Afro-Asian J. Finance and Accounting, Vol. 2, No. 2, 2010

135

The implementation of activity-based costing and the financial performance of the Jordanian industrial shareholding companies Husam Aldeen Al-Khadash* Hashemite University, P.O. Box 330125, Zarqa 13133, Jordan E-mail:

[email protected] *Corresponding author

Mahmoud Nassar Accounting Department, Applied Science Private University Amman, P.O. Box 926296, Amman 11931, Jordan E-mail:

[email protected] Abstract: The purpose of this study is to investigate the improvement in financial performance associated with the use of activity-based costing (ABC). Data were obtained through a cross-sectional mail survey of financial managers who furnished information regarding company financial performance, the extent of ABC usage, and the enabling conditions that have been identified in the literature as affecting ABC efficacy. Data were obtained from the Jordanian shareholding companies as of the end of 2009. Regression analysis is used to test the association between the awareness level of using ABC and the level of adopting ABC. It is also used to identify the improvement in ROA as a mean of financial performance which associated with ABC initiatives. Results show that the awareness level of using ABC is high among the financial managers, but ABC implementation is not high; also it is found that there is a positive association between ABC and improvement in ROA. Keywords: improvement in financial performance; ABC success; structural equation models; Jordan; activity-based costing; ABC. Reference to this paper should be made as follows: Al-Khadash, H.A. and Nassar, M. (2010) ‘The implementation of activity-based costing and the financial performance of the Jordanian industrial shareholding companies’, Afro-Asian J. Finance and Accounting, Vol. 2, No. 2, pp.135–153. Biographical notes: Husam Al-Khadash is an Associate Professor of Accounting. He graduated from Western Sydney University, Australia. He specialises in accounting theory and his research interest is in accounting education, accounting theory and auditing. He has over 20 published papers and five textbooks, and has over 16 years of teaching experience in Jordan and Australia. Mahmoud Nassar obtained his MA in Accounting in 2005. In 2010, he received his PhD in Accounting from the University of Wales, Newport. His main research interests include cost accounting systems, survey design and analysis. He has developed close links with a wide variety of industries in the Jordan undertaking a number research survey projects in the area of cost accounting and analysis.

Copyright © 2010 Inderscience Enterprises Ltd.

136

1

H.A. Al-Khadash and M. Nassar

Introduction

In the late 1980s, activity-based costing (ABC) gained the attention of academic researchers and managers as a means of overcoming the disadvantage of traditional cost accounting (TCA) (Roztocki and Schultz, 2005). The TCA methods were actually misleading decision makers, causing them to make decisions inconsistent with their organisations’ needs and goals, principally because of misallocated costs (Kaplan and Anderson, 2004). Cost accounting had traditionally allocated overhead to products or services using only one volume-based allocation, typically direct labour. For organisations with high overhead and a mix of products or services, using a single cost driver may distort cost estimates (Cooper, 1987; Cooper and Kaplan, 1988). These traditional costing systems tend to distort product costs and lead to poor strategic decision-making (Johnson, 1992). Owing to the impact of technology and the diversity of products and services, TCA lacks the degree of accuracy necessary to properly identify cost product. Incorrect costing can distort the real situation and create problems with pricing and allocation decision. So the need for a new system that overcomes those problems has pushed researchers to improve models of ABC smooth implementation (Johnson, 1992). ABC is a valuable concept that can be used to correct the shortcomings in the cost systems of the past (Cooper and Kaplan, 1991). A movement from TCA methods to ABC was seen as a great advancement for companies which were striving to gain control and better manage indirect or overhead cost. This motivated companies to take initiatives in implementing ABC which lead them toward long-term competitiveness and profitability (Roztocki and Needy, 1999). Although ABC has found rapid and wide acceptance, there is significant diversity of opinions regarding the efficiency of ABC (McGowan and Klammer, 1997). And there is still no significant body of empirical evidence to validate the alleged benefits of ABC (Shim and Stagliano, 1997; McGowan and Klammer, 1997). Empirical research is needed to document the (financial) consequences of ABC implementation (Kennedy and Bull, 2000). Accordingly, the aims of this study are to investigate the extent of using ABC in the industrial Jordanian companies and to investigate the extent of financial managers’ awareness of the importance underlying the implementation of the ABC. Empirical research on the efficacy of ABC has generally concentrated on identifying successful ABC systems and modelling the factors that lead to this success. Success has been defined as ‘use for decision-making’ (Innes and Mitchell, 1995; Krumwiede, 1998; Anderson and Young, 1999), ‘satisfaction’ with the costing system (Shields, 1995; Swenson, 1995; McGowan and Klammer, 1997), perceived financial benefit, but there is limited empirical evidence about investigating the relationship between the implementation of ABC and organisation performance. Most of the previous studies have focused on three points when investigate ABC implementation: Successful implementation of ABC; the benefits of ABC implementation; and the effects of the environment on the successful implementation of ABC. The current study will attempt to focus on this important relation between implementation of ABC and organisation performance. In sum, the present study aims at filling the gap in our literature concerning the case of using strategic management initiatives specially ABC, and investigating its

The implementation of activity-based costing and the financial performance 137 impact on organisation performance. Few attempts have been found in terms of developing countries including Jordan. Under this reality, many researchers concluded that most of strategic management practice survey and literature have focused on developed countries. Therefore, the important principle of this study is to provide evidence about the extent of using ABC and investigating its impact on the organisation performance in industrial Jordanian companies. It does so by investigating four research questions: 1

To what extent is the ABC system applied in Jordanian industrial shareholding companies according to financial managers’ perceptions?

