8th International Conference of Modeling and Simulation - MOSIM’10 - May 10-12, 2010 - Hammamet - Tunisia ”Evaluation and optimization of innovative production systems of goods and services”

SHIFT-SCHEDULING OF CALL CENTERS WITH UNCERTAIN ARRIVAL PARAMETERS S. LIAO, C. VAN DELFT

G. KOOLE, O. JOUINI

Ecole Centrale Paris 92290 Chˆatenay-Malabry, France

[email protected],

[email protected]

Groupe HEC 78351 Jouy-en-Josas, France

[email protected],

[email protected]

ABSTRACT: This paper considers a multi-periodic multi-shift call center staffing problem with two types of jobs: calls and emails. The arrival rate of calls is random and the workforce presents some flexibility: the agents can be affected to one job type in real-time. At each period of the day, a service quality constraint limits the waiting time for a call. The staffing problem is modeled as a newsboy-type model under an expected cost criterion. We then consider three different approaches in order to solve the optimization problem. First, we explicitly formulate the expected cost newsboy-type formulation as a stochastic program. Second, the formulation is extended to the conditional value-at-risk (CVaR) setting. Third, we develop the robust optimization approach. The proposed approaches are evaluated with real data obtained from the call center of a Dutch hospital. Computational results show that the robust approach is highly tractable and the solutions have good quality under several conditions. We show in addition the necessity of taking into account the randomness of the call arrival rates. We also show that profiting from the email job flexibility is highly attractive. KEYWORDS: Call centers, uncertain arrival parameters, staffing, newsboy model, stochastic programming, robust programming.

1

INTRODUCTION

Call centers have become more and more important for many large organizations: a study (Brown et al., 2002) reports that in 2002 more than 70% of all customer-business interactions were handled in call centers, and that the US call center industry employed more than 3.5 million people, which corresponds to 2.6% of the workforce. The staffing cost is a major component in the operating costs of call centers and can represent 70% of the labor cost (Gans et al., 2003). An efficient staffing is thereafter crucial. Unfortunately, the uncertainty plaguing the arrival process render the staffing problem difficult. Statistic studies (Avramidis et al., 2004; Shen and Huang, 2008) show that in addition to the usual uncertainty modeled by a stochastic process, there exists some uncertainty for the process parameters themselves, namely the parameter arrival rate is itself random and non-stationary. But in fact, most call center models in the literature assume a known, fixed arrival rate and ignore the issue of arrival rate uncertainty. In (Gans et al., 2003), the authors say “Surprisingly, however, there is little work devoted to an exploration of how to accommodate uncertainty”. A few papers take this parametric randomness into account. In (Jongbloed and Koole, 2001), the authors propose to include arrival parameter uncertainty via a

Poisson mixture model for the arrival process, which allows to model the over dispersion associated with random arrival rates. This approach leads to a generalization of the standard Erlang formula-type staffing approaches. In a different vein, in (Harrison and Zeevi, 2005; Whitt, 2006; Robbins, 2007; Steckley et al., 2004) the basic idea can be summarized as estimating performance indices, conditional on the random model-parameter vector, and then unconditioning to get the effective indices. Concerning the arrival rates or and the random employee absenteeism, but under the assumption of a constant staffing level, (Harrison and Zeevi, 2005; Whitt, 2006) develop static stochastic program via stochastic fluid model approximation. (Gurvich et al., 2009) has used stochastic programming to account for arrival-rate uncertainty when making shift-run staffing and call-routing decisions. (Robbins, 2007), (Robbins and Harrison, 2008) and (Robbins et al., 2008) extend the stochastic programming framework to employee scheduling, and recent papers by (Mehrotra et al., 2009) and (Gans et al., 2009) use recours action to adjust pre-scheduled staffing levels in reaction to realized deviations from arrival-rate forecasts. In (Bertsimas and Doan, 2008), the authors develop a fluid model approximation to solve both the staffing and routing problem for large multiclass/multi-pool call centers with random ar-

MOSIM’10 - May 10-12, 2010 - Hammamet - Tunisia

rival rates and customer abandonment. The model is solved via stochastic fluid model approximation and a robust optimization approach. Different from all these studies, we consider a call center with flexible agents to handle inbound calls and emails. The arrival rate of calls is assumed to be random. We model the staffing problem of this call center as a cost optimization-based newsboy-type model. We then propose three approaches to solve it. The first approach formulates the problem as a classic stochastic optimization problem. The second approach consider in a CVaR generalization of the classic stochastic optimization. The third approach relies on robust optimization theory. We illustrate the main characteristics of the optimal solutions corresponding to these approaches with data gathered from a Dutch hospital call center. We distinguish two main contributions in this paper. The first contribution is the modeling and the analysis of the staffing problem of a blending call center with uncertain call arrival parameter. The second contribution is the analysis of the impact of the flexibility offered by emails in order to mitigate the undesirable effects of uncertainty. This paper is an extension of our working paper (Liao et al., 2009). The rest of the paper is structured as follows. In Section 2, we describe the call center model under study and formulate the associated optimization problem. In Section 3, we present three different solution approaches for the optimization problem. In Section 4, we then conduct a numerical study to evaluate the approaches, to analyze the necessity of taking into account the uncertainty of the call arrival parameter, and to analyze the impact of the flexibility offered by email on the optimization problem. The paper ends with concluding remarks and next steps for research. 2

