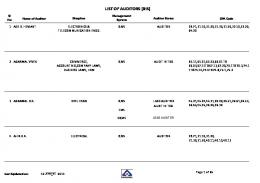

indicated that the subjects (auditors) used available unaudited book values and that the ..... sales, cost of sales, net inventories, net accounts receivable, accounts payable, and ..... XYZ, Inc., anew audit client, is a closely-held publicly-traded company, in which ... from about $10 million in 1976 to about S19 million in 1981.

Auditors' usage of unaudited book values when making presampling audit value estimates* MICHAEL D. SHIELDS San Diego State University IRA SOLOMON University of Illinois WILLIAM S. WALLER University of Arizona

Abstract. An important issue in audit judgment research concems auditors' use of unaudited book values when making judgments in the presampling phase of the audit. This paper presents a rudimentary model of the auditor's belief revision process with respect to unaudited book values from an audit value estimation perspective. An experiment testing some implications of the model is also presented. The model proposes that the auditor should judge the validity of unaudited book values in the circumstances and use them accordingly when making presampling audit value estimates. The experimental results indicated that the subjects (auditors) used available unaudited book values and that the extent of usage varied over accounts. However, the results also indicated some inaccurate presampling validity judgments which led to overweighting of unaudited book values. ResumS. Une question importante qui pr^occupe les chercheurs dans le domaine de la formulation de jugements en verification a trait it ['utilisation par les verificateurs de valeurs comptables non \6riMes dans la formulation de jugements au cours de la phase de la verification pr6c6dant l'echantillonnage. Les auteurs pr^sentent un modele rudimentaire du processus de revision des convictions du verificateur en ce qui a trait aux valeurs comptables non v6rifi6es dans une perspective d'estimation de la valeur de verification. Ils font egalement etat d'une experience destinee a verifier certaines des consequences du modele. Selon le modae, Ie verificateur devrait juger de la validite des valeurs comptables non vedfiees dans Ies circonstances et les utiliser en consequence dans la formation d'estimations de la valeur de verification avant echantillonnage. Les resultats de I'experience revfelent que les sujets (verificateurs) utilisent les valeurs comptables non vedfiees disponibles et que retendue de cette utilisation vade avec les comptes. Toutefois, les resultats revMent aussi l'inexactitude de certains jugements relatifs a la validite antedeure h rechantillonnage, h la suite desquels une importance trop grande a ete accordee aux valeurs comptables non vedfiees.

Introduction Performing an audit involves a sequential belief revision process. The auditor begins with a relatively diffuse prior belief about the appropriate audit values of the auditee's financial statement accounts, collects and processes new information * We appreciate the comments on earlier drafts of two anonymous reviewers, Paul Beck, Jim Donegan, Bill Felix, Jim Jiambalvo, Morley Lemon, Rachel Payes, John Wild, and the participants at the University of Illinois Accountancy Research Forum, Big Ten Doctoral Consortium, and the 1986 Amencan Accounting Association Midwest Meeting. Contemporary Accounting Research Vol. 5 No. 1 pp. 1-18

2 M.D. Shields

I. Solomon

W.S. Waller

about these values, and refines his prior belief accordingly. Audit values are the account values ultimately determined by the auditor to be in accordance with generally accepted accounting principles through the application of appropriate audit procedures. As interpreted here, the auditor's task is to form a sufficiently accurate posterior belief about audit values and, if necessary, impose adjustments such that the issued financial statements are consistent with this posterior belief (cf. Scott (1973)). The auditor's belief revision process is sequential because decomposed judgments and decisions made in early phases of the audit affect information collection and processing which in turn affect judgments and decisions in later phases (Felix and Kinney (1982)). For example, in the presampling or orientation/planning phase, judgments based on limited information are made about individual accounts and transaction cycles. These presampling judgments affect decisions about the nature and extent of evidence collection activities (i.e., sampling plans), and the collected evidence affects judgments about account valuation as well as decisions about audit adjustments. The sequential nature of the process highlights the importance of the auditor's presampling judgments and information processing underlying those judgments (Gibbins(1984); Waller and Felix (1984); Beck, Solomon andTomassini (1985)). One type of information about an account that is normally available for processing in the presampling phase is the unaudited book value, i.e., the value assigned by the auditee prior to the audit. Indeed, because unaudited book values are used in presampling audit procedures such as taking a trial balance and judging materiality, it may be difficult in most cases for the auditor to avoid processing this information. Recently, there has been some controversy regarding auditors' use of unaudited book values when forming expectations about the appropriate audit values (see Kinney and Uecker (1982); Biggs and Wild (1985)). However, given the above interpretation of the auditor's task, such use in principle is not at all controversial. On the contrary, because unaudited book values and audit values are highly correlated, often having the same value (Hylas and Ashton (1982)), use of the former when estimating the latter may be an efficient and effective means by which to accomplish this task. The purpose of this paper is to present a rudimentary model of the auditor's belief revision process with respect to unaudited book values and report an experiment that tested some implications of the model. The model proposes that, when making a presampling subjective probability estimate of an account's audit value, it is rational (in the sense of belief coherence) for the auditor to use the account's unaudited book value to the extent of its validity as judged at the time of estimation. Thus, an unaudited book value should not be used when its presampling validity is judged only to be minimal. Naturally, the consequences of such usage in a given case depend on the accuracy of the auditor's presampling validity judgment, such that both accuracy and coherence are important evaluation criteria. The experiment provides evidence on the following questions: Do subjects (auditors) use available unaudited book values when making presampling

Auditors' Usage of Unaudited Book Values

3

Figure 1 The auditor's sequential belief revision process P{a)

P{a\b, c) or P{a\c)?