2

Are the financial managers of industrial Jordanian shareholding companies familiar with the benefits of ABC?

3

Is there a significant relationship between the financial mangers’ familiarity with the ABC and the adoption of the ABC?

4

Is there a significant relationship between adopting the ABC and the profitability of Jordanian industrial shareholding companies?

2

Literature review

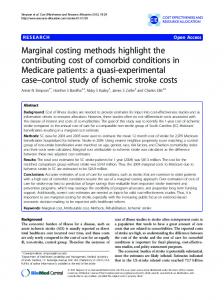

2.1 Distinguishing between TCS and ABC systems Drury (2004) claimed that both TCS and ABC systems rely on what has become known as the two-stage allocation process. In the first stage TCS assigns indirect costs to cost centres (normally departments), whereas ABC systems assign costs to each major activity centre rather than departments. Hence, the first distinguishing feature between the two systems is that ABC systems assign costs to a greater number of first-stage cost centres (i.e., cost pools) (Homburg, 2001). The second stage allocates costs from the cost centres to cost objects (products/services). TCS allocates indirect costs to cost objects using a small number of allocation bases/cost drivers that tend to vary directly with the volume produced. Direct labour hours/cost and machine hours are the allocation bases that are mostly used by TCS. In contrast, ABC systems use many second-stage cost drivers, including drivers that do not vary directly with volume produced. Examples include the number of production runs and the number of purchasing orders for allocating the costs of production scheduling and purchasing to cost objects respectively (Horngren et al., 2003). The ABC systems focus on the accurate cost assignment of overheads to products. In the cost assignment view, the assignment of costs through ABC occurs in two stages as shown in Figure 1: cost objects (i.e., products or services) consume activities, activities consume resource costs. In practice, this means that resource costs are assigned to various activity centres by using resource drivers in the first stage. An activity centre is composed of a group of related activities, usually defined by function or process. The group of resource drivers is the factor chosen to estimate the consumption of resources by the activities in the activity centres. Every type of resource assigned to an activity centre becomes a cost element in an activity cost pool. And, in the second stage, each activity

138

H.A. Al-Khadash and M. Nassar

cost is distributed to cost objects by using a suitable activity driver to measure the consumption of activities by products or services (Turney and Anderson, 1989). Then, the total cost can be calculated by adding the various activities costs to a specific product or service. And the total cost divided by the quantity of the product can acquire the unit cost of product. Figure 1

ABC model

2.2 Empirical studies relating to determine the implementation rate of ABC systems In the USA, UK, Australia, Greece and Ireland, for example, surveys between the early 1990s and 2007 have indicated an increasing extent of ABC adoption in each of these countries. In this regard, the extent of ABC adoption of a broad range of US companies has increased from 25% to 52% and that of UK companies has increased from 6% to 23%. Manufacturing firms in Ireland increased their ABC adoption from 12% to 34.9%, while Australian manufacturing firm adoption levels rose from 12% to 56% (Sartorius et al 2007). A summary of these surveys is shown in Table 1.

The implementation of activity-based costing and the financial performance 139 Table 1

Summaries the ABC implementation rate

Year

Country

Survey

Implementation rate

1990

UK

Innes and Mitchell (1991), members of the CIMA

6% began to implement ABC

1991

Sweden

Ask and Ax (1992), engineering Industry

2% are applying ABC

1990

UK

Davies et al. (1992), manufactures

32% are applying ABC

1991

UK

Nicholls (1992), 178 companies that attended an ABC seminar in May 1990

10% had implemented ABC

1992

Canada

Armitage and Nicholson (1993), financial post list of 700 largest companies in Canada

14% are applying ABC

1994

UK

Yakhou and Dorweiler’s (1995)

48% of respondent companies in the U.K. were using ABC

1994

UK

Innes and Mitchell (1995), firms listed in TIME 1000

20% consider ABC applicable to their organisations (only 8% used it extensively)

1995

USA

Shim and Sudit (1995), US Fortune 1,000 companies

25% had implemented ABC

1995

Australia

Booth and Giacobbe (1997), Australian manufacturing companies

12% of 213 respondent companies had adopted ABC

1997

Singapore

Chung et al. (1997), Singapore companies

(4%-21%) were still at the early stages of ABC implementation

1997

Australia

Nguyen and Brooks (1997), Australian manufacturing companies

12.5% of 120 respondent companies in the State of Victoria in Australia were using ABC

1998

Australia

Chenhall and Langfield-Smith (1998), manufacturing firms

56% had implemented ABC

1999

Ireland

Clarke et al (1999), manufacturing industry

12% had implemented ABC, 20% were assessing it and 13% had rejected

2003

USA

Kiani and Sangeladji (2003), largest 500 US industrial companies

52% had implemented ABC

2003

Greek

Cohen et al (2005), 88 leading companies

40.9% (36 companies) are adopters ABC. And 59.1% (52 companies) are non-ABC adopters

2004

Ireland

Pierce and Brown (2004), manufacturing firms

Manufacturing firms had implemented ABC 34.9% Services firms had implemented ABC 17.8% Financial firms had implemented ABC 28.6%

2007

South Africa

Sartorius et al (2007), companies listed on the Johannesburg Securities Exchange (JSE)

