 0. The highest possible value of φ is attained for a value of γ = γ u with π (θu ) = γ , φu = M (1 − F (θu )), and sav (θu ) = C 0 (φu ). For γ < γ u , then φ < φu , and n > M [1 − F (θu )], and only some messages are examined. For γ > γ u , then φ < φu , and n < M [1 − F (θu )], and all messages are examined. The interesting feature of this case is the beneficial effects of a higher γ for γ < γ u . Then, as noted above, the number of messages examined rises because a higher γ crowds out senders with lower θ. This raises the average surplus from examination, causing the receiver to examine more messages.10 u

5.3

Equilibrium with decreasing receiver benefits

This case leads to an upward-sloping receiver examination function. It may join the constraint, φ ≤ n and leave it, then join it again, etc. Such a upward-sloping relation implies that multiple equilibria are possible. Figure 5 illustrates such a case with four equilibria at the intersections of the REF and STF.11 1 0 It

is possible for aggregate sender surplus to go up too. Figure is drawn with a positive vertical intercept for the REF. This arises if C 0 (0) < s (1), meaning that if only the top profit sender were present, the receiver is interested. If 1 1 The

13

INSERT FIGURE 5. Equilibrium with decreasing surplus, s0 (θ) < 0. The stable equilibria among these are the two for which the reception function cuts the transmission function from above. The logic is akin to that for duopoly reaction functions. In particular, the zero-equilibrium in the Figure is unstable, and the one at (φc , nmax ) is stable.12 More generally, if the reception function meets the transmission function from above at the no examination/no send equilibrium, then it is unstable. Multiple equilibria entail different levels of sender transmission. For example, a low level of transmission is sustained as an equilibrium because receiver rationally anticipate a low average surplus from the highest profit sender types. The receiver then examines few messages, inducing few senders to transmit. A higher level of transmission can also be sustained as an equilibrium because the receiver examines more messages in rational anticipation of high numbers sent and therefore high average surplus from the messages. Senders respond to high examination with high transmission. Now consider the receiver welfare at alternative equilibria. Clearly, higher sender numbers are better because the average expected surplus (sav ) is higher. For the senders, the equilibrium in the Figure at nmax is best because all messages sent are examined. The decreasing receiver benefits case may also entail that the only equilibrium is the one with no messages sent at all. This case may arise if the receiver’s examination function lies everywhere below the senders’ transmission function. Here is are two examples. Example 1. Suppose that s (θ) = 1 for θ ∈ [0, 1/2], and s (θ) = 0 for ∗ 1 ∗ 2 −θ θ ∈ (1/2, 1]. Let too F (θ) = θ. Then, sav (θ∗ ) = 1−θ ∈ [0, 1/2], and ∗ for θ 2

sav (θ∗ ) = 0 for θ∗ ∈ (1/2, 1]. Suppose that C (φ) = φ2 . Then the receiver’s 1 examination function, as a function of θ∗ , satisfies φr (θ∗ ) = 1 − 2[1−θ ∗ ] for r ∗ ∗ ∗ θ ∈ [0, 1/2], and φ (θ ) = 0 for θ ∈ (1/2, 1]. Note that the first part of the curve is a decreasing and convex function. Suppose too that π (θ) = kθ, with k > γ, M = 1. Then the senders’ transmission function is given by inverting φ = γ, as long as φ ≤ 1 − θ, i.e., θ ≥ γ/k. Hence, we have the relation kθ 1−θ

the senders’ transmission function as φs (θ∗ ) = γ[1−θ] for θ ≥ γ/k. If k is kθ large enough, the only intersection with the receiver’s examination function is at φ = 0, and so the only equilibrium is the one where the market unravels.13 However, for low k (and γ not too large) the social optimum involves the lowest set of products.

instead C 0 (0) > s (1), the REF will hug the horizontal axis until a sufficient number of senders transmit that the average surplus is high enough to make it worthwhile to start examining messages. 1 2 This logic also implies that the no examination/no send equilibrium for the constant and increasing sender benefits cases of the two preceding sub-sections is unstable. 1 3 For higher k, there are two other equilibria where the receiver and senders’ functions intersect. For example, if k/γ = 20, then there are two solutions: θ∗ = 0.22 and θ∗ = 0.42. From the argument in the text, the former solution describes the stable equilibrium; the no examination/no send equilibrium is also stable. Welfare is lowest at the no examination/no send equilibrium.