Problem Formulation

We consider a call center simultaneously handling inbound calls, to be served without delay, and emails, that can be delayed in some extend. In this section, we describe the call blending problem of interest and develop the economic framework associated to the optimization of the call center staffing level under uncertain arrival rates. 2.1

The Inbound Calls Arrival Process

Generally speaking, several characteristics of call center arrival processes have emerged in recent studies. First, the total daily number of calls has over dispersion relative to the classical Poisson distribution (i.e. the observed variance is greater than the observed mean). Second, the arrival rate varies considerably with the time of day. Third, there is strong positive correlation between arrival counts in a time partition

of a day. In order to address these issues, i.e. uncertain timevarying arrival rates coupled with significant correlations, we model the inbound calls arrival process as a doubly stochastic Poisson process (see (Avramidis et al., 2004; Harrison and Zeevi, 2005; Whitt, 1999)). In our setting, consider I as the set of the distinct, equal periods of length T , divided from a given working day. The mean arrival rate of calls during period i is denoted by Λi for i ∈ I, and is uncertain. Furthermore, according to (Avramidis et al., 2004; Whitt, 1999), the arrival rate Λi , for i ∈ I, is assumed to be of the form Λi = Θfi ,

(1)

where Θ is the only (positive real-valued) random variable that can be interpreted as the (unpredictable) “busyness” of a day. A large (small) outcome of Θ corresponds to a busy (not busy) day. The constants fi model the shape of the variation of the arrival rate intensity across the periods of the day. Formally, let us denote a sample value, for a given day, of the random variable Θ by the positive real value θ and the corresponding replication of the arrival rate over period i for that day is λi = θfi . The random variable Θ is characterized by a discrete probability distribution, defined by the sequences θl and probability pθl , with l ∈ L. We assume exponential service times, with rate µ, independent of the time period. Furthermore, the calls are served according to a single FCFS queue with multiple servers. Neither abandonments nor retrials are allowed. For a given θ, we denote vi (θ fi ) the required number of agents in order to meet the quality of service constraint in period i to handle the calls (computing using the Erlang C formula). 2.2

The Emails Arrival Process

We assume that all emails to handle are available at the beginning of the day: think about a call center that stores all the emails of a given day and handle them the following one. We denote by W the random required number of agents to handle the emails workload in one period. The random variable W is characterized by a discrete probability distribution, defined by the sequences wk and probability pwk , with k ∈ K. 2.3

Cost Criterion

We consider a multi-shift call center with J as the shifts set. We develop a cost model to be minimized, in which the decision variables are the number of agents xj assigned to shift j for the day of interest, with j ∈ J. aij indicates if schedule j is staffed in

MOSIM’10 - May 10-12, 2010 - Hammamet - Tunisia time period i, with i ∈ I, and j ∈ J. For any given vector x = {xj } and matrix a = {aij }, we can compute y = {yi }, using y=ax, where yi represents the number of agents who are scheduled to work at time period i, i ∈ I.

in Equation (2).

We assume that all agents are able to handle both types of jobs, calls and emails. Since calls have to be addressed in real time or near real time, we give them the priority over the storable/flexible job of emails. For instance, assessing the flexibility offered by emails and its impact on the optimization staffing problem is one of the main contributions of this paper. For each period i, if the actual number of agents yi is larger than the required number of agents to handle the calls Vi (θfi ), then we assign Vi (θfi ) agents to calls and yi −Vi (θfi ) agents to emails. If not (yi < Vi (θfi )), we assign all the yi agents to calls, and no agents are thereafter assigned to emails. In this under-staffing case, a penalty u is paid per difference unit between the actual capacity yi and the required one Vi (θfi ). Each agent gets a salary c for a period where he is assigned to work. If it happens that at the end of the day there is still a backlog of emails, they have to be handled on overtime. The overtime salary is r per agent per period. The assumption c < r < u is necessary to guarantee coherence of the problem. The assumptions r < u ensures that the calls have the priority to be addressed over the storable/flexible job of emails. The assumption c < r is necessary to ensure that it is not optimal to have agents working in overtime if it can be avoided.

This convexity allows us to get the convexity result on xj of the cost functions of the stochastic programming approach with CVAR conception we will propose in Section 3. The proof of Theorem 1 and Proposition 1 are omitted due to the space limitation. They will be given in the final version of this paper.

Let us denote by C(xj ) the expected daily total cost associated with the staffing level y. It can be expressed as

C(xj )

=

∑

c yi + u E

i∈I

[∑

(yi − Vi (Θfi ))−

] (2)

i∈I

[ ]+ ∑ + +r E W − E[ (yi − Vi (Θfi )) ] , with

yi =

∑

i∈I

aij xj ,

i ∈ I, xj ∈ N.

j∈J

where E[X] denotes the expected value of a random variable X, and x+ = max(0, x) for x ∈ R. In Equation (2), the first term is the salary of the agents working during the regular time. The second term is the expected penalty cost in case of under-staffing with respect to the service level objective for the inbound calls. The third term is the expected overtime salary used to handle the eventual remaining unfinished emails at the end of the regular time. Under this economic framework, our objective concretely consists on deciding on the optimal value of xj , j ∈ J, which minimize the total daily cost given

Theorem 1 The total cost function C(xj ) is joint convex on xj , j ∈ J.