1

P(a\b, c, cDoTP{a\c, d)1

1

f = 0

1 f= 2

1=1

Presampling Phase

Sampling Phase

subjective probability estimates of audit values? Does the extent of usage vary over accounts? Does estimation accuracy vary over accounts? The main results were that the subjects used unaudited book values and that the extent of usage vaded over accounts. Our interpretation is that the subjects made account-specific presampling validity judgments, for each account where the unaudited book value's presampling validity was judged not to be minimal, and accordingly used these values. However, estimation accuracy vaded over accounts in a manner which indicated that there were some erroneous presampling validity judgments and overweighting of unaudited book values. The remainder of the paper is organized as follows. The second section presents the model and states three related hypotheses. This section also contrasts the present study's approach with that of previous studies. The third and fourth sections report the expedment's method and results, respectively. The last section provides a discussion. Model and hypotheses The model assumes that the auditor's task is audit value estimation, i.e., to determine the appropdate audit values of the auditee's financial statement accounts. This task is accomplished through a sequential belief revision process (see Figure 1). At the beginning of the process (f = 0), the auditor has relatively diffuse beliefs about the audit values. These beliefs are based on previous contact with the auditee and other expert knowledge. At the level of an individual account, these beliefs may be represented by a subjective probability distdbution over possible audit values, Pia), where a denotes audit value and P(.) is a subjective probability estimate. The collection and processing of new infonnation dudng the audit may be seen as consisting of presampling and sampling phases. Dudng the presampling phase, the auditor collects and processes a vadety of information regarding the auditee's attdbutes (e.g., industry, operations, personnel, accounting system) and revises Pia) accordingly. As discussed further below, a key issue is whether the set of information processed dudng the presampling phase should include the unaudited book value (denoted by i ) ' . That is, should the auditor estimate Pia\b,c) or estimate Pia\c) ignodng b, where c denotes all other information besides b processed dudng the presampling phase? Using either 1 A further issue is whether the unaudited book value should be used at any point in the auditor's belief revision process. However, the focus of the present study is confined to its use dudng the presampling phase.

4

M.D. Shields

I. Solomon

W.S. Waller

P(a\b,c) or /'(ale), the auditor prepares a sampling plan at / = 1. During the sampling phase, this plan is implemented and sample evidence (denoted by d) is generated. The auditor processes d and revises P(alfc,c) or P(alc) into a posterior belief at t = 2, which may be represented by P{a\b,c,d) or P(alc,d), depending on whether b has been processed. The audit value then is a point estimate which summarizes the auditor's subjective probability estimate at r = 2. While this point estimate is the most important audit judgment about an account, the auditor's subjective probability estimate at / = 1 also is important because of its effects on his posterior belief at r = 2, both directly and through the sampling plan (see Beck, Solomon and Tomassini (1985)). Focusing on the presampling phase, suppose for the moment that the auditor processes c but not b. Since c consists of many individual pieces of information, Cx, C2 Cn, belief revision from P{a) to P{a\c) may be decomposed into numerous revisions, e.g., P{a) to P(alci) P(alci) to P{a\ciC2), and so on. It is assumed that each revision is consistent with Bayes' theorem^. Thus, for any c/, />(alc,) = PiCi\a)P{a)lP(Ci), given that P(c,) > 0. The likelihood, P(c,la), may be characterized as the presampling validity of c,- with respect to a. This validity is maximal when the variance of Pic,\a) is zero and minimal when P(c,la) is uniform. Increases in the presampling validity of c,- with respect to a, when judged accurately (see below), will on average lead to increases in the accuracy oi P{a\c^, other things being equal. So long as presampling validity is judged accurately and is not minimal, use of c,- when making a subjective probability estimate of a is rational, exclusive of cost considerations. Now, suppose that the auditor processes b as well as c during the presampling phase. The effects of using b are analogous to those of using c,. Assuming that belief revision from P(alc) to P{a\b,c) is consistent with Bayes' theorem,

P{a\b,c) = P(b\a,c)P{a,c)/P{b,c), given that Pib,c) > 0. P(b\a,c) is the presampling validity of b with respect to a given c. Increases in this validity (when judged accurately) will on average lead to increases in the accuracy of Pia\b,c), other things being equal. Use of b when estimating a is rational so long as b's validity is judged accurately and is not minimal. The likely consequences of this are a less extensive sampling plan prepared at r = 1 and more acciu^te posterior belief about a at r = 2. In short, the use of unaudited book values" may enhance both audit efficiency and effectiveness. It should be emphasized that the presampling validity of an unaudited book value employed in the auditor's belief revision process is conditional on his beliefs when this validity is judged, hence the modifier "presampling." It may happen that information processed during the sampling phase indicates a change in an unaudited book value's validity. Such a change would be incorporated into P{a\b,c,d). Also, the presampling validity of unaudited book values clearly does not need to be constant over audits or accounts within an audit. For example, the 2 Bayes' theorem is used as a belief revision model because of its general familiarity. Other belief revision models (see Diaconis and Zabell (1982)) could be used without changing the essence of our model.