14

Example 2. This example illustrates a major potential problem with unsolicited advertising. Suppose that there were two different classes of product. Let π i denote the sender benefit of each product in class i, i = 1, 2, and similarly let si denote the receiver benefit. We assume that π1 > π 2 and s1 < s2 , so that the first class has higher sender benefit and lower receiver benefit than the second class. There is a large enough number of independent products in each class. (This is similar to the main model except now products are clustered on two points.) In equilibrium, only the high profit senders survive: any low profit sender is driven out of the market since a high profit sender has a bigger incentive to send a message (advertise). Put another way, if the high-profit senders are earning zero expected profits from sending messages, then the low-profit ones cannot enter the market given that the consumer chooses at random which messages to examine. However, the optimum arrangement will have only the low profit senders sending messages if the sum b = π + s is higher. In equilibrium, the low-profit senders are chased from the market by the others, even though the social surplus associated with them is higher. This is reminiscent of Gresham’s law - bad junk mail crowds out good. Note that the receiver would examine more messages if she got more of the low-profit messages, but she does not rationally expect to get it. An extreme form of this phenomenon is when the surplus on the highest profit messages is zero. Then the high-profit ones crowd out all others, and the market unravels completely because no receiver finds it worthwhile to examine any messages. This is the “lemons” problem of e-mail - some people have closed their accounts because of the preponderance of junk. Proposition 5 Suppose that there are two product classes, with many products in each class. Benefits satisfy π1 > π 2 > γ and s1 < s2 . If C 0 (0) ≥ s1 , the only equilibrium has no messages sent. If C 0 (0) < s1 , and π 1 + s1 < π 2 + s2 , the only equilibrium at which a positive number of messages is sent involves only messages of type 1, but the optimum entails only messages of type 2 being sent. Proof. If C 0 (0) ≥ s1 , then if any messages were examined, type 1 senders would crowd out type 2 senders. Suppose not, and that some type 2 senders were transmitting. They would need to earn non-negative profits. But then further type 1 senders would transmit, up till the margin where profits for the type 1 senders were zero. This would mean that the type 2 senders would make losses, and therefore not transmit. Given then that only type 1 senders could transmit at any putative equilibrium with positive examination, the receiver would not wish to examine any messages since the marginal cost exceeds the marginal benefit from type 2 messages even at zero examination. If C 0 (0) < s1 , the above argument again implies that only type 1 senders will transmit messages, and in this case there exists an equilibrium with positive examination. However, if π1 + s1 < π 2 + s2 , the socially optimal messages transmitted are of type 2 since they imbue higher social surplus. Q.E.D. More generally, the fundamental property is that senders transmit messages based on their profitability and receivers examine messages based on average 15

expected surplus. We then expect the greatest problem in the market system is that high profit but low surplus deals survive. The bigger the negative correlation, the bigger the problem of the market failure: even fewer messages are examined but more and “worse” ones are trying to get through.

6

Decentralizable optimum

We now consider conditions under which the first-best optimum can be attained by judiciously choosing γ. First, recall that the optimum allocation entails all messages received being examined and only the messages associated to the highest benefit, b, should be sent. If the set of optimal messages sent is not convex, or even if does not comprise all messages above some critical θ (for example, if b is decreasing, it involves all messages below a threshold, θl ) then it is not possible to replicate the first-best optimum with a single price instrument, γ. The reason is that the market equilibrium necessarily involves all senders above some critical profit level (equal to γ) transmitting messages. The market therefore cannot deliver other patterns. Suppose then that the optimum does entail all messages being sent above some critical level of θ, θh . A sufficient condition is that b is increasing, ³ ´which we assume in what follows. Then, the choice of γ = γ o such that π θh = γ o will ensure that all messages that are optimally sent will be sent in equilibrium. However, full decentralization also requires that the receivers voluntarily exam³ ´ ¡ ¢ ine all the messages sent. That is, it must be true that C 0 nh ≤ sav θh , h ³ ´i where we have defined nh = M 1 − F θh . Recall that (when b is increasing) the optimum cut-off θh satisfies ³ ´ ³ ´ ¡ ¢ γ¯ + C 0 nh = π θh + s θh .