3

Optimization Approaches

In this section we propose three different approaches to solve our staffing problem. The first approach refereed as classic stochastic programming approach directly built on the discrete probability distributions characterizing the random variables of the model (namely Θ and W ). The second approach we introduce into the stochastic programming approach an explicit way to take the risk into account by adopting a risk aversion measure in objective. The cost function of classic stochastic programming approach can be viewed actually a special case of this risk aversion measure. The third approach refereed to as robust optimization approach consists on optimizing the staffing level with respect to the different possible “bad” scenarios that would happen, i.e., the cases where Θ and W take large values. In what follows we concretely formulate our problem under the three approaches of optimization. We then compare them through the numerical analysis of Section 4. Classic Stochastic Programming Approach (CSPA): The first approach consists in developing (2) under a linear form as follows, we average on all the possible values of the random variable Θ and W . For each value θl of Θ, we use Equation (1) in order to get the arrival rate of calls in each period i, say λi,l , λi,l = θl fi . A required number of agents, say vi (θl fi ) is corresponding to each λi,l according to the Erlang C formula. The optimization problem can be then formulated as following mixed integer program: M in

∑

c yi +

i∈I

s.t.

yi =

∑

∑∑

− pθl u Mi,l +

l∈L i∈I

∑

pwk r Nk+

k∈K

i ∈ I,

aij xj ,

j∈J

Mi,l = yi − vi (θl fi ), Mi,l =

+ Mi,l

N k = wk − Nk =

− Mi,l ,

− ∑∑

l∈L i∈I + Nk − Nk− ,

i ∈ I, l ∈ L, i ∈ I, l ∈ L,

+ pθl Mi,l ,

k ∈ K, k ∈ K,

(3)

MOSIM’10 - May 10-12, 2010 - Hammamet - Tunisia + − Mi,l , Mi,l , Nk+ , Nk− ≥ 0, xj ∈ N,

i ∈ I, l ∈ L, k ∈ K, j ∈ J.

Stochastic Programming Approach with Risk Aversion (RASPA): Our first model relies on the expected cost criterion. This measure is risk-neutral and may not be fit for practical decision-making. A modern way to take into account the risk consists of by bounding the conditional value at risk (CVaR) (Rockafellar and Uryasev, 2002). The CVaR is known as a coherent risk measure, which consistents with the second (or higher) order stochastic dominance (Ogryczak and Ruszczynski, 2002) and possesses the attractive feature of being computationally tractable in particular, in the framework of stochastic programming. Let us briefly recall the definition of the conditional value at risk (see (Gothoh and Tankano, 2007) and (van Delft and Vial, 2009)). Let L(x, ξ) be the loss which is random for a fix x. Let us denote the distribution function of L by ψ(s|x) := P{L(x, ξ) ≤ s} . In other words, ψ(s|x) is the probability that the loss is less than s. Let 0 < α ≤ 1 be a given confidence level. We associate with it the critical threshold

problem since the solution with α = 1 is equal to that of the classic stochastic programming approach. The optimization problem can be then formulated as following mixed integer program:

∑

s.t.

(4)

The conditional value at risk is CV aR(α) = E(L(x, ξ)|L(x, ξ) ≥ s(α)).

c yi +

yi =

∑

∑

+ − − s ≤ zk,l , k ∈ K, l ∈ L, u Mi,l + r Nk,l

i∈I

i ∈ I,

aij xj ,

j∈J

Mi,l = y − vi (θl fi ), + − Mi,l = Mi,l − Mi,l , ∑ + Nk,l = wk − Mi,l ,

i ∈ I, l ∈ L, i ∈ I, l ∈ L, k ∈ K, l ∈ L,

i∈I + − Nk,l = Nk,l − Nk,l ,

k ∈ K, l ∈ L,

+ − + − Mi,l , Mi,l , Nk,l , Nk,l ,≥

xj ∈ N, s ∈ R, zk,l

0 i ∈ I, k ∈ K, l ∈ L, ≥ 0, j ∈ J, k ∈ K, l ∈ L.

In this problem formulation, the objective is to minimize the ∑ ∑ expected value of the total − + costs c yi + u Mi,l + r Nk,l which exceeds the i∈I

threshold s(α), with respect to x and s. Thanks to the convexity of the ∑total ∑ cost function in x, the CVaR pwk pθl zk,l is joint convex in function s + α−1 k∈K l∈L

(5)

In (Rockafellar and Uryasev, 2002), the author introduces that the minimization of CVaR is the solution of a simple minimization problem with respect to x ∈ X and s ∈ R, simultaneously: min CV aR(α) = min{s + α−1 E[(L(x, ξ) − s)+ ]}, (6) x

pwk pθl zk,l

k∈K l∈L

i∈I

i∈I

s(α) = min{s|ψ(s|x) ≥ 1 − α)}.