Auditors' Usage of Unaudited Book Values 5 presampling validity of unaudited book values may be judged lower (higher) for an auditee with a weak (strong) control structure. Similarly, for a given auditee, the current unaudited book value of an account with (without) enors in previous years may have a lower (higher) judged presampling validity. As indicated above, effective use of unaudited book values depends on the accuracy with which their presampling validity is judged. Before discussing an approach to evaluating the accuracy of such validity judgments, it is necessary to consider the auditor's ultimate goal of formulating a sufficiently accurate posterior belief about audit values. In particular, what does "sufficiently accurate" mean? A complete answer would require a detailed consideration of many difficult issues (e.g., the auditor's utility function, processes for aggregating beliefs over accounts), which are not as yet resolved in the literature (see Scott, (1973, 1975, 1979); Felix and Grimlund (1977); Felix (1980)), and such resolution is beyond the scope of this paper. A tentative answer follows. The nonexistence of a true underlying audit value for an account precludes an evaluation of estimation accuracy by comparing the auditor's estimate with an objective criterion. However, one can imagine the distribution of audit values that would result from a large number of repeated applications of generally accepted audit procedures to the same situation. In principle, the accuracy of a given audit value estimate could be evaluated by comparing it to the central tendency of this distribution. However, since this distribution is merely hypothetical, indirect indicators of accuracy must be used. One such indicator is whether the audit values in the issued financial statements have been challenged by users. The absence of such challenges is prima facie evidence of sufficient accuracy. Evaluating the accuracy of presampling validity judgments is even more problematic, since the validity involves a relation between the unaudited book value and a sufficiently accurate audit value. Nevertheless, there should be a positive association between presampling validity judgment accuracy and the accuracy of P(olfo,c) relative to F(alc), so long as the validity is not minimal. Assuming that an unchallenged audit value is an adequate accuracy criterion, an evaluation of the relative accuracy of Pia\b,c) vs. P(alc) would provide indirect evidence of presampling validity judgment accuracy. When such validity is miminal, the accuracy of Pia\b,c) and Pia\c) should be the same. Conformance with the above model would produce the experimental results hypothesized below. The experiment involved two groups of subjects, all of whom were auditors. The experimental group assessed Pia\b,c), while the control group assessed P(alc) without knowledge of b^. It was expected that subjects in the experimental group would use the unaudited book values, assuming that they judged presampling validity not to be minimal. Such use would be indicated by a smaller difference between audit value estimates and conesponding unaudited book values for the experimental group than for the control group. 3 A between-subjects design was used to avoid demand characteristics that would have accompanied a within-subject design for this task.

6

M.D. Shields

I. Solomon

W.S. Waller

Figure 2 Accuracy and presence or absence of material error Accuracy Experimental group

Control group

Material error present

Material error absent

H I : Auditors use available unaudited book values when making audit value estimates.

As noted earlier, presampling validity is likely to vary over accounts within an audit. In the experiment, it was expected that such variability would produce changes over accounts in the weighting of unaudited book values when subjects in the experimental group made audit value estimates. Evidence of such changes would support the conclusion that the subjects did not treat the presampling validity of unaudited book values as constant, but instead conditioned such validity judgments on the unique circumstances of each judgment setting. H2: Auditors' usage of available unaudited book values when making audit value estimates vades over accounts. The last hypothesis concems presampling validity judgment accuracy. Accuracy was evaluated by comparing realized audit values with the subjects' audit value estimates. For simplicity, suppose that realized audit values may be dichotomized such that the unaudited book value contained or did not contain a material error. The presence of a material enor is prima facie evidence of minimal presampling validity. When this validity is minimal, the accuracy of the audit value estimates of the experimental and control groups should be the same. In other cases, the experimental group's estimates should be more accurate. H3: When unaudited book values contain matedal errors, the accuracy of audit value estimates made by auditors with and without these values is the same, but when unaudited book values do not contain matedal errors, the accuracy of audit value estimates is greater for auditors with these values.

This hypothesis is illustrated in Figure 2. For comparison purposes, it is worthwhile to consider some possible violations of the above model. One type of violation would be nonusage of unaudited book values when their presampling validity is not minimal, which would be indicated