(4)

To check whether the examination condition holds, it is useful to consider a benchmark case when s (θ) = s¯. In this case, we can write the above equation as ¡ ¢ γ¯ + C 0 nh = γ o + s¯. ¡ ¢ Suppose that γ o ≤ γ¯ . Then necessarily C 0 nh ≤ s¯, as required for the receiver to examine all nh messages received. This implies that the optimum is decentralizable. On the contrary, if γ o > γ¯ , it is impossible to decentralize the optimum. In that case, the marginal examination cost necessarily exceeds the average (expected) sender surplus. h Proposition 6 Assume ´ π (θ) is increasing and that s (θ) = s¯, where θ ³ that ¡ ¢ h s. Then, the first-best optimum can be decentralized solves γ¯ +C 0 nh = π θ +¯ ³ ´ ³ ´ h o (by setting γ = π θ ) if and only if π θh ≤ γ¯ .

16

The interesting point about the Proposition is that it involves subsidizing message transmission! Notice that we only allow for action on the transmission price: we do not simultaneously allow consumers to be subsidized (say) for examining more messages. It would seem hard in practice to do so since the opportunities for misrepresentation would be great. The receiver could simply claim to have carefully examined the messages. The intuition for the result is as follows. At the optimum, all messages ought to be examined. This means that if it can be decentralized, then the receivers want to examine at least as many messages as they actually do receive. However, if the transmission price were at or above marginal transmission cost, then a price cut would have a positive effect on both sides of the market by inducing more senders to transmit, and consumers would necessarily examine those messages and be better off, a contradiction. ³ ´ ³ ´ Corollary 2 a) Assume that b (θ) is increasing and that sav θh > s θh ,

the first-best optimum can be decentralized (by setting where θ³h solves ´ (4). ³ Then, ´ γ o = π θh ) if π θh ≤ γ¯ . ³ ´ ³ ´ b) Assume that b (θ) is increasing and that sav θh < s θh , where θh solves ³ ´ (4). Then, the first-best optimum cannot be decentralized if π θh ≥ γ¯ . ³ ´ Proof. First note that a transmission rate γ o = π θh must be set to attain optimality. ³ ´ ¡ ¢ a) The optimality condition implies that γ¯ + C 0 nh < γ o + sav θh . Since ³ ´ ¡ ¢ γ o ≤ γ¯ . Then, necessarily, C 0 nh < sav θh , and receivers do examine all messages, as required. ³ ´ ¡ ¢ b) The optimality condition implies that γ¯ + C 0 nh > γ o + sav θh . Since ³ ´ ¡ ¢ γ o ≥ γ¯ . Then, necessarily, C 0 nh > sav θh , and receivers do not examine all messages, so the optimum cannot be decentralized. Q.E.D. The above analysis effectively focuses on the case of no information congestion. It should be clear from what follows that the interesting case is when there is congestion. Note that if there were congestion at a message transmission rate of γ¯ , then dropping the message transmission rate (by subsidizing) will only raise congestion. Therefore, the optimum will not be decentralizable.