12% of 181 respondent companies had implemented ABC

140

H.A. Al-Khadash and M. Nassar

2.3 Empirical studies relating to benefits of ABC It is claimed that ABC provides many significant benefits over TCS, such as enhanced product cost accuracy, more comprehensive cost information for performance measurement, more pertinent data for management decision-making, increased potential for sensitivity analysis, and a model for value-adding organisational transactions and activities (Kaplan and Anderson, 2004; Innes and Mitchell, 1995; Chung et al., 1997). Innes and Mitchell (1991) argue that ABC provides more relevant product costs leading to more accurate costs reflecting total overhead costs associated with the product. They also indicate that ABC is providing better product and pricing strategies through the availability of more realistic information on product profitability. It is also claimed that ABC information is useful for managers in the processes of budgeting and performance measurement (Kaplan and Anderson, 2004; Innes and Mitchell, 1995). Moreover, several studies (Innes and Mitchell, 1995; Nicholls, 1992; Sartorius et al., 2007) report that the key areas of ABC benefits are cost control and cost reduction, as well as improved profitability. Finally, Innes and Mitchell (1991), Booth and Giacobbe (1997) and Chung et al. (1997), argue that ABC is a significant source of information for decision-making about product costs and product-line profitability. Innes and Mitchell (1991) also claim that accurate product costs are critical to pricing decisions, new product introductions, decisions to drop out-of-date products as well as decisions on how to respond to the products of competitors correctly and on time. This is because product costs identify causes of resource consumption and ways of saving resources, especially at the product and process design stage (Chung et al., 1997).

2.4 Empirical studies relating to examine the association between ABC and improvement in financial performance The theories of diffusion of innovations (Kwon and Zmud, 1987), transaction cost economics (Roberts and Sylvester, 1996) suggest that organisations adopt an innovation to obtain benefits that directly or indirectly affect financial performance measures. There have been numerous claims and counterclaims, rarely supported by objective and rigorous empirical evidence, regarding whether programs have yielded net financial gains. Balakrishnan et al. (1996) pointed out in their discussion of management strategic initiatives, that a firm’s pre-adoption operating efficiency will influence its ROA response to the increased efficiency of initiatives use. Some researchers have been successful in detecting a link between use of ABC and improvement in financial performance in specific business environments. Kennedy and Afleck-Graves (2001) were successful in linking the implementation of ABC with a net improvement in financial performance in manufacturers; however, Cagwin and Bouwman (2002) found that ABCs contribution was an indirect, rather than a direct effect on improvement in financial performance. Cagwin and Bouwman (2002) investigated the improvement of financial performance that is associated with the use of ABC, and the conditions that are associated with improvement of financial performance. They used confirmatory factor analysis and structural equation modelling to investigate the relationship between ABC and improvement in financial performance. This study suggested a positive association between ABC and improved return on investment (ROI) when ABC is used concurrently

The implementation of activity-based costing and the financial performance 141 with other strategic initiatives, when implemented in complexes and diverse firms, when used in environments where costs are relatively important, and when there are limited numbers of intra-company transactions.

2.5 ABC in the Jordanian industrial sector ABC is a new cost accounting system in the Jordanian industrial sector (Al-Khadash and Feridun, 2006). It is known by Jordanian academics who have studied abroad since the early 1990s (Hutaibat, 2005) and first appeared in Jordanian literature in the early 1990s and thereafter began to be discussed. However, these discussions tended to stay at the conceptual and theoretical levels and there were not any sufficient or comprehensive studies about its application at that time. In the mid-1990s and early 2000s, ABC was widely discussed in Jordan through seminars, conferences and journals (Khasharmeh, 2002). The consideration of ABC by companies in the Jordanian industrial sector first occurred as a result of parent company policies in the USA or the UK (Hutaibat, 2005; Arafat, 2002). The first study to examine the level of ABC implementation in the Jordanian industrial sector was carried out by Khasharmeh (2002). His study population consists of all the Jordanian Industrial Shareholding Companies that were listed on the Amman Stock Exchange at the end of 2001 (40 companies). According to his result 4 of 40 companies of the Jordanian manufacturing companies use the ABC system (implementation levels of ABC is about 10%). The second study carried out by Al-Khadash and Feridun (2006) aimed to investigate the link between the practice of ABC, just in time (JIT) and total quality management (TQM) as management accounting innovations and the improvement in corporate financial performance of 56 industrial shareholding companies. The study population consists of all the Jordanian Industrial Shareholding Companies that are listed at Amman Stock Exchange at the end of 2003. Telephone interviews were conducted with all industrial companies (56 companies in total) to identify those companies that applied the management accounting innovation. It was found that six companies had implemented ABC. It should be note that both studies do not segment ABC to stages. Al-Ghazzawi’s (2003) study investigates the role of the ABC system in production policies, and the improvement of profitability of Jordanian industrial corporations. It seeks to identify the reasons which necessitate the use of the ABC system. The study concluded that the industrial corporations applying the ABC lack accuracy in selecting and determining cost drivers, the policies of production were affected by the applications of the ABC by a percentage of 73%. Moreover the application of the ABC had an effect on the profitability and revenues of industrial corporations by a percentage of 72%. Also Nassar et al. (2009) determined the extent of ABC implementation within the Jordanian industrial sector and identified the factors that facilitate and motivate the decision to implement ABC. The implementation process is segment by stages: considering, analysis, approved for implementation and used extensively. Additional objective includes assessing the degree of success of ABC implementation. The survey findings indicate that ABC implementation among the Jordanian industrial companies is quite satisfactory. The rate of ABC implementation is about 55.7%. The most cited factors that facilitate the decision to implement ABC were that adequate training was provided for designing ABC and operating data in the information system are updated in

142

H.A. Al-Khadash and M. Nassar

real time: followed by the fact that adequate training was provided for using ABC. The most influential factors that motivate the process of ABC implementation are among others the increasing proportion of overhead costs, growing costs, including product costs and administrative costs, and currently the increasing number of product variants.