Auditors' Usage of Unaudited Book Values Figure 3

7

Consequences of violation of normative model

Accuracy Experimental group

Control group

Material eiror present

Material error absent

by no differences between the experimental and control groups. Another type of violation would be consistent weighting of unaudited book values regardless of their presampling validity. Figure 3 illustrates the consequences of such a violation. Before describing the experiment that tested these hypotheses, it is important to contrast this study's approach with that of previous studies (Kinney and Uecker, (1982); Biggs and Wild (1985)), In the previous studies, the task was to specify a noninvestigation interval for an account as a part of an attention-directing analytical review. Special attention would be directed to the account only if the unaudited book value were to fall outside the interval. This decision rule effectively involves testing the hypothesis that the unaudited book value does not contain a material error, which is rejected only if the interval does not contain the unaudited book value (see Beck and Solomon (1985)). Use of the unaudited book value when specifying a noninvestigation interval is inappropriate. Although its use may decrease the risk of concluding that the unaudited book value contains a material error when in fact it does not, it also may increase the risk of concluding that the unaudited book value does not contain a material error when in fact it does. This concern arises when a noninvestigation interval is based on an audit value estimate. If an audit value estimate is affected by a materially misstated unaudited book value, then the noninvestigation interval would be biased in the direction of the unaudited book value. The result would be an increased risk of erroneously concluding that the unaudited book value does not contain a material error, which is undesirable assuming that compromising audit effectiveness is more costly than compromising audit efficiency. In addition, such usage involves a logical inconsistency in that the unaudited book value is an element of both the hypothesis and evidence set used to test the hypothesis. Despite these normative considerations, the previous studies reported that auditors used unaudited book values when specifying noninvestigation intervals.

8

M.D. Shields

I. Solomon

W.S. Waller

In contrast, the task in the present study's experiment was to make subjective probability estimates of audit values. The task included no explicit or implicit test of a hypothesis regarding the unaudited book value and, specifically, no postjudgment comparison between the unaudited book value and audit value estimate or related judgment variable (e.g., noninvestigation interval). Thus, the previous studies' proscriptions against the use of unaudited book values were not applicable. Instead, the audit value estimatation model presented earlier provides a relevant basis for evaluating the subjects' usage of unaudited book values. Method Overview Sixty-two auditors were randomly assigned to the experimental and control groups. They were given questionnaires containing an audit case, which asked them to make subjective probability estimates of the audit values of a set of accounts. The case information for the experimental group included current unaudited book values, while that for the control group excluded them. Thus, the estimates of the control group provided a baseline representing nonusage of unaudited book values. Besides unaudited book values, a substantial amount of case information was provided to both groups (see Appendix). Also, the realized audit values from the actual audit on which the case was based were available to us, but not to the subjects. Finally, since prior research has found that subjects' subjective probability estimates often are sensitive to the response mode (e.g., Winkler (1967) Felix (1976)), two modes were used as a between-subjects control variable. Subjects The subjects were auditors employed by three Big-Eight CPA firms in large metropolitan areas. Representatives of these firms were contacted who agreed to provide subjects. Questionnaires were sent to designated partners of these firms who distributed them to participating firm members. The subjects ranged from staff auditors to partners and had, on average, 4.3 years of auditing experience, 1.8 semester hours of college statistics, and 21.0 hours of in-house training related to statistics.'* Procedure and task The questionnaire had two parts. Thefirstpart provided an overview and a detailed practice exercise. Each subject was informed that the study was concemed with auditors' subjective probability estimates of audit values made in the presampling phase of the audit. The second part presented information regarding an auditee and 4 Subj'ects were not recruited from the CPA firm that provided the information on which the experiment's case was based. Further, the cooperating office of thisfirmand auditee were located in a different metropolitan area than those where the subjects were employed. Thus, it is unlikely that any of the subjects were able to identify the auditee or had independent access to the realized audit values.

Auditors' Usage of Unaudited Book Values

9

elicited subjective probability estimates of the audit values of six accounts - total sales, cost of sales, net inventories, net accounts receivable, accounts payable, and depreciation expense. All estimates were in the form of a cumulative distribution function (CDF) over possible audit values. Complete CDFs were elicited to facilitate the evaluation of estimation accuracy. The information set for both groups described the auditee's ownership, operations, products, growth pattem, economic environment, competition, financing, relations with a predecessor auditor, intemal control system quality, and financial data including audit values for two preceding years. The procedure for eliciting subjective probability estimates depended on the response mode. The two modes are designated below as the value-probability (VP) mode and probability-value (PV) mode. Using the VP mode for a given account, each subject was presented with mutually exclusive and collectively exhaustive intervals of possible audit values and was asked to specify a probability for each interval. For example, each subject was asked for the sales account, "What is the probability that the audit value is less than $11,500,000?", "What is the probability that the audit value is between $11,500,000 and $13,500,000?", and so on through "What is the probability that the audit value is greater than $23,500,000?"' Using the responses to these questions, each subject was instructed to perform a series of straightforward addition operations to compute cumulative probabilities for various possible audit values. Then, each subject plotted these cumulative probablities on a graph with possible audit values on the horizontal axis and cumulative probability on the vertical axis. Finally, each subject drew a complete CDF through these points on the graph. The last step was included, instead of ex post curve fitting, because it avoided arbitrary assumptions on our part about the nature of the CDF between the plotted points. Using the PV mode for a given account, each subject was presented with cumulative probabilities and asked to specify conesponding audit values. For example, each subject was asked for the sales account, "What is the dollar amount such that the probability is 0.05 that the audit value is less than that dollar amount?" This question was repeated using the cumulative probabilities 0.10, 0.25, 0.50, 0.75, 0.90, and 0.95. Each subject plotted the reponses to these questions on a graph similar to that used under the VP mode and drew a complete CDF through these points on the graph. Measures For hypotheses-testing purposes, use of the unaudited book value when making a subjective probability estimate of the audit value of an account was measured by u 5 When designing the questionnaire, the specific intervals for an account were established subject to three constraints. First, the intervals were equal, except for the "tails" (e.g., below $ 11,500,000 and above $23,500,(XX) for the sales account). Second, the number of intervals did not require an inordinate number of estimates (eight, including those for the "tails"). Third, the "nontail" intervals taken together covered a broad range such that it was unlikely that subjects would assign high probabilities to the "tails." This was done to enhance the precision of accuracy measures. The size of an interval ranged from ten percent (sales and cost of sales) to 23 percent (accounts payable) of an account's unaudited book value.