7

Pas de publicité svp and the Federal Do-NotCall List

Some Belgians and Frenchmen have a little sign on their letterboxes saying they do not want advertising flyers. In the US, the Do Not Call List is a successful initiative orchestrated by the Federal Trade Commission that allows people choose not to receive calls from telemarketers. 17

If there is a nuisance cost to receiving the ads, then it makes sense to the individual to decline all of them.14 However, she then foregoes some socially beneficial prospects. Our next aim is to introduce this receiver option into the model, so that the receiver may refuse to accept the messages. Let S ∗ denote the equilibrium value of expected receiver surplus from examining messages, and let C ∗ denote the corresponding examination cost. Assume that receiving each message has a constant annoyance cost, ω. Note that the surplus and examination cost are independent of the nuisance cost, which is sunk if receivers intrinsically dislike receiving messages (telemarketing calls especially). Then the private benefit while receiving messages is S ∗ − C ∗ − nω.With the option of electing to receive no messages, this benefit is to be compared to the zero benefit the receiver gets by opting out.15 Suppose that ω is distributed in the population (which has unit mass) with support [ω, ω ¯ ] and density g (ω) with distribution G (ω), so that different individuals face different annoyance costs. An equilibrium with some, but not all, individuals opting out is then a critical value, ω ˆ ∈ (ω, ω ¯ ) with ω ˆ=

S∗ − C∗ . n

The social benefit associated with a receiver accepting messages is S ∗ − C ∗ − nω + Π∗ − n¯ γ. The two extra terms added here are the senders’ gross benefits and the transmission costs (assumed priced at social cost). A blanket ban is preferred to allowing the nuisance if Z ω¯ A ∗ ∗ ωg (ω) dω + Π∗ − n¯ B ≡S −C −n γ < 0, ω

so that the the social perspective may not prescribe a blanket ban. Allowing individuals to opt out is better than a total ban if Z ωˆ oo ∗ ∗ ∗ ωg (ω) dω > 0, γ ] G (ˆ ω) − n B ≡ [S − C + Π − n¯ ω

where G (ˆ ω ) is the fraction of receivers opting in. This is necessarily positive since S ∗ −C ∗ −nω must be positive for all those opting in (by revealed preference) γ , which also holds by revealed preference because senders only and also Π∗ > n¯ transmit when they get non-negative net benefits. 1 4 In the sequel we suppose that the receiver does not consider the option (in the status quo of no restrictions, and therefore free access) of closing down the message medium entirely. For example, she could disconnect her telephone to block out telemarketers’ calls, or she could close her e-mail account to stop spam. Allowing for such options enriches the analysis that follows. 1 5 The zero here reflects the surplus from the message transmission: the basic message medium may have a positive benefit (telephone service or mail delivery) that is netted out on both sides of any comparison.

18

Conversely, allowing opt-out from a status quo of no opt-out improves welfare if B oo > B A , or Z ω¯ [S ∗ − C ∗ + Π∗ − n¯ ωg (ω) dω < 0. γ ] [1 − G (ˆ ω )] − n ω ˆ

This condition may or may not hold. For example, if ω ˆ is close to ω ¯ then nearly all individuals opt out. If Π∗ − n¯ γ is large, allowing opt-out is socially disadvantageous. Indeed, the reason is because "too many" individuals opt out. To see this, notice that the optimal opt-out cut-off, ω o , is lower than the privately chosen one. This is because the individual does not account for the profit of senders at the margin. In summary, in a comparison of regimes we have: Proposition 7 The opt-out regime is socially preferable to banning messages entirely, but may be worse or better than allowing free access. The first part follows because opting improves welfare by letting in information when both receiver and senders essentially agree; the second part depends simply on whether surplus is greater with or without messages, given that the receiver side achieves a negative total benefit at the status quo of receiving all that senders wish to transmit. The Do-Not-Call opt-out option may also change the quality of messages received through a volume effect, once we aggregate over different consumers. For example, suppose that a particular message type is sent by a sender that produces with increasing returns to scale. Insofar as its equilibrium price decreases with volume, then a reduction of sales through less information getting through to consumers who opt out of receiving messages may lead to a higher price for the remaining consumers. On the other hand, a decreasing returns to scale technology may have the opposite impact. It may also be (even with constant returns to scale) that the consumers who exclude themselves have a more inelastic demand (for example) and so when they opt out the price falls. Note that when the price falls, the remaining consumers expect higher surplus and so end up examining more messages.

8

More than one message?