3

Research methodology and data collection methods

3.1 Population of study The Jordanian industrial sector is viewed as one of the economic sectors that Jordan should develop if it is to achieve better economic growth (Central Bank of Jordan, 2007). It is mainly built upon three industries: manufacturing, electricity production, and mining. Companies in these three sectors are largely privately owned and are mostly small and medium-sized (Hutaibat, 2005). The overall contribution of the industrial sector to the Jordanian GDP for the year 2005 was approximately 17 per cent. In the same year, the value of industrial exports was about (2,379) JD million (1JD = £1). Industrial sector exports contributed about 93.5% of the national exports. The total number of industrial establishments reached 21,000, employing more than 173,000 workers. This figure represents about 48% of the total number of workers in Jordan (Ministry of Planning Report, 2007). By the beginning of the 1990s, Jordan’s accession to the World Trade Organisation (WTO), and signing of free-trade agreements with a number of different parties, meant that it had become a fertile ground for its industrial production to grow and expand (Central Bank of Jordan, 2007). The country’s industrial production index comprised of 77% in manufacturing production, 15% in mining, and 8% in electricity production (Goussous, 2002). Following Jordan’s joining of these global bodies, an urgent need was identified to develop all Jordanian economic sectors, especially the industrial sector, so that it might operate successfully in a free market economy (Ministry of Planning Report, 2007). The industrial sector grew to nearly 21% of GDP by 2006, in large part as a result of the USA – Jordan Free Trade Agreement (ratified in 2001 by the US Senate). This agreement led to the establishment of 13 qualifying industrial zones (QIZs) throughout the country (Ministry of Planning Report, 2007). The QIZs, which provide duty-free access to the US market, produce mostly light industrial products, especially ready-made garments. By 2006 the QIZs accounted for nearly US$1.1 billion in exports (Ministry of Planning Report, 2007). As more multinational companies establish joint ventures or regional offices in Jordan, it is expected that changes will occur to management accounting practices. These changes will be driven by the need for Jordanian companies to implement cost accounting innovations in order to compete more effectively. This study focuses on the Jordanian industrial sector for three reasons: 1

The researchers had extensive familiarity with and experience of cost accounting systems in Jordanian industrial companies.

2

There is a clear trend in the social and economic development plans of successive Jordanian governments to support the industrial sector. Recently, this has been one of the central reoccupations of the government and industry alike. The primary aim

The implementation of activity-based costing and the financial performance 143 of such a policy must be to provide a clear sense of direction by carefully identifying the priorities and by paying equal attention to both the developments of the internal capabilities of industrial companies as well as providing the necessary environment and conditions for industrialisation (Central Bank of Jordan, 2007). Such a policy should position Jordanian companies so that they can develop and compete in international markets and meet the expected challenges and opportunities for growth, especially now that, in the last few years, Jordan has undertaken major steps on its path to enter international markets. 3

Industrial companies are exposed to changes in the industrial environment such as changes in the production cost structure (Innes and Mitchell, 1991; Askarany, 2006) and new high technological manufacturing techniques (Clarke et al., 1999). Due to these changes, industrial companies are also commonly associated with implementing cost accounting innovations.

The population of the study consisted of Jordanian Industrial Shareholding Companies listed on the Amman Stock Exchange at the end of 2009. The total number of companies included was 67, and phone calls were made to all these listed industrial companies to identify those companies which applied the ABC. Out of the total two companies did not cooperate, so at the end 65 companies were investigated. These companies were selected as the arena for this study for two reasons: 1

the industrial companies sector is one of the largest sectors listed on the Amman Stock Exchange

2

a great deal of data about the industrial shareholding companies are available from the Amman Stock Exchange.

3.2 Methods of data collecting A survey instrument was developed to collect data to provide evidence about the current status of ABC implementation. As part of a strategy to develop an accurate mailing list and secure a high response rate, a phone call was lodged with each company and the name of the most suitable person to complete the survey was identified. These were typically the chief accountant, chief controller, or chief financial officer. In most cases, the particular manager was spoken to and the purpose of the research explained. The mailed survey package included a covering letter explaining the purpose of the research, a copy of the survey with a glossary of terms used. The survey included demographic questions about the respondent’s position in the organisation and experience, age and education. Respondents were also asked about their familiarity with ABC and about the cost systems presently in use in their companies and the methods used to apply the overheads. Careful attention is given to making sure that the wording of each question is clear, concise and described only one concept. The questionnaire of this study is intended to measure the extent to which industrial companies are implementing ABC initiative along with the extent of the financial managers’ belief in the importance of such use, and their familiarity with ABC. The main parts of the questionnaire are as follows: Part One collects demographic questions about the respondent’s and their companies. Part two seeks to find out the extent of using the ABC and the respondent’s belief in the importance of using such

144

H.A. Al-Khadash and M. Nassar

initiative. Part Three aims to measure the degree of financial managers’ familiarity with ABC. It is noteworthy to point out that answers to questions in parts two and three have been worded by using Likert scale for measuring degrees of agreements. So, five answers have been given to determine the extent of responses (i.e., extremely large, large, medium, little and very little). Also annual reports of 2009 were used to collect information about the ROA in order to test to what extent the initiatives are related to the level of financial performance (ROA).

3.3 Methods of data analysis For the purpose of analysing the data and testing the hypotheses, the current study used the descriptive statistical analysis such as the mean and the standard deviation; also simple regression analysis is used to test the association between the level of familiarity of using the ABC and the level of implementing this initiative. Also it is used to test the improvement in ROA as a mean of financial performance which associated with the using of ABC.