10 M.D. Shields

I. Solomon

W.S. Waller

TABLE 1 Realized audit values and unaudited book values

Sales Cost of sales Net inventories Net accounts receivable Accounts payable Depreciation expense

Realized audit values

Unaudited book values

Understatement (overstatement)

$19,012,000 14,346,000 3,983,000 3,660,000 1,070,000 346,000

$19,012,000 14,338,000 4,040,000 3,660,000 1,080,000 502,000

$

0 8,000 (57,000)

0 (10,000) (156,000)

= \m — b\/b, where m is the median of a subject's CDF for the account and b is the account's unaudited book value. The absolute difference between m and b was scaled by b to permit comparisons over accounts. Maximal use is indicated by « = 0, while nonuse is indicated by the mean value of u for the control group (see below). Two measures were used to evaluate estimation accuracy.* First, an "extremeness" measure, e, indicated how much probability was assigned to a nanow range of values centered on the realized audit value. For each account, this range equaled five percent of its realized audit value. Second, a "quadratic" measure, q, was computed by: (1) partitioning the scale of possible audit values of an account into many intervals, all of which were equal to five percent of its realized audit value and one of which was centered on that value, (2) determining the probability assigned to each interval, and (3) solving q= I — the sum of (r, — d,)^, where r,is the probability assigned to interval i andrf,-equals one for the interval centered on the realized audit value and zero for all other intervals. A key difference between e and qi is that the former focuses on only a part of the CDF while the latter takes the entire CDF into account. The range was [0,1] for e and [-1,1] for q. Both measures increase with accuracy. Results Preliminary analyses Table 1 presents the realized audit values and unaudited book values of the six accounts,' The unaudited book values of two accounts (sales and net accounts receivable) contained no enor, three accounts (cost of sales, net inventories, and accounts payable) contained small errors (less than two percent of the realized audit value), and one account (depreciation expense) contained a large enor (45 percent). Table 2 presents descriptive statistics, by group and overall, for m. For 6 Discussions of criteria for evaluating the accuracy of subjective probability estimates are provided by Winkler and Murphy (1968), Lichtenstein, Fischhoff and Phillips (1977,1982), and Beck, Solomon and Tomassini (1985). The measures used in this study were adapted from Winkler and Murphy (1968). 7 Since the audit was performed in 1982, there have beennochallenges(e.g., lawsuits byusers)ofthe CPA firms' conclusions. This provides indirect evidence that the realized audit values were sufficiently accurate.

Auditors' Usage of Unaudited Book Values

11

TABLE 2 Means (standard deviations) of m PVmode Experimental Control group (n = 31) group (n = 31) in = 33) $17,611,194 (1,544,419) 13,911,935 Cost of sales (1,163,737) Net inventories 3,964,968 (519,311) 3,399,355 Net accounts receivable (399,961) Accounts payable 1,207,429 (193,630) Depreciation expense 448,323 (54,215) Sales

$15,808,229 (3,459,819) 13,434,355 (1,831,528) 4,366,871 (758,339) 3,240,710 (720,865) 1,531,183 (246,080) 395,549 (39,921)

VP mode (n = 29)

$15,902,730 $17,627,999 (1,399,722) (3,447,416) 13,514,545 13,853,621 (1,023,897) (1,884,723) 4,146,091 4,188,483 (439,356) (836,918) 3,190,364 3,467,586 (661,621) (446,596) 1,356,721 1,383,626 (333,259) (189,072) 416.035 427,122 (60,815) (45,869)

Overall (n = 62) $16,709,711 (2,808,222) 13,673,145 (1,540,697) 4,165,919 (675,648) 3,320,033 (583,637) 1,369,306 (273,595) 421,936 (54,194)

m is the median of a subject's CDF for an account.

each account, the mean value of m for the experimental group was closer to the unaudited book value than was the mean value for the control group. For each account except depreciation expense, the variability in m was smaller for the experimental group than for the control group. In addition, the response mode appeared to affect the subjects' estimates. In particular, there was much less variability in m under the VP mode. Table 3 presents descriptive statistics, by group and overall, for u, e, and q. For each account, the mean value of u was closer to zero for the experimental group than for the control group. For each account except depreciation expense, mean accuracy (measured by either e or ^) was higher for the experimental group. Again, response mode effects appear to be present. Hypotheses testing HI predicted that auditors use available unaudited book values when making audit value estimates. H2 predicted that auditors' use of unaudited book values when making audit value estimates varies over accounts. To test both hypotheses, a 2x2x6 repeated-measures analysis of variance was performed in which « was the dependent variable, the set of six accounts was the within-subject factor, and both the presence or absence of unaudited book values and response mode were two-level between-subjects factors. The difference in u between the experimental and control groups was employed to measure the extent to which subjects in the former group used unaudited book values. To support HI, the mean value of u must be significantly lower for the experimental group. Regarding H2, if subjects in the experimental group always used the unaudited book values to the same extent, then the difference in u between the experimental and control groups would be equal for all accounts. Conversely, if the use of unaudited book values by subjects in the experimental group varied over accounts, then the difference in « would vary over accounts. In other words, to support H2, there must be a