The main model has each sender sending only one message to the receiver. Clearly, we need to analyze market performance when senders can send many messages. The advantage to the sender from sending multiple messages is that this will improve the likelihood that the recipient does examine at least one of the sender’s messages, and so raises the probability of a successful transaction. However, the recipient need only examine one message from a sender in order to make a transaction, so that any further messages received beyond the first one from a particular sender are wasted. This situation bears some formal analogies to a lottery ticket problem, as we explain below. 19

With multiple messages, we may now find overcrowding in both depth and width. The width decision gives a further dimension of common property problem. In particular, we might think of a lottery (fixed number of prizes) although the prizes are more highly valued by some (high θ types) than others. We conjecture that in equilibrium, higher θ types send more ads. This is clear because they have higher profit. Moreover, increasing the cost of sending each message, γ should help now (for those who do not examine all messages) in two dimensions. First, there will be fewer sender types (the low end drops off) and there will be less competition (in terms of messages sent) at any given level. We nevertheless expect the more subtle property that higher θ types see an increase in the probability they are examined, so raising efficiency. This raises average quality now for two reasons: the drop off of the low types (as we had before) and that the high types now are more “prominent” in the sense that their messages get through more clearly (less clutter from the low types).16 Some formal modeling is provided below. We assume for this section that receivers examine a fixed number of messages, φ, that π (θ) = π ¯ θ, and furthermore that the distribution of types is uniform (f (θ) = 1). Let n be the total number of messages sent by all senders. k Then φ/n ≤ 1 is the probability that a message is examined, so [1 − φ/n] is the probability that none of the k messages sent by a sender is examined.17 The probability that at least one of the sender’s messages is examined is: 1 − [1 − φ/n]k . We assume that senders consider n as fixed when choosing how many messages they should send. (This is akin to a monopolistic competition assumption.) Then sender θ’s problem is h ³ ´ i max π ¯ θ 1 − [1 − φ/n]k − γk (5) k

and the corresponding first-order condition is (holding n constant) k

−¯ π θ [1 − φ/n] ln [1 − φ/n] = γ, where the L.H.S. is positive because the log is negative. Note that the L.H.S. is decreasing in k, so that the second order condition holds. Moreover, the L.H.S. is increasing in θ. This means that the higher θ senders send out more ads. Note too that there are decreasing returns to messages sent so that there are rents - higher θ senders make higher profits. (This latter property can be seen readily by applying the envelope theorem to (5)). We can rewrite the solution as:

k (θ) =

1 ln ln [1 − φ/n]

µ

−γ π ¯ θ ln [1 − φ/n]

¶

,

(6)

1 6 Indeed, note that the first-best social optimum is to have just the top φ types send messages. Each would send just one, so there would be no crowding. 1 7 This is similar to Butters’ (1977) classic model of letterbox advertising.

20

where both terms are negative on the R.H.S. (recall that φ < n). We can now determine the equilibrium cut-off level for sender types, ˆθ (which we will then use to determine ³the´ equilibrium n that we have so far held constant). Since ˆθ is defined by k ˆθ = 0, we have ˆθ =

We can rewrite this as n=

γ . −¯ π ln [1 − φ/n]

φ ³ ´, 1 − exp −γ/πˆθ

(7)

which is clearly (and reassuringly) larger than φ, as indeed is coherent with our maintained hypothesis that φ/n ≤ 1. Since n=M

Z

1

k (θ) dθ,

ˆ θ

substituting for k (θ) from (6) yields ¶¸ Z 1 · µ −1 −γ ln θdθ. n=M ln ln [1 − φ/n (x)] π ln [1 − φ/n (x)] ˆ θ h i R1 Now note that θˆ ln θdθ = [θ ln θ − θ]1θˆ = −1 − ˆθ ln ˆθ + ˆθ , so that the relationship in (7) can be written as ³ ´i ³ ´ h i π ˆθ h 1 − exp −γ/π ˆθ ln ˆθ ˆθ − ˆθ ln ˆθ − 1 . γ which uniquely determines the critical sender type, ˆθ, such that all θ ≥ ˆθ send messages in equilibrium. dˆ θ is negative, so that if receivers examine more, then It can be shown that dφ more sender types are active. Substituting (6) in (7) then indicates that each type sends more messages when receivers examine more messages. Therefore, the two expected effects are illustrated here: both breadth and depth of messages sent rise so the total number of messages received rises. It can also be shown that a higher message transmission cost, γ, causes both breadth and depth to fall. φ=