4

Results

4.1 Characteristics of the study sample The following part of the study is a description of the analysis of the sample characteristics. Table 2 shows that all respondents were financial managers with a percentage of 100%. It also indicates that the maximum percentage (41.5%) of the respondents was located in the category of (11–15) years of experience, and the minimum percentage (7.7%) has less than five years of experience. Consequently, the majority of financial managers of the study sample are with high level of experience. Table 5 indicates that (41.5%) of the respondents were located in the category of 41–50 years old (i.e., 27 out of 65), and (6.2%) of the respondents are less than 30 years old (i.e., 4 out of 65). Furthermore it shows that (76.9%) of the respondents have bachelor degrees, followed by nearly (21.6%) of the respondents have a master degree. Also the table indicates that (87.7%) of the respondents do not have professional certificates: this might be as a result of the new launching of the only local professional certificate, Jordanian Certified Public Accountant (JCPA) in Jordan in 2003. In the future this percent might be decreased as JCPA becomes more popular in Jordan. Moreover, the Jordanian universities have the responsibility to equip their students with the necessary skills to help in this area. Table 3, about the main cost accounting systems used, shows that 6.2% of the industrial Jordanian shareholding companies are not implementing any cost calculation, they just use a manual financial accounting system and do not have any records for any cost calculation. Also 24.6% of these companies calculate their product cost based on standard costing, they use judgment to value the work in process inventory end of the financial period without having a system to record the actual costs. Job-order costing systems and process costing systems are the main cost accounting techniques used with a total percentage of 60. The ABC system is not used mainly in the Jordanian companies for cost calculation, the percentage of the companies using such a system is 9.2%.

The implementation of activity-based costing and the financial performance 145 Consequently, it has to be mentioned that most of the companies have some costing systems. Table 2

Characteristics of the respondents

Position Financial manager

Frequency

Percent

65

100.0

Years of experience Less than five years

5

7.7

6–10 years

14

21.6

11–15 years

27

41.5

16 years and more

19

29.2

Total

65

100.0

Age Less than 30 years

4

6.2

30–40 years

20

30.8

41–50 years

27

41.5

51 years and more

14

21.5

Total

65

100.0

1

1.5

Bachelor

50

76.9

Master

14

21.6

Total

65

100.0

CPA

1

1.6

JCPA

4

6.1

CMA

3

4.6

No professional certificates

57

87.7

Total

65

100.0

Level of education Diploma or below

Professional certificates in accounting

Table 3

Characteristics of companies under investigation

The main cost accounting techniques used

Frequency

Percent

None Standard costing

4 16

6.2 24.6

Job order costing system

15

23.0

Process costing system

24

36.9

ABC system

6

9.2

Total

65

100.0

Also some information is collected to know the most common bases used to apply overhead to cost objects. Table 4 shows that the maximum percentage (44.6%) was linked to the number of units’ base, 29 companies were used this base. Also eight more

146

H.A. Al-Khadash and M. Nassar

companies used the number of units’ base associated with some other bases such as direct hours and machine hours. Table 4

Bases to used to apply overhead costs

Bases (cost drivers)

Frequency

Percent

Direct hours

6

9.2

Machines hours

2

3.1

Direct materials

6

9.2

Number of units

29

44.6

Direct hours and machines hours

2

3.1

Direct hours and number of units

6

9.2

Machines hours and number of units

2

3.1

None

4

6.1

Use all of them

8

12.3

Total

65

100.0

4.2 Survey results Results are reported below for each of the research questions. 1

To what extent is the ABC system applied in Jordanian industrial shareholding companies according to financial managers’ perceptions?

As presented previously in Table 3, 9.2% of the investigated companies mentioned that they use the ABC system. The following Table 5 shows the level of implementation of ABC based on Brown et al. (2004) categories. Table 5

Level of ABC implementation

Description ABC has not been known. And the management use another systems in costing or do not use any ABC is being known and implementation is possible but implementation has not been approved Approval has been granted to implement the ABC, but analysis has not yet begun ABC implementation team is in the process of determining project scope and objectives, collecting data, and/or analysing activities and cost drivers Analysis is complete and ABC model has been implemented, but ABC information is not yet used outside of accounting department for decision making ABC is applied in the company and the information is used for decision making Total

Frequency

Percent

A

Not considered

Stage

34

52%

B

Considering

13

20%

C

Approved for implementation Starting analysis

8

12%

3

5%

E

Implemented and used some what

3

5%

F

Used extensively

3

5%

65

100.0

D

The implementation of activity-based costing and the financial performance 147 Table 5 pointed out that 48% of the respondents had some knowledge about the ABC concepts. 20% of the sample is currently considering the implementation of the ABC system. 12% of the respondents approved the need for the ABC system but the system is still not in use yet. 5% of the respondents begin the analysis process as an introduction to apply the ABC system. 10% of the respondents are currently using the ABC system, i.e., six companies. Consequently, this study concludes that the rate of ABC diffusion within the Jordanian industrial sectors is about 15% (10% had fully implemented the ABC system plus 5% of the companies are in the process of implementing the ABC). In Jordan there has been a growing interest into the implementation of the ABC, Al-Khadash and Feridun (2006) pointed out that the awareness level of the importance of implementing ABC is found to be significantly high among the Jordanian financial managers. This evidence combines to support and explain the increase level of awareness of ABC implementation within the Jordanian Industrial sector in the last six years (Al-Khadash and Feridun, 2006). 2

Are the financial managers of industrial Jordanian shareholding companies familiar with the benefits of ABC?