∑∑

s + α−1

M in

x,s

where X ⊂ Rn is a feasible region. It is shown that the right-hand side optimization problem in Equation (6) is joint convex in (x, s) if the loss function L(x, ξ) from Rn to (−∞, ∞] is convex. It is furthermore proved that with an optimal solution (x∗ , s∗ ) of the right-hand side optimization problem in Equation (6), x∗ is an optimal solution of the left-hand side one, and s∗ is almost (or sometimes exactly) equal to s(α), see (Rockafellar and Uryasev, 2002). The given confidence level α is associated to the protection against risk. For example, if we take α = 0.1, so that the CVaR function would control the largest 10% of the total costs. It is discussed in (Gothoh and Tankano, 2007) that the CVaR minimization gives a simple generalization of the classic stochastic optimal

(x,s). The special case of this optimization problem with α = 1 is equivalent to that of the classic stochastic programming approach. Robust Optimization Approach(ROA): In reallife applications, the stochastic programming approaches(with or without risk aversion) often suffers from the high dimensionality of the problem. It is not appropriate neither when we can not well characterize the demand distribution. We refer the reader to (Thenie et al., 2007) and (van Delft and Vial, 2004) for more discussions. A robust approach using the robust optimization would be in such a case an attractive alternative choice. It consists on considering a restricted problem associated with a given level of uncertainty. The robust approach takes then into account the uncertainty without assuming a specific distribution, while remaining at the same time highly tractable and providing insights for the analysis of the problem. It also allows adjustment of the level of robustness of the solution in order to trade off between performance and protection against uncertainty, see (Bertsimas and Sim, 2004) and (Bertsimas and Brown, 2005) for further details. We consider the robust approach which considers all possible worst-case scenarios with respect to the random variables Θ and we take W as its expected value.

(7)

MOSIM’10 - May 10-12, 2010 - Hammamet - Tunisia

If the the random variable Θ belongs to the uncertainty set U , then we need to solve the following mixed integer problem: M in s.t.

max θ∈U

yi =

∑

c yi +

i∈I

∑

∑

M in s.t.

i∈I

i ∈ I,

(8)

i ∈ I, i ∈ I,

i ∈ I,

xj ∈ N,

j ∈ J.

i∈I

s.t.

yi =

∑

∑

u Mi− + r N + i ∈ I,

(9)

j∈J

Mi = yi − vi (θ fi ), Mi = Mi+ − Mi− , ∑ N =w− Mi+ ,

Mi = yi − vi ((θ + k σθ ) fi ),

i ∈ I,

Mi = Mi+ − Mi− , ∑ Mi+ , N = w + k σw −

i ∈ I,

i ∈ I, i ∈ I,

i∈I

i ∈ I,

xj ∈ N,

j ∈ J.

Proposition 1 Let C0 (x, θ, w) be the optimal objective value of problem defined in (9). For any i ∈ I and δ > 0, C0 (x, θ + δ, w) ≥ C0 (y, θ, w),

(10)

Numerical Comparison

In this section, we conduct a numerical study in order to compare and evaluate different approaches. In Section 4.1, we describe the numerical experiments. In Section 4.2, we analyze the results and derive various insights. 4.1

N = N + − N −, Mi+ , Mi− , N + , N − ≥ 0,

Experiments

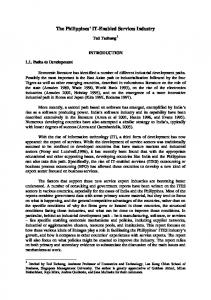

In this paper, we use data from a Dutch hospital where the number of calls over the periods of the same day are strongly positively correlated. Agreeing with the observed experience in call centers, although there is significant stochastic variability in the arrival rate from one day to another, there is a strong seasonal pattern across the periods of a given day, see Figure 1. We assume the arrival rate may be accurately estimated. The planning interval is set to be Arrival rate

7.00

It is obvious from the proposition (10) that, an une certainty set U := {Θ : 0 ≤ θ ≤ θ},

i ∈ I, j ∈ J.

The definition of the uncertainty set U can be modified by changing the value of the parameter k which presents the robust degree considered. The bigger k is, the uncertainty set is larger, and the optimal solution is more conservative (robust). 4

i∈I

aij xj ,

i ∈ I, (13)

aij xj ,

Mi+ , Mi− , N + , N − ≥ 0, xj ∈ N,

In order to analyze the above robust formulation, we study firstly the properties of the optimal value of the following optimization problem: c yi +

i∈I

i∈I

N = N + − N −, Mi+ , Mi− , N + , N − ≥ 0,

∑

u Mi− + r N +

N = N + − N −,

i∈I

M in

yi =

∑

∑

j∈J

j∈J

Mi = yi − vi (θ fi ), Mi = Mi+ − Mi− , ∑ N =w− Mi+ ,

c yi +

i∈I

u Mi− + r N +

aij xj ,

∑

6.00 average day (fi) not busy day

5.00

busy day 4.00

3.00

e w), xj ∈ N, j ∈ J. maxC0 (x, θ, w) = C0 (x, θ, θ∈U

(11)

2.00

1.00

0.00 0

Suppose that the uncertainty set U is defined as follows:

1

2

3

4

5

6

7

8

9

10

11 period

12

(12)

Figure 1: (Solid line), call arrival rates fi ; (higher dashed line), a busy day; (lower dashed line), a not busy day

The robust formulation of the mixed integer problem with the uncertainty set (12) is as follows:

from 7 : 00 to 18 : 00, and is divided into 11 periods of one hour each. Agents work 8-hour days with

U = {Θ : 0 ≤ θ ≤ θ + k σθ , k ≥ 0}.