12 M.D. Shields

1. Solomon

W.S. Waller

TABLE 3 Means (standard deviations) of u, e, and q Experimental group {n = 31) u: Sales Cost of sales Net inventories Net accounts receivable Accounts payable Depreciation expense Over accounts e: Sales Cost of sales Net inventories Net accounts receivable Accounts payable Depreciation expense Over accounts

Control group (n = 31)

PV mode (n = 33)

VP mode (n = 29)

Overall (n = 62)

0.078(0.077) 0.064(0.058) 0.094(0.088)

0.172(0.179) 0.106(0.093) 0.151(0.136)

0.166(0.179) 0 078(0.068) 0.107(0.094) 0.060(0.051) 0.148(0.145) 0.093(0.065)

0.125(0.145) 0.085(0.080) 0.122(0.117)

0.103(0.079) 0.160(0.141)

0.180(0.137) 0.418(0.228)

0.179(0.129) 0.099(0.087) 0.296(0.269) 0.281(0.175)

0.142(0.117) 0.289(0.228)

0.127(0.082) 0.104(0.050)

0.212(0.080) 0.207(0.100)

0.168(0.092) 0.171(0.091) 0.177(0.113) 0.130(0.058)

0.170(0.091) 0.155(0.094)

0.181(0.134) 0.171(0.097) 0.105(0.067)

0.076(0.088) 0.105(0.087) 0.079(0.066)

0.092(0.120) 0.170(0.118) 0.128(0.100) 0.149(0.094) 0.079(0.063) 0.106(0 069)

0 128(0.124) 0.138(0.097) 0.092(0.067)

0.107(0.066) 0.075(0.054)

0.062(0.043) 0.023(0.024)

0.083(0.066) 0.085(0.054) 0.049(0.053) 0.049(0.044)

0.084(0.060) 0.049(0.049)

0.031(0.024) 0.112(0.057)

0.066(0.060) 0.069(0.027)

0.043(0.055) 0.055(0.040) 0.079(0 031) 0.102(0.049)

0.049(0.048) 0.090(0.038)

VSales 0.162(0.275) -0.073(0.250) -0.050(0.313) 0.152(0.211) 0.045(0.286) Cost of sales 0.177(0.194) 0.046(0.218) 0.093(0.235) 0.132(0.192) 0.111(0.215) Net inventories 0.088(0.129) 0.057(0.125) 0.055(0.120) 0.093(0.134) 0.073(0.127) Net accounts receivable 0.086(0.137) 0.003(0.147) 0.037(0.168) 0.053(0.120) 0.044(0.147) Accounts payable 0.056(0.107) -0.044(0.097) -0.016(0.131) 0.031(0.084) 0.006(0.113) Depreciation expense -0.031(0.071) 0.015(0.137) -0.041(0.118) 0.029(0.017) -0.003(0.111) Over accounts 0.090(0.076) 0.001(0.051) 0.013(0.057) 0.082(0.052) 0.046(0.042) M is |m — b\tb, where m is the median of a subject's CDF for an account and b is the unaudited book value. e is the extremeness accuracy measure. q is the quadratic accuracy measure.

significant interaction between the account vadable and the presence or absence of unaudited book values. All three factors had significant main effects (Table 4). The significant effect for the presence or absence of unaudited book values, in conjunction with the lower mean value of u for the expedmental group than for the control group (Table 3), indicated that the subjects in the expedmental group used the unaudited book values. In addition, separate F-tests for each account consistently showed significant differences in u between the expedmental and control groups (Table 5). These results supported HI. Further, there was a significant account by presence or absence of unaudited book values interaction effect (Table 4). The between-group difference in u ranged from 0.042 for cost of sales to 0.258 for accounts payable. These results supported H2.

Auditors' Usage of Unaudited Book Values

13

TABLE 4 Analysis of variance for u Source

Sum of squares

Mean square

df

F

P

6.03 29.44 1.16

0.017 0.001 0.285

29.70 1.89 6.93 0.68

0.001 0.111 0.001 0 642

Between-subjects:

M B MxB Error Within-subjects: A AxM AxB AxBxM Error

0.205 l.OOO 0.040 1.971

1 I 1

58

0.205 1.000 0.040 0.034

2.673 0.170 0.625 0 060 5 345

5 5 5 5 290

0.535 0.034 0.125 0.012 0.018

« is |m — b\tb, where m is the median of a subject's CDF for an account and b is the unaudited book value. A is the set of six accounts. B is the presence or absence of unaudited book values. M IS the response mode variable. TABLE 5 F-tests for group differences in «

Account

Sum of squares

Sales Cost of sales Net inventories Net accounts receivable Accounts payable Depreciation expense

0.15 0.03 0.05 0.10 1.03 O.U

df

Mean square

Error sum of squares

1 1 1 1 1 1

0.15 0.03 0.05 0.10 1.03 0.11

0.98 0.31 0.73 0 63 2.14 0.39

df

Error mean square

F

P

58 58 58 58 58 58

0.017 0.005 0.012 0.011 0.037 0.007

8.67 5.66 4.21 9.07 28.00 16.63

0.004 0.020 0.040 0.004 0.001 0 001

« is (m - b\lb, where m is the median of a subject's CDF for an account and b is the unaudited book value.