The questionnaire also included questions about financial managers’ familiarity with the benefits that would be gained from the adoption of the ABC. This question was ranked on a five-point scale (1 = strongly disagree and 5 = strongly agree). As indicated in Table 6 that there is good familiarity with the ABC system, because the mean scores are above of 3 for all answers. Results also showed that the major objectives of the ABC adoption were to improve planning process (mean scores = 4.26) as well as to improve the decision making quality (mean scores = 4.23). Table 6

Descriptive statistics of the financial managers’ familiarity with ABC

ABC improves the planning process

Minimum

Maximum

Mean

Std. deviation

3

5

4.26

.50

ABC improves the decision making quality

3

5

4.23

.54

ABC provides information about the best mix of products

2

5

4.15

.63

ABC system increases the service in different levels of management

3

5

4.15

.59

ABC enhance the cost control improvement

3

5

4.13

.58

ABC leads to better performance measurement

3

5

4.13

.66

ABC leads to better method in overhead costs allocations

3

5

4.00

.73

ABC improves the profitability

3

5

3.97

.63

ABC assists in cost reduction efforts

2

5

3.95

.69

ABC makes more accurate product/service costs

3

5

3.95

.65

ABC assists in product/service design

1

5

3.90

.88

ABC increases the effectiveness of budget by identifying relationships between costs and activities

3

5

3.82

.65

148

H.A. Al-Khadash and M. Nassar

In addition, the ABC system provides information about the best mix of products (mean scores = 4.15), the ABC system serves different levels of management (mean scores = 4.15), enhance the cost control improvement (mean scores = 4.13), leads to better performance measurement (mean scores = 4.13), leads to better method in overhead costs allocations (mean scores = 4.00). All of the above objectives are regarded by respondents as important goals for adopting the ABC. These results indicate that the financial managers are aware of the importance of applying the ABC system. Consequently and based on the results shown in Table 6 it might be concluded that financial managers of Industrial Jordanian Shareholding Companies are familiar enough with the benefits and importance of using the ABC. 3

Is there a significant relationship between the financial managers’ familiarity with the ABC and the adoption of the ABC?

This section comes to test if there is any association between the ABC implementation and financial managers’ familiarity with ABC. It might be argued that if the managers are familiar and aware enough to the importance of using such initiative, so the level of practicing it is higher in comparison with a case of lower level of awareness. Consequently, testing of research question number three is achieved through estimation of the following regression model: ABCit = a + AABCit + eit,

(1)

where ABCit

represents the level of adopting the ABC (the dependent variable, it, is measured using two-point scale yes or no)

AABCit

represents the financial managers’ familiarity with the importance of using the ABC (the independent variable, it, is measured using Likert-type scale 5: extremely familiar and 1: not at all familiar)

eit

represents the unexplained error of the regression model utilised.

As shown in Table 7 the suggested regression model was significant at the level of .05. This result confirms that there is a relationship between financial managers’ familiarity with ABC and the level of adopting the ABC in Industrial Jordanian Shareholding Companies. This result gives an indicator that a high level of familiarity and awareness with the ABC initiative is associated with a real practice of the ABC, an expected explanation for such results might be that while financial managers are familiar with the ABC and aware enough to the importance of using the ABC initiative, they influence the decision makers, to take a real action toward adopting this initiative. Table 7

ABC implementation and the financial managers’ familiarity with the ABC

Regression model Regression model 1 (ABC)

4

Adjusted R2

F

Sig.

.253

5.089

.046

Is there a significant relationship between adopting the ABC and the profitability of Jordanian industrial shareholding companies?

Testing of research question number four is achieved through estimation of the following regression model:

The implementation of activity-based costing and the financial performance 149 ROAit = ABCit + eit,

(2)

where ROAit represents the change on return on assets ( the dependent variable, the ROA used is the simply reported return on assets) ABCit represents the level of adopting the ABC (the independent variable) eit

represents the unexplained error of the regression model utilised.

Based on the figures shown in Table 8 and Table 9 the result of testing the association shows a significant relationship between financial performance and the level of implementing the ABC, so it might be argued that the level of using ABC has a positive effect with the financial performance. This confirms the results of the previous studies which found a significant positive association between the use of management initiatives and improvement in financial performance. Table 8

The results of the regression model

F

152.73

p-value

0.000

R2

0.762

Adjusted R2

0.743

Coefficients (dependent variable: ROA)

T

Sig.

(Constant)

5.265

.000

ABC

2.590

.025

Table 9

Correlation Matrix of the study variables ROA

ABC

ROA

1.00

-

ABC

.265*

1.00

Notes: *Significant at α = 0.05 **Significant at α = 0.01

5

Discussions and conclusions

This paper investigated the improvement in financial performance that is associated with ABC use. The adoption of ABC has been researched extensively in developed countries. Research on these issues in Jordan in general and within the Jordanian industrial sector more specifically is limited. A quantitative methodology was adopted to evaluate the extent of ABC implementation. A personal questionnaire survey was employed to determine each stage for each company, then a secondary data was used to investigate whether the financial managers of the industrial Jordanian shareholding companies are aware of importance of using the ABC and whether such strategic initiative is associated with improvement in financial performance in the manufacturing sector or not. The primary goal of the firm is to achieve and improve financial profitability (Chenhall and