MOSIM’10 - May 10-12, 2010 - Hammamet - Tunisia

a break lasting an hour after his first 4 hours work. There are 4 shifts. Using the data of the Dutch hospital, we determine the fi s of Monday by averaging on all Mondays of year. The arrival rates f1 , f2 , ... f11 are 0.05, 1.84, 3.44, 3.15, 2.90, 1.29, 2.84, 2.50, 1.74, 0.52 and 0.13, respectively. We assume that the random variable describing the “business” of the day, Θ, follows a discrete probability distribution. We obtain this distribution by discretizing a normal distribution with mean E[Θ] and standard deviation (std) σΘ . Using the data of the hospital for all Mondays of a given year, we have E[Θ] = 1 and σΘ = 0.21. We also truncate the distribution of Θ by considering only replication values ranging from E[Θ] − 3σΘ to E[Θ] + 3σΘ . The cumulative probability of the remaining intervals are then uniformly shared on the interval [E[Θ]−3σΘ , E[Θ]+3σΘ ]. This would avoid to consider useless values such as negative or very large values. Having this in hand, one can easily get the probability distributions of θfi by mean of Equation (1). The mean service time is 1/µ = 5 minutes and the service level per period is P r{W ≤ 20s} ≥ 80%. We can then easily deduce the required agents number Vi in period i using the Erlang C formula. In a similar way, we discretize a normal distribution in order to characterize the random variable related to emails, W . We consider three cases: Normal(120, 12), Normal(60, 6) and W = 0, where Normal(x, y) denotes a normal distribution with mean x and standard deviation y. The cost parameters are as follows. The salary during the regular time is c = 15 per agent per period. The salary during the overtime r = 20 per agent per period. For each period, we pay a penalty u for being understaffed of one agent. We vary u by choosing the values 50, 100 and 500 which satisfies the assumption c < r < u. We first compute the optimal staffing levels given by different approaches. For the RASPA, we compare 8 values of α (= 1, 0.8, 0.6, 0.4, 0.2, 0.05, 0.028, 0.00135) which associate with a protection against risk level ranging from low to high values. Similarly, we compare 5 values of k(= 0.2, 0.6, 1, 2, 3) which associates with a protection against risk level ranging from low to high values for the ROA. Next, we randomly generate 10000 scenarios according to the distribution of Θ and W described above. Each scenario, indexed by s, corresponds to a couple {θs , ws } which is an independent replication of the random variables {Θ, W }. For a given scenario s, we denote vs, i (θs fi ) the required number of agents. The average total cost of a given approach is calculated as follows. With the optimal staffing level x∗j,m determined above, we then compute for each scenario ′ s the associated total cost Cs,m (x∗j,m ). m corresponds

to different models and conservative levels presented above. We then get the average value of the total cost by simply averaging on all possible scenarios. ′ Cs,m (x∗j,m )

=

∑

∗ c yi,m +

i∈I

∑

∗ u (vs, i (θs fi ) − yi,m )+

i∈I

+r (ws −

∑

(14) ∗ (yi,m

− vs, i (θs fi )) ) , + +

i∈I

with

yi,m =

∑

aij xj,m , i ∈ I, xj,m ∈ N.

j∈J

4.2

Insights

In this section, we comment the numerical results and derive the main insights. We first show the necessity of considering the uncertainty in the call arrival parameters. Second, we evaluate and comparer the proposed approaches: the CSPA, the RASPA and the ROA. We also underline the efficiency of the ROA. Third, we analyze the effect of the flexibility provided by emails on our staffing optimization problem. 4.2.1

The necessity of considering the uncertainty in arrival rate Λi

In order to analyze the necessity of taking into account the randomness of the call arrival rates, we provide a comparison between the CSPA with the common practice which is based on the expected value of the random variable Θ, called deterministic approach. In this deterministic approach we reduce Θ to its expected value E[Θ]. Equation (1) gives the values of E[θfi ], E[θfi ] = E[Θ]fi . The required number of agents to handle the calls of period i, Vi (E[θfi ]), is calculated using Erlang C formula, µ and the 80/20 rule. Since the objective is to evaluate the effect of randomness of the call arrival rates, in this deterministic approach we average on all possibilities of the random variable related to emails, W , as the stochastic approaches (with or without risk aversion) do. In order to compare computational results of two approaches, we plot a total cost mean-standard deviation(std) frontiers with respect to different email workload tail, W , and different under-staffing cost parameter, u. In Figure 2, break point line corresponds to the deterministic approach, and solid line the CSPA. The three points on the same line from lower left to upper right represent the value of u = 50, 100, 500 respectively. Three cases of email workload: Normal(120, 12), Normal(60, 6) and W = 0, are presented from left to right side. Figure 2 shows that for both approaches, the average total costs and total cost stds increase when the under-staffing cost or email workload increases. But under the same parameters of W and u, the CSPA performances much

