Oct 15, 1994 - blending product design and cost accounting, that of auto- ..... programs. GT will be .... was developed from data collected at a machine shop.

Computer-AidedDesign,

Vol. 28, No. 617, pp. 423438.1996 CoWright8 1996 Elsevier Science Ltd Printed in Great Britain. All rights reserved 00104485/96 $15.00 + 0.00

Research

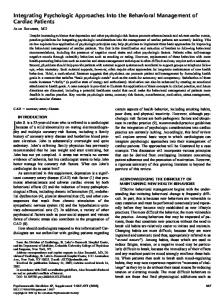

Automated design-to-cost: integrating costing into the design decision Theodore S Geiger and David M Dilts* ers from the actual cost information located in the accounting database, (2) the lack of suitable tools to provide designers with rapid cost feedback on proposed new parts, and (3) the inability to integrate the existing but diverse and heterogeneous data of the various functions. If a computer-integrated manufacturing (CIM) application could be developed that provided designers with product cost information during the design process, it could significantly improve both the design function and the competitive position of the firm 2’. We developed a conceptual model for an approach that provides such automated design-to-cost (DTC) capabilities (see Figure I). The model integrates the manufacturing and accounting concepts of feature-based modelling, group technology coding, computer-aided process planning, and activity based costing. In addition to product cost estimates, the model searches for existing parts which are similar to, or ‘near’, the proposed part and offers them as design alternatives. In order to demonstrate the feasibility of the model, a prototype system was built. Using information gathered from a local machining facility and from accounting literature, the prototype demonstrated the feasibilty of the conceptual model.

While the concepts of design for manufacturability and concurrent engineering have made significant advances in integrating the design function with other areas in the firm, there are still major gaps in timely and accurate costing information available to designers. Our research develops a conceptual model and working prototype of a new application for blending product design and cost accounting, that of automated design-to-cost. The purpose of the application is to provide rapid and dynamic feedback during the design process regarding estimated final product cost of a new part design. The system first calculates the cost of a new part design directly from existing computer-aided design, accounting, and other computer-integrated manufacturing databases. It then finds and displays, along with their costs, all existing parts that are similar or ‘near’ to the proposed part. The model developed was successfully implemented as a prototype. It is able to integrate and process information from the diverse databases of feature-based modelling computer-aided design, group technology classification, computer-aided process planning and activity-based costing. Copyright 0 1996 Elsevier Science Ltd Keywords: product costing, design-to-cost, agement

The time to begin reducing

design and man-

and controlling

a product’s

MODEL OVERVIEW

cost must be at the design stage when product designers have the greatest freedom to improve their desi and to minimize the product’s overall life-cycle cost e . Even though design for manufacturability3,4 and concurrent engineering’ have made great strides in integrating design with other functional areas, there are still major gaps in the accurate and timely costing information available to designers. This is due to three reasons: (1) the traditional isolation of product design-

To introduce

the areas which will be discussed in the literature review, a brief description of the key elements of the DTC system is required. The design process begins when a designer develops a computergenerated part model which is stored in the new part database. The designer then initiates the DTC system and the part model is input into the DTC system. The first system task is to classify the new part, using the group technology classifier, to find the part’s group code. The next tasks follow two parallel paths. The first path calculates the cost of the proposed new part through a three-step process: (1) a process plan is developed, (2) a cost plan is developed from the process

Department of Management Sciences, University of Waterloo, Waterloo, Ontario, Canada *To whom correspondence should be addressed Paper received: 10 May 1994. Revised: 15 October 1994

423

Automated

design-to-cost:

T S Geiger and D M Dilts

DESIGN-TO-COST I

FEKlURE-BASED MODELLING CAD

“NEARNESS’ SEARCH

Figure I

“._

.

PIANNER I

_C

UTPLAUS m

Conceptual model

![Modular product development - AlvaresTech [PDF]](https://m.moam.info/img/260x300/modular-product-development-alvarestech-pdf_6479e7f7098a9ee0288b45ec.jpg)