150

H.A. Al-Khadash and M. Nassar

Langfield-Smith, 1998) and it is vital that firms have empirical evidence of the effectiveness of strategic initiatives. The first finding was that the diffusion of ABC in the Jordanian industrial sector is quite satisfactory. The diffusion rate is 15%. The other finding is that positive synergies are obtained from the concurrent use of the ABC. The empirical evidence shows that the awareness level of the importance of using the ABC is high among the financial managers. Furthermore, it is found that there is a strong positive association between using ABC and improvement in financial performance. This finding is consistent with statements by researchers that management accounting systems are meant to be efficient in supporting firms’ operational effectiveness (Granlund and Lukka, 1998; Porter, 1996; Granlund, 1997). A primary purpose of initiatives is to improve this effectiveness and ABC is contributing in this regard. Some limitations should be noted when interpreting the results of this study. The limitations, however, present opportunities for future study. Firstly, the scope of the study is limited by the population which included only industrial Jordanian companies listed on the Amman stock exchange. This limitation may restrict the generalisability of the findings to only industrial shareholding companies. The findings of this study may have been different if a broader range of companies had been selected within the industrial sector. In addition, the results of this study may have been different if the sample had included the service sector and non-profit companies. Therefore, there is a need to find ways to increase the coverage of similar surveys so as to obtain a more comprehensive picture of Jordan company’ perceptions of ABC. Secondly, the number of companies in each category of ABC adoption and implementation was very small. Therefore, it was difficult to conduct meaningful statistical tests. The discussions concerning the adoption and implementation of ABC in this study mainly relied on description as the means to communicate the survey results. The results may have been different if the number of companies in each category had been higher and the number of ABC users had been larger. However, As a result of undertaking this research it is possible to identify several areas for future research. Further research in the Jordanian industrial sector is suggested in order to determine the factors that could motivate and facilitate the process to implement ABC and identify the barriers they could face during implementation process. Research that identifies the components of financial performance that are impacted by initiative use would be of benefit. Also additional statistics such as a factor analysis, or chi-square calculation might be used in analysing the data of a similar research paper in the future.

References Al-Ghazzawi, M. (2003) ‘The role of the ABC system in production policies, and the improvement of profitability of Jordanian industrial corporations’, Master’s thesis, Amman Arab University, Amman-Jordan. Al-Khadash, H. and Feridun, M. (2006) ‘Impact of strategic initiatives in management accounting on corporate financial performance: evidence from Amman Stock Exchange’, Managing Global Transitions, Vol. 4, No. 4, pp.299–313. Anderson, W. and Young, M. (1999) ‘The impact of contextual and process factors on the evaluation of activity-based costing systems’, Accounting Organizations and Society, Vol. 24, No. 7, pp.525–559.

The implementation of activity-based costing and the financial performance 151 Arafat, A. (2002) ‘Sector report: education. Jordan, research and studies’, Investment Banking Unit, Export and Finance Bank. Armitage, H. and Nicholson, R. (1993) ‘Activity-based costing: a survey of Canadian practice’, CMA Magazine, March, p.22. Ask, U. and Ax, C. (1992) ‘Trends in the development of product costing practices and techniques – a survey of the Swedish manufacturing industry’, The 15th Annual Congress of the European Accounting Association, Madrid, Spain, 22–24 April. Askarany, D. (2006) ‘Characteristics of adopters and organisational changes’, Thunderbird International Business Review, Vol. 48, No. 5, pp.705–725. Balakrishnan, R., Linsmeier, T. And Venkatachalam, M. (1996) ‘Financial benefits from JIT adoption: effects of customer concentration and cost structure’, The Accounting Review, April, pp.183–205. Booth, P. and Giacobbe, F. (1997) ‘Activity-based costing in Australia manufacturing firms: key survey findings’, Management Accounting Issues Report by the Management Accounting Centre of Excellence of ASCPA, Vol. 5, pp.1–6. Brown, D., Booth, P. and Glacobbe, F. (2004) ‘Technological and organizational influences on the adoption of activity-based costing in Australia’, Accounting and Finance, Vol. 44, No. 2, pp.329–356. Cagwin, D. and Bouwman, M.J. (2002) ‘The association between activity-based costing and improvement in financial performance’, Management Accounting Research, Vol. 13, No. 1, pp.1–39. Central Bank of Jordan (2007) Summary of Economic Development in 2006, available at http//www. cbj.gov.jo. Chenhall, R. and Langfield-Smith, K. (1998) ‘Adoption and benefits of management accounting practices: an Australian study’, Management Accounting Research, Vol. 9, No. 1, pp.1–19. Chung, L., Schochh, H. and Teoh, H. (1997) ‘Activity-based costing in Singapore: a synthesis of evidence and evaluation’, Accounting Research Journal, Vol. 10, No. 2, pp.125–141. Clarke, P.J., Hill, N.T. and Stevens, K. (1999) ‘Activity based costing in Ireland: barriers to, and opportunities, for change’, Critical Perspectives on Accounting, Vol. 10, No. 4, pp.443–68. Cohen, S., Venieris, G. and Kaimenaki, E. (2005) ‘ABC: adopters, supporters, deniers and unawares’, Managerial Auditing Journal, Vol. 20, No. 9, pp.981–1001. Cooper, R. (1987) ‘The two –stage procedure in cost accounting part one’, Journal of Cost Management, Vol. 1, No. 2, pp.43–51. Cooper, R. and Kaplan, R. (1988) ‘Measure costs right: make the right decisions’, Harvard Business Review, Vol. 66, No. 5, pp.96–105. Cooper, R. and Kaplan, R. (1991) ‘Profit priorities from activity –based costing’, Harvard Business Review, Vol. 12, No. 5, pp.130–135. Davies, B.J., Downes, C. and Sweeting, R. (1992) ‘The deployment of costing techniques and practices: a UK study’, Management Accounting Research, Vol. 3, pp.201–211. Drury, C. (2004) Management and Cost Accounting. 6th ed., Thomson, London. Goussous, R. (2002) ‘The Jordanian economy: building a solid future’, Country Report, Jordan, Investment Banking and Capital Markets, Export and Finance Bank. Granlund, M. (1997) ‘The challenge of management accounting change’, Doctoral Manuscript, Turku School of Economics and Business Administration. Granlund, M. and Lukka, K. (1998) ‘It’s a small world of management accounting practices’, Journal of Management Accounting Research, No. 10, pp.153–179. Homburg, C. (2001) ‘A note on optimal cost driver selection in ABC’, Journal of Management Accounting Research, Vol. 12, pp.197–205. Horngren, C., Datar, S. and Foster, G. (2003) Cost Accounting: A Managerial Emphasis, 11th ed., Prentice Hall International Inc, New Jersey.