MOSIM’10 - May 10-12, 2010 - Hammamet - Tunisia

Deterministic(no email)

3500

Deterministic(email(60,6)) Deterministic(email(120,12)

3000

Stochastic(no email) Stochastic(email(60,6))

2500 Total Cost std

Stochastic (email(120,12))

2000 1500 1000 500 0 2500

3000

3500 4000 Mean Total Cost

4500

5000

Figure 2: Mean-std frontiers of deterministic approach and CSPA

better than the deterministic approach, by obtaining smaller average total costs and smaller total cost stds, specially in the case where the under-staffing cost u is high. From the analyst of the probability distributions of total cost values, we find that the total cost values associated with the deterministic approach scatter in a relatively wide interval which includes very high costs. Specially in the case of large values of u, the probabilities associated with very high total cost outcomes are non-negligible. The total cost values from the CSPA achieve very high values much less frequently comparing to the deterministic approach, even though they also scatter in a relatively wide interval. With the RASPA and ROA, this risk issue will be better settled, see Section 4.2.2 and Figure 7. Recall that the CSPA takes into account all the possible value of arrival rates, while the deterministic approach assumes that the call arrival rate per period of the day is deterministic and is equal to its expected value. We can see that it is necessary to consider the uncertainty of arrival rates, which is ignored by most existing studies. 4.2.2

Evaluation and Comparison of the proposed Approaches

We mentioned in Section 3 that the RASPA gives a generalization of the CSPA. The extreme case of the RASPA with α = 100% is identical to the CSPA. In the comparison study, we include the CSPA into the RASPA. In what follows, we compare between the performance of the RASPA and the ROA for given distribution of Θ and W . We particularly focus on the analysis of the impact of the under-staffing cost parameter, u. If we look on the staffing levels, the optimal solution of each approach increases in u. The reason is that for large values of u, we tend to highly cover ourself in order to avoid under-staffing situations that would increase drastically the total cost. Under the RASPA, we see that the optimal staffing level x corresponding to a small α is always bigger

than that corresponding to a larger one, independently of all remaining parameters. Table 1 presents an instance of the impact of α where u is chosen to be 50 and email workload follows Normal(60, 6) distribution. The reason is that the CVaR measures with small values of α protect more strictly against risks. For example, controlling the expected value of the largest 40% total costs (α = 0.4) is more strict than controlling the expected value of all total costs (α = 1). Thus a risk-averse manager who cares about large total cost via α-CVaR is likely to schedule more agents according to small values of α than large ones. The same phenomenon exists for the ROA. The staffing level x increases along with the robustness level, which is described by k. This indicates that both ROA and RASPA are adjustable by selecting different values of conservative levels, in order to trade off between performance and protection against uncertainty (risks). However, RASPA with (α ̸= 1) always leads to an optimal staffing level larger than that of the CSPA, while this is not always the case under ROA. Table 1: an instance of the impact of α in RASPA α 1 0.8 0.6 0.4 0.2

xa 4 4 4 5 5

xb 16 16 17 17 18

xc 5 5 5 5 6

xd 2 3 3 3 3

In order to compare the computational results between the approaches, we plot in Figures 3-6 the mean-std frontiers of the total costs with respect to different values of u, W and the conservative level for RASPA and ROA. The points on the same curve are associated with different conservative levels (confident levels α for the RASPA and robust levels k for the ROA). In general, for both models, the average total costs increase when the conservative level increases (the confidence level decreases or equivalently the robust degree increases), while the total cost std decreases. The best average total cost for any set of parameters is always given by the CSPA. Because by the Law of Large Numbers, for a given (fixed) staffing level, the average of the total cost over many replications, will converge with probability one to the expectation. So that the solution of the CSPA will be optimal on average. From Figure 3 and 4 we see that in the case where u takes small values, the RASPA and ROA works almost identically, independently of the email workload size W . The two curves coincide since the two models have almost the same average total costs and total cost stds. This indicates that, if the under-staffing

MOSIM’10 - May 10-12, 2010 - Hammamet - Tunisia

cost is not important, it makes not much difference from taking only one sample path covering all possible sample paths of the random arrival rates. The total cost will not increase much even if an under-staffing situation occurs.

big u, W ~ Normal(120,12) 800

RASPA ROA

700 600 500 400 300 200 100

In the case where under-staffing cost is important, i.e., u is high, different results emerge due to conservative level. Figure 5 and Figure 6 show that the RASPA works better than ROA when the manager has not much intention to averse risks (k is small and α is close to 1). When the risk-averse is important, the curves of ROA and RASPA coincide in the case of small email workload W (see Figure 5). For high values of W (for example Normal (120,12) distribution), ROA is even better than RASPA, see (Figure 6). small u, W=0 800 RASPA