H3 predicted that, when unaudited book values contain material errors, the accuracy of audit value estimates made by auditors with and without these values is the same, but when unaudited book values do not contain material errors, the accuracy of audit value estimates is greater for auditors with these values. Recall that there was no error or a very small error in the unaudited book values of all accounts except depreciation expense. To support H3, there must be an interaction between the account variable and the presence or absence of unaudited book values, whereby accuracy is the same for the experimental and control groups in the case of depreciation expense but higher for the experimental group in the case of all other accounts. A 2x2x6 repeated-measures analysis of variance was performed in which e was the dependent variable, the set of six accounts was the within-subject factor, and both the presence or absence of unaudited book values and response mode were two-level between-subjects factors. The key result was a

14 M.D. Shields

I. Solomon

W.S. Waller

TABLE 6 Analysis of variance for e Souree

Sum of squares

Between-subjects: M B MxB Error

0.056 0.179 0.000 0.367

1 1 1 58

Within-subjects: A AxM AxB AxBxM Error

0.463 0.069 0.171 0.028 1.434

5 5 5 5 290

Mean square

F

P

0.056 0.179 0.000 0.006

8.91 28.28 0.00

0.004 0.001 0.944

0.463 0.014 0.034 0.006 0.005

18.73 2.78 6.93 1.14

0.001 0.018 0.001 0.337

e is the extremeness accuracy measure. A is the set of six accounts. B is the presence or absence of unaudited book values. M is the response mode variable.

significant account by presence or absence of unaudited book values interaction (Table 6). To investigate this interaction further, an F-test was performed for each account to evaluate the relative accuracy of the experimental and control groups (Table 7). While the mean value of e was significantly higher for the experimental group in the case of sales, cost of sales, net accounts receivable, and accounts payable, it was significantly lower in the case of depreciation expense. These results did not support H3. Indeed, the results conformed closely to the violation pattem illustrated in Figure 3. The above analyses were repeated using q instead of e, and essentially the same results occuned.^ Discussion This paper has presented a model of the auditor's sequential belief revision process with respect to unaudited book values and has reported an experiment that tested some implications of tbe model. The model assumed that the auditor's task is audit value estimation. In performing this task, unaudited book values, like other information available to the auditor in the presampling phase, should be used to the extent of their judged validity in the circumstances. In the experiment, the subjects acted as if they judged the presampling validity of unaudited book values not to be minimal and accordingly used them when making audit value estimates. Further, the extent of usage varied over accounts, indicating that account-specific presampling validity judgments were made. These results were consistent with the model. However, the accuracy of the subjects' presampling validity judgments 8 Numerous sensitivity analyses were performed, including the use of wider intervals (ten percent rather than five pereent of the realized audit value) when constmcting the e and q measures, and adjusting the realized audit values upward and downward by five percent. In each analysis, essentially the same results occurred as those reported above.

Auditors' Usage of Unaudited Book Values

15

TABLE 7 F-tests for group differences in e

Account

Sum of squares

Sales Cost of sales Net inventories Net accounts receivable Accounts payable Depreciation expense

0.18 0.07 0.01 0.03 0.04 0.02

df

Mean square

Error sum of squares

df

Error mean square

1 1 1 1 1 1

0.18 0.07 0.01 0.03 0.04 0.02

0.67 0.49 0.25 0.17 0.10 0.12

58 58 58 58 58 58

0.011 0.008 0.004 0.003 0.002 0.002

F

P

15.7

0.001 0.006 0.104 0.002 0.001 0.004

8.1 2.7 10.6 23.2

8.9

€ is the extremeness accuracy measure.

varied over accounts in a manner that indicated violations of the model. Although subjects with unaudited book values were more accurate when the unaudited book values contained little or no error, they were less accurate when the unaudited book value contained a large error. In the latter case, no effect due to having unaudited book values would have been consistent with the model. The subjects appeared to make some inaccurate presampling validity judgments which led to overweighting unaudited book values. Four caveats and related issues for future researeh should be noted. First, although the model's state of development was sufficient for present purposes, it must be seen as mdimentary. Future analytical research on auditors' use of unaudited book values from an audit value estimation perspective would be welcome. Second, conclusions about the subjects' presampling validity judgments were infened from their subjective probability estimates of audit values. Future research should measure directly auditors' judgments of the presampling validity of unaudited book values and develop information processing models regarding the factors that affect such judgments (e.g., control structure, financial condition, industry, initial vs. continuing engagement, errors in previous years). Also, field research on the association between unaudited book values and audit values under various conditions would be valuable. Third, only one experimental case was used, so it is reasonable to question whether some of the results depended on idiosyncratic features of this case. For example, the auditee in the case had a relatively weak control structure and deteriorating financial condition. Thus, another question for future research is whether the extent or variability, or both, of auditors' usage of unaudited book values are different when an auditee has a stronger control structure or better financial condition. Also, it may have been unusual that depreciation expense tumed out to be the only account containing a large error. Fourth, expressing audit value estimates in the form of subjective probability distributions is not a "normal" task for most auditors. Our subjects clearly were not normative experts in subjective probability estimation, as indicated by the effects of formally equivalent response modes. However, the overall results of the experiment suggested that the subjects' lack of normative expertise did not prevent them from accomplishing the more basic task of audit value estimation.