152

H.A. Al-Khadash and M. Nassar

Hutaibat, K. (2005) ‘Management accounting practices in Jordan – a contingency approach’, Unpublished PhD thesis, Bristol University, Bristol. Innes, I. and Mitchell, F. (1991) ‘Activity based cost management: a case study of implementation’, CIMA, London. Innes, I. and Mitchell, F. (1995) ‘A survey of activity based costing in the UK’S largest companies’, Management Accounting Research, Vol. 6, No. 2, pp.53–137. Johnson, H. (1992) ‘It’s time to stop overselling activity-based concepts’, Management Accounting, September, pp.26–35. Kaplan, R. and Anderson, S. (2004) ‘Time-driven activity-based costing’, Harvard Business Review, Vol. 82, No. 1, pp.131–138. Kennedy, T. and Afleck-Graves, J. (2001) ‘The impact of activity-based costing techniques on firm performance’, Journal of Management Accounting Research, Vol. 13, pp.19–45. Kennedy, T. and Bull, R. (2000) ‘The great debate’, Management Accounting, Vol. 78, pp.32–33. Khasharmeh, H. (2002) ‘Activity –based costing in Jordanian manufacturing companies’, Derasat, Vol. 29, No. 1, pp.213–227. Kiani, M. and Sangeladji, M. (2003) ‘An empirical study about the use of ABC/ABM models by some of the fortune 500 largest industrial corporations in the USA’, Journal of American Academy of Business, Cambridge, Vol. 3, Nos. 1/2, pp.174–182. Krumwiede, K. (1998) ‘The implementation stages of activity- based costing and the impact of contextual and organizational factors’, Journal of Management Accounting Research, Vol. 10, pp.227–239. Kwon, T.H. and Zmud, R.W. (1987) ‘Unifying the fragmented models of information systems and implementation’, in R.J. Boland and R. Hirscheim (Eds.): Critical Issues in Information Systems Research, John Wiley & Sons, New York. Mcgowan, A.S. and Klammer, T. (1997) ‘Satisfaction with activity based cost management implementation’, Journal of Management Accounting Research, Vol. 9, pp.217–237. Ministry of Planning Report (2007) The Economic Indicators 2007, Amman, Jordan. Ministry of Planning Report (2007) The Economic Indicators 2007, available at http://www.mop.gov.jo/index.php. Nassar, M., Morris, D., Thomas, A. and Sangster, A. (2009) ‘An empirical study of activity-based costing (ABC) systems within the Jordanian industrial sector: critical success factors and barriers to ABC implementation’, Research in Accounting in Emerging Economies, Vol. 9, pp.229–263. Nguyen, H. and Brooks, A. (1997) ‘An empirical investigation of adoption issues relating to activity-based costing’, Asian Review of Accounting, Vol. 5, No. 1, pp.1–18. Nicholls, B. (1992) ABC ‘in the UK: a status report’, Management Accounting, May, pp.22–28. Pierce, B. and Brown, R. (2004) ‘An empirical study of activity based systems in Ireland’, The Irish Accounting Review, Vol. 11, No. 1, pp.55–61. Porter, M. (1996) ‘What is strategy?’, Harvard Business Review, Vol. 74, pp.61–78. Roberts, M. and Silvester, K. (1996) ‘Why ABC failed and how it may yet succeed’, Journal of Cost Management, Winter, pp.23–35. Roztocki, N. and Needy, L. (1999) ‘Integrating activity-based costing and economic value added in manufacturing’, Engineering Management Journal, Vol. 11, No. 2, pp.17–22. Roztocki, N. and Schultz, M. (2005) ‘Adoption and implementation of activity – based costing: a web-based survey’, Harvard Business Review, Vol. 41, No. 2, pp.29–35. Sartorius, K., Eitzen, C. and Kamala, P. (2007) ‘The design and implementation of activity based costing (ABC): a South African survey’, Meditari Accountancy Research, Vol. 15, No. 2, pp.1–21. Shields, M. (1995) ‘An empirical analysis of firms’ implementation experiences with activity-based costing’, Journal of Management Accounting Research, Fall, Vol. 7, pp.148–166.

The implementation of activity-based costing and the financial performance 153 Shim, E. and Stagliano, A. (1997) ‘A survey of U.S. manufacturers on implementation of ABC’, Journal of Cost Management, Vol. 11, No. 1, pp.39–41. Shim, E. and Sudit, E. (1995) ‘How Manufacturers Price Products’, Management Accounting, February, Vol. 76, No. 8, pp.37–39. Swenson, D. (1995) ‘The benefits of activity-based cost management to the manufacturing industry’, Journal of Management Accounting Research, Fall, Vol. 7, pp.167–180. Turney, P.B.B. and Anderson, B. (1989) ‘Accounting for continuous improvement’, Sloan Management Review, Vol. 30, No. 2, pp.37–47. Yakhou, M. and Dorweiler, V. (1995) ‘Advanced cost management systems: an empirical comparison of England, France and the United States’, Advances in International Accounting, Vol. 8, pp.99–127.