700

ROA

std total cost

600 500 400 300 200 100 0 2500

2700

2900

3100

3300

3500

3700

3900

mean total cost

Figure 3: Mean-std frontiers in the case W = 0 with small u

0 4000

4200

4400

4600

4800

5000

5200

Figure 6: Mean-std frontiers in the case W ∼ Normal(120, 12) with big u

CSPA is always the lowest, the total cost of a single trial might be very high. One important common feature between ROA and RASPA is the departure point: protecting against uncertainty (risks). In order to show the probability distribution of total costs associated with different approaches, Figure 7 displays an instance case with u = 100 and W following Normal (60,6) distribution. We can see that when the ROA and RAPSA take high conservative level, all the total cost values centralize in almost the same value, and the probability of obtaining high values almost zero. If we need solutions protecting us perfectly from risk, these two approaches provide good solutions by taking a high conservative level. 1

Deterministic CSPA

0,9

RASPA, alpha=0,2 0,8

ROA, k=2

0,7 0,6

small u, W~ Normal(120,12) 500

0,5

RASPA

0,4

ROA

450 400

0,3

350

0,2

300

0,1

250

0 2000

200

3000

4000

5000

6000

7000

8000

9000

10000

150 100 50 0 4000

4200

4400

4600

4800

5000

Figure 4: Mean-std frontiers in the case W ∼Normal (120, 12) with small u

big u,W=0 3500 RASPA

3000

ROA

std total cost

2500 2000 1500 1000 500 0 3000

3200

3400

3600

3800

4000

4200

4400

mean toal cost

Figure 7: The probability distribution of total cost values associated with different approaches

In conclusion, the ROA provide solutions that at least as good as those under the RASPA when understaffing cost is not important or the manager pay attentions to averse risk. Moreover, ROA requires much less time than the former. Note that a problem formulated under the RASPA has the same computational complexity as one formulated under the CSPA, because they cover all possible sample paths. ROA have a significant advantage in terms of computational time since it needs to take under consideration only one sample path.

Figure 5: Mean-std frontiers in the case W = 0 with big u

4.2.3

In Section 4.2.1, we mentioned that the total cost values associated with the CSPA scatter in a relatively wide interval which includes very high costs. This indicates that, even though the average total cost of

In this section, we illustrate the advantage of the flexibility offered by emails using the numeric results under CSPA, with respect to different values of understaffing cost u and email workload W . Table 2 dis-

Advantages of The Flexibility Offered by Emails

MOSIM’10 - May 10-12, 2010 - Hammamet - Tunisia

u 50 500

Table 2: the computation results by classic stochastic programming approach Email mean total cost Std1 salary cost under-staffing Std2 overtime w=0 2531.76 433.02 2310 221.74 433.02 0 N(120,12) 4077.22 443.90 3570 0.4 10.46 506.82 w=0 3165.85 692.65 3045 120.85 692.65 0 N (120,12) 4080.82 466.38 3570 4 104.57 506.82

plays the average total cost, the average values of the three components of the total cost, and also the std of the total cost, the under-staffing cost and the over-time cost, denoted by Std1 , Std2 and Std3 , respectively. We can see from Table 2 that the average total cost for a call center blending calls and emails workload, is less than the sum of the total cost for a call center treating only calls (2531.76, 3165.85 for u = 50, 500 respectively) and the cost for treating only emails (c ∗ W ). This means we make profit by blending the calls and emails workload. This profit is due to the bimodal shape of required agents number for treating calls as in Figure 1, many idle agents can be assigned to treat emails. In a blending call center, the staffing level only needs to be increased by a small number compared to the case where we have only emails (we would need 120 working hours). Even though additional over-time cost occurs after the blending of the calls and emails workloads, the saving is large enough to cancel it out. Particularly in the case where u is much bigger than r, more agents should be scheduled to protect against arrival rate uncertainty in the case W = 0, more idle agents are available to be assigned to treat emails. It is remarkable that in Table 2, the under-staffing cost stds are relatively high comparing to the associated average under-staffing costs. This is because of highly sensitive required agents number for treating calls over calls arrival rate variability. Small fluctuations of the business level Θ lead to big fluctuations on the required agents number Vi for each period i, this results that the under-staffing cost varies a lot for a given staffing level. With a big email workload seize W , we draw an interesting remark that both the under-staffing costs and the associated stds are decreasing. This is related with the event that after blending, the optimal staffing levels increase by small number comparing to the case we had no emails or a small amount of emails. These additional agents, even with a small number, would indeed help us in case of a high volume of unpredicted demand of calls. Then we conclude that combining the demand of calls with a relatively high workload of emails protects us from calls arrival rate uncertainty. We can see that the relative std of the total cost (total cost std/average total cost) decreases when W increases. As a conclusion, the flexibility offered by emails may

Std3 0 442.57 0 442.57

allow us to efficiently behave against the undesirable seasonality of a day demand of calls, and to lighten the uncertainty in the parameters of this demand. And the combination of calls and emails workload may make big saving on the total operating cost. 5