Proposition 8 Let f be uniform, let π (θ) = π ¯ θ and suppose that φ is given. If senders choose how many messages to transmit, the higher profit types send more messages than lower ones. In equilibrium, higher φ leads more messages sent, so sender transmission function slopes up. Fewer senders are active and each sender sends fewer messages as transmission casts, γ, rise. The first part of the Proposition implies that more profitable senders are more prominent in the message portfolio received. They are then more likely to be examined.

21

9

A Monopoly Information Intermediary Gatekeeper

One benchmark case is when the price of transmitting messages is determined by pure profit maximization concerns. For example, there could be a profit maximizing Post Office, telephone company, Internet Service Provider, or Broadcast Company. Such an entity is the intermediary (or “platform”) in a two-sided market with negative externalities where the price may have a positive effect of reducing the common property problem. Access can be priced by the Post Office — which will therefore account for the common property problem. But it is also interested in the volume of messages. It may not be clear a priori whether it will encourage mailings rather than concentrating on just the highquality senders. However, as indicated below, such a Post Office will price out the common property problem. ¯ messages. This We analyze the simple case where the receiver examines φ ¯ would be the case if C (φ) = 0 for φ ≤ φ, and C (φ) is arbitrarily large otherwise. Let M = 1 and let π (θ) = θ. Suppose still though that the density of advertiser f types is f (θ) with distribution F (θ), and let 1−F be an increasing function. This is the monotone likelihood ratio property (MLRP), or, equivalently, the log-concavity of 1 − F . Suppose first that there were congestion, so that the price, p, a critical sender type ˆθ is willing to pay to be included in the mailing is φˆθ h ³ ´i = p. M 1 − F ˆθ If there is congestion, then some mail is unexamined, so that h ³ ´i M 1 − F ˆθ > φ.

Recall that the constant marginal cost of delivering a message is γ¯ .18 The gatekeeper’s profit is then h ³ ´i ³ h ³ ´i ´ M 1 − F ˆθ (p − γ¯ ) = φˆθ − M 1 − F ˆθ c ,

which is increasing in ˆθ. This means that a monopoly Post Office would price out any congestion. Loosely, if each message had a 50-50 chance of being read, a (risk-neutral) sender would pay twice as much to be read for sure. This means that the monopoly could ration message delivery by half and keep revenues the same. It would save on costs and raise profits. Equivalently, if there is congestion, the monopoly is in the inelastic part of its demand curve and can therefore raise profits by pricing higher. Thus, a monopolist will not tolerate congestion 1 8 This is a gross over-simplification. The cost structure is an important determinant of the Post Office’s pricing policy. Costs, and associated tariffs, are lower per unit in bulk mailings that group similar destinations and when the sender uses a bar-code for addresses. Price discrimination over different classes of mail is another important dimension to the Post Office’s behavior. Non-profit organizations also benefit from lower tariffs.

22

(assuming indeed that all consumers are the same); so suppose that there is no congestion, so ˆθ = p. Then the gatekeeper faces a simple monopoly problem of maximizing (p − c) M (1 − F (p)), which has a straightforward solution. Under the log-concavity condition, it chooses a unique price, and either prices so high that the message-examination constraint is slack, or else holds with equality.19 The case of endogenous examination with s (θ) = s¯ also fits the above monopoly analysis. In this case, the receiver either examines all messages sent or else a fixed number. Again the monopoly always prices out congestion. However, the socially optimal choice of γ may entail there being some congestion (n > φ). This means that the monopoly does not necessarily implement the optimum arrangement, although this is possible.