Conclusions and Future Research

We have developed a multi-shift call center model which handles two types of jobs: calls and emails. We focused on optimizing the staffing level subject to minimizing the total operating cost of the call center. We modelled this problem as a cost optimizationbased newsboy-type model. We then propose different approaches to numerically solve it: The classic stochastic programming approach, the stochastic programming approach with risk aversion and the robust optimization approach. We next conducted a numerical study in order to evaluate the performance of the approaches and gain useful insights. First, by comparing with the deterministic approach, we underlined the necessity of taking into account the uncertainty in the call demand parameters, which is not often the case in most exiting studies. Second, we evaluated the two approaches and point out the efficiency of robust optimization approach. Third, we showed that profiting from the flexibility of the email job (because they are storable) helps us to mitigate the effect of the uncertainty in the call demand. In next step, we want to extend the analysis of this paper to a global service level which is a non-linear problem. We will employ some method to linearize this problem accurately by paying a price of adding many variables. This would make it very difficult for the stochastic programming approach to solve it, but the robust optimization approach may offer some interesting results. REFERENCES Avramidis, A., Deslauriers, A., and L’Ecuyer, P. (2004). Modeling Daily Arrivals to a Telephone Call Center. Management Science, 50. Bertsimas, D. and Brown, D. (2005). Robust Linear Optimization and Coherent Risk Measures. Working paper. Massachusetts Institute of Technology. Bertsimas, D. and Doan, X. (2008). Robust and Data-

MOSIM’10 - May 10-12, 2010 - Hammamet - Tunisia

Driven Approaches to Call Centers. Working Paper, Operations Research Center, MIT. Bertsimas, D. and Sim, M. (2004). The Price of Robustness. Operations Research, 52:35–53. Brown, L., Mandelbaum, A., Sakov, A., Shen, H., Zeltyn, S., and Zhao, L. (2002). Multifactor Poisson and Gamma-Poisson Models for Call Center Arrival Times. Technical report, University of Pennsylvania. Gans, N., Koole, G., and Mandelbaum, A. (2003). Telephone Calls Centers: a Tutorial and Literature Review and Research Prospects. Manufacturing and Service Operations Management, 5:79–141. Gans, N., Shen, H., and Zhou, Y. (2009). Parametric Stochastic Programming Models for Call-Center Workforce Scheduling. working paper. Gothoh, J. and Tankano, Y. (2007). Newsvendor Solutions Via conditional Value-at-risk Minimization. European Journal of Operational Research, 179:80– 96. Gurvich, I., Luedtke, J., and Tezcan, T. (2009). Staffing Call-Centers With Uncertain Demand Forecasts: A Chance-Constraints Approach. working paper.

Robbins, T., Medeiros, D., and Harrison, T. (2008). Optimal Cross Training in Call Centers with Uncertain Arrivals and Global Service Level Agreements. Working paper. Pennsylvania State University. Rockafellar, T. and Uryasev, S. (2002). Conditional Value-at-risk for General Loss Distributions. Journal of Banking and Finance, 26:1443–1471. Shen, H. and Huang, J. (2008). Interday Forecasting and Intraday Updating of Call Center Arrivals. Manufacturing and Service Operations Management, 10:391–410. Steckley, S., Henderson, S., and Mehrotra, V. (2004). Service System Planning in The Presence of A Random Arrival Rate. Technical report, Cornell University, Ithaca, NY. Thenie, J., van Delft, C., and Vial, J. (2007). Automatic Formulation of Stochastic Programs Via an Algebraic Modeling Language. Computational Management Science, 4:17–40. van Delft, C. and Vial, J. (2004). A Practical Implementation of stochastic Programming: An Applications to the Evaluation of Option Contracts in Supply Chains. Automatica, 40:743–756.

Harrison, J. and Zeevi, A. (2005). A Method for Staffing Large Call Centers Based on Stochastic Fluid Models. Manufacturing and Service Management, 7:20–36.

van Delft, C. and Vial, J. (2009). Apractical Implementation of Stochastic Programming: an Application to The Evaluation of Option Contracts in Supply Chains. Preprint submitted to Automatica.

Jongbloed, G. and Koole, G. (2001). Managing Uncertainty in Call Centers Using Poisson Mixtures. Applied Stochastic Models in Business and Industry, 17:307–318.

Whitt, W. (1999). Dynamic Staffng in a Telephone Call Center Aiming to Immediately Answer all Calls. Operations Research Letters, 24:205–212.

Liao, S., Van Delft, C., Koole, G., and Jouini, O. (2009). Staffing a Blending Call Center with Uncertain Arrival Rates. Working paper. Ecole Centrale Paris. Mehrotra, V., Ozluk, O., and Saltzman, R. (2009). Intelligent Procedures for Intra-day Updating of Call Center Agent Schedules. To appear in Production Operations Management. Ogryczak, W. and Ruszczynski, A. (2002). Dual Stochastic Dominance and Related Meancrisk Models. SIAM Journal on Optimization, 13:60–78. Robbins, T. (2007). Managing Service Capacity Under Uncertainty. Ph.D. Dissertation, Penn State University. Robbins, T. and Harrison, T. (2008). A Stochastic Programming Model for Scheduling Call Centers with Global Service Level Agreements. Working paper. Pennsylvania State University.

Whitt, W. (2006). Staffing a Call Center with Uncertain Arrival Rate and Absenteeism. Production and Operations Management, 15:88–102.