10

Firm Competition

The models above have assumed that each ad is sent by a firm producing a different new good. However, most junk mail is for credit cards, and most spam concerns Viagra or mortgages. Similarly, many telemarketers call about timesharing. This leads us to consider the effects of competition when there are many firms that offer the products for sale. Suppose for concreteness, that all junk mail is from credit card companies and all credit cards are perfectly homogeneous except for possibly their price. Assume that consumers open messages randomly but there is a cost of each additional message examined. The equilibrium has consumers rationally anticipate the prices announced in the mail, and firms maximize profits rationally anticipating other firms’ prices and consumer mail-opening. Then, as per the Diamond (1971) paradox, the only equilibrium is that all firms set the monopoly price.20 Now though, firms will enter to dissipate all rents. This rent dissipation has an important implication for the welfare economics of the optimal tax. Raising the message transmission price necessarily raises welfare by decreasing the amount of rent dissipation of the monopoly profit. With a higher rate, fewer messages are sent to capture the fixed profit. More generally, when there is competition within product classes, the junk message problem is in a sense a double common property resource problem. 1 9 The monopoly Post Office chooses the same solution as would a monopoly over the wares proposed in the messages. 2 0 This analysis has supposed that all credit cards are the same (the standard homogeneous good assumption). Anderson and Renault (1999) introduce product heterogeneity, and this tempers some of the extreme results associated with the Diamond Paradox. First, consumers will typically open several envelopes in order to find a product better suited to their tastes. This brings firms into competition with each other, and brings equilibrium prices down (there is no competition in the original set-up because only one letter is opened). Moreover, equilibrium price decreases with the number of firms and increases with search costs. The rent dissipation problem mentioned in the text is muted when products are heterogeneous. In this case, there is some benefit from multiple mailings because consumers typically choose the best of several offers. However, as shown in Anderson and Renault (1999), the number of firms is excessive, meaning that an increase in the postage rate is always optimal.

23

First there is over-fishing for a consumer’s attention and second there is overfishing in any product class (business stealing). The case for high postage rates on junk mail (email) is the strongest when most consumers do not open all of their mail and there are high rents so that there are many competing products within any class. What comes to mind is credit card ads through the regular mail and Viagra through email.

11

Conclusions

This paper has studied the economics of communication through unsolicited advertising. Consumer attention is a scarce resource, but may be considered as “common property” by advertisers, and so be over-utilized. Consumers also need to exert effort to process and absorb the content of unsolicited advertising. In determining how much effort to exert, they consider only the average benefit from the advertising sent. This market set-up is unlike standard markets in which the marginal agents on both sides determine the volume of transactions. The important policy implications from understanding these markets have to do with optimally restricting access to the consumers, for example through pricing or direct regulation. In particular, junk email has gotten so out of hand that many people automatically trash many messages, or quarantine them through a spam filter. But this may prevent legitimate firms getting their message across. Bill Gates has suggested an email tax might help: “At perhaps a penny or less per item, e-mail postage wouldn’t significantly dent the pocketbooks of people who send only a few messages a day. Not so for spammers who mail millions at a time.” Indeed, some proposals (for example, by Barry Nalebuff) allow recipients to set their own rates: a college student might accept e-mail with a one-cent stamp; a busy chief executive might demand a dollar. One drawback is that this solution gives all the power to the recipient, who neglects advertiser benefits. With junk mail, too, people do not pay much attention because the average message is of too poor quality. Raising the postage rate on bulk mail may have the advantageous effect of improving the allocation of resources, and through two sources. People recognize only the better offers will be sent, and therefore pay more attention, so getting better mail. This surprising possibility may raise more revenue for the Postal Service because firms are prepared to pay more to mail — more messages will be opened if they cost more to send (because sending then signals it must be a worthwhile offer). One regulatory solution actually enacted in the case of telemarketing is the DNC list. Despite widespread success, one problem with this is that it does not account for advertiser surplus. The more general problem is that of unsolicited ads. The research here stresses the intricate nature of the market equilibrium: consumer expected surplus is determined by the average message quality and determines the attention to devote. The average message quality is determined by the number of messages absorbed and the expected profit of the marginal firm.

24

The current analysis is restrictive in several respects. We assumed a single receiver. Nevertheless, the main part the analysis goes through with multiple types of receiver if the senders know who they are. The equilibrium and optimum then applies to each group separately. Different groups will then be in different circumstances as regards whether or not they examine all their messages. Some groups (with greater proclivity to examine, for example) will receive more messages, as will those with greater attractiveness for senders. The latter are most likely to be the most congested: overfishing is greatest for the biggest fish. However, if the message transmission rate must be universally applied (as opposed to individually tailored) then an optimum analysis must balance out the marginal benefits across individual groups. For example, it is likely that at a second-best optimum, a marginal rise in the transmission rate will improve the welfare of some receivers who are currently in a congested state, while simultaneously reducing the welfare of others who are constrained by the number of messages received. For the latter, a rise in the transmission rate will make them worse off because they will get fewer messages when they already desired more. Another issue that arises is the degree of targeting by senders. For example, engaging market research firms to determine the consumer demographics most likely to buy one’s product is costly, but benefits the firm by being able to target and adjust its advertising message. Along similar lines, senders also choose which media to employ for which consumer types, and different sectors tend to use different media. The framework of this model is hopefully a useful ingredient to analyzing this problem.

References [1] Anderson, Simon P. and Coate, Steven C. (2004) Market Provision of Broadcasting: A Welfare Analysis. Review of Economic Studies, forthcoming. [2] Anderson, Simon P. and de Palma, Andre. (2004) The Economics of Pricing Parking. Journal of Urban Economics, 55, 1-20. [3] Anderson, Simon P., de Palma, Andre, and Thisse, JacquesFrançois. (1992): Discrete Choice Theory of Product Differentiation, M.I.T. Press, Cambridge, Mass. [4] Anderson, Simon P. and Renault, Regis (1999): Pricing, Product Diversity and Search Costs: a Bertrand-Chamberlin-Diamond Model. RAND Journal of Economics, 30, 719-735. [5] Bagwell, Kyle (2002): The Economic Analysis of Advertising, in Handbook of Industrial Organization, III, forthcoming, Elsevier Science, North Holland.

25

[6] Butters, Gerard R. (1977): Equilibrium Distributions of Sales and Advertising Prices. Review of Economic Studies, 44, 465-491. [7] Caplin Andrew, and Nalebuff, Barry (1991): Aggregation and Imperfect Competition: On the Existence of Equilibrium. Econometrica, 59, 25-59. [8] Diamond, Peter A. (1971): A Model of Price Adjustment. Journal of Economic Theory, 3, 156-168. [9] Dixit, Avinash K. and Norman, Victor D. (1978): Advertising and Welfare. Bell Journal of Economics. 9, 1-17. [10] Engers, Maxim P. and Joshua Gans (1998): Why Referees are Not Paid (Enough), American Economic Review, 88, 1341-1349. [11] McFadden, D. (2001): “Economic Choices,” American Economic Review, 93, 3, 351-378. [12] Shapiro C. (1980). Comment on Dixit and Norman. RAND Journal of Economics. [13] Shirman, D. R. (1996) When E-mail becomes junk mail: the welfare implications of the advancement of communications technology. Review of Industrial Organization, 11, 35-48. [14] Willmore, C. (1999) A penny for your thoughts: E-mail and the undervaluation of expert time. Working Paper, University of Warwick.

26

φ φ =n +1

φc

φ =γ

0

n ⎛ n ⎞⎞ ⎛ Π⎜⎜ F −1 ⎜1 − ⎟ ⎟⎟ ⎝ m ⎠⎠ ⎝

n max

Figure 1. Sender transmission function N(φ)

n

φ φ =n +1

c '−1 (s )

0

n Figure 2. Receiver examination function Φ(n) when s(θ) is constant

φ φ 3c

φ =n STF1

STF2

STF3

φ2c = c '−1 (s )

REF

φ1c

n 1max

n 2max

( ) n3max

N 3 φ 2c

Figure 3. Equilibrium with constant surplus

n

φ φ =n

φc

STF

φu REF

0

(

( ))

N 1− F θ n

n max

Figure 4. Equilibrium with increasing surplus

n

φ STF

φ =n REF

φc

0

n max Figure 5. Equilibrium with decreasing surplus

n