16 M.D. Shields

I. Solomon

W.S. Waller

Appendix Case information for experimental group XYZ, Inc., anew audit client, is a closely-held publicly-traded company, in which members of the same family own about 44 percent of the voting shares. Since its incorporation about 30 years ago, XYZ has engaged in the design, development, manufacture, and sale of computer-related products. Its annual sales have risen from about $10 million in 1976 to about S19 million in 1981. Foreign subsidiaries accounted for about 15 percent ofthe total sales in 1981, while one customer alone accounted for about 21 percent of domestic sales for the same fiscal year. All manufacturing activities, however, take place at the company's facilities in the U.S. Both the adverse effects of continued inflation and reduced margins on some of the company's products, which were caused by intensified domestic and international competition, have accounted for the downward trend in profits for the last few years. Also, the rate of growth of the firm's sales is lower than those of its competitors. Furthermore, because of increases in short-term borrowings, interest expenses have increased substantially for the past two years, increasing by about 27 percent from fiscal 1979 to fiscal 1980, and by about 30 percent from fiscal 1980 to fiscal 1981. Most of XYZ's competitors are larger and have greater financial resources. XYZ believes that its ability to continue to compete successfully in its present markets is dependent on a combination of product quality, service, and price. Management also believes that the company has sufficient financial resources and personnel to maintain its competitive position in its present business. XYZ's internal control is on the lower end of the continuum of internal control systems upon which the external auditor can place reliance. In 1981, there was a large turnover of accounting personnel, including both the controller and the accounting supervisor. Their respective successors are less familiar with the electronics industry, and the new accounting supervisor is yet to comprehend fully XYZ's accounting practices. Discussions with the predecessor (Big Eight) auditor indicate that, historically, XYZ booked several adjustments as a result of the external audit. Most of these adjustments could be attributed to unintentional errors (mostly relating to purchases ahd costing of inventories), or nonconformity with company accounting principles on a consistent basis (especially relating to capitalizing versus expensing certain expenditures). The firm also rarely seeks the advice or services of the auditors on issues of accounting significance. For example, XYZ usually files quarterly reports without prior review. Hence, such reviews typically are performed retrospectively. The EDP systems are out of date, and new ones are urgently required. In addition, XYZ's cost accounting system is unreliable. Although there appears to be a reasonable segregation of duties between related employees, four members of the same family hold key corporate positions enhancing the likelihood of

Auditors' Usage of Unaudited Book Values

17

management overdde of the intemal control system. The firm has no intemal audit function, but does have an active three-member audit committee (two of which are nonemployee directors).

Financial Data Account item Total sales Cost of sales Income before taxes Income tax provision Net income Inventory: Finished goods Work-in-process Raw materials Inventory valuation reserve (a) Net inventory Inventory expensed as obsolete Accounts receivable: Consolidated balance (b) Allowance for doubtful accounts Net accounts receivable Bad debt expense Accounts payable Plant, property & equipment: Land Depreciable assets Accumulated depreciation Net plant, property & equipment Depreciation expense

Audited 1979

Audited 1980

Unaudited 1981

$16,204,000 10,967,000 1,429,000 597,000 832,000

$15,641,000 11,851,000 255,000 47,000 208.000

$19,012,000 14,338,000 289,000 110,000 179,000

283,000 555,000 2,624,000 3,462,000 0 3,462,000 14,000

204,000 874,000 3,158,000 4,236,000 (185,000) 4,051,000 189,000

481,000 912,000 2,647,000 4,040,000 0 4,040,000 360.000

3,344,000 (77,000) 3,267,000 26,000 1,354,000

3,045,000 (77,000) 2,968,000 1,000 1,407,000

3,775.000 (115.000) 3,660,000 61,000 1,080,000

302,000 5,040,000 (1.490,000) 3,852,000 311,000

302,000 5,156,000 (1,845,000) 3,613,000 371,000

302,000 5.286.000 (2,186,000) 3.402,000 502.000

Supplemental notes to financial data (a) "Inventory Valuation Reserve" represents reserve for slow-moving inventodes of finished goods and raw matedals which would have to be sold below cturent pdces because of obsolescence. (b) The Accounts Receivable Aging Analysis is as follows: Current 31-60 days 61-90 days Over90days

$2,508,000 602.000 134.000 100.000

75.0% 18.0 4.0 3.0

$1,857,000 731.000 244,000 213.000

61.0% 24.0 8.0 7.0

$2,227,000 679.000 189,000 680.000*

59.0% 18.0 5.0 18.0

$3,344,000

100.0%

$3,045,000

100.0%

$3,775,000

100.0%

* Includes $363,000 of long-term extended Accounts Receivable. Otherwise, the aging pereentage for this category would have been eight pereent.

18 M.D. Shields

I.Solomon

W.S. Waller

References Beck, P. and I. Solomon, "Sampling Risks and Audit Consequences under Altemative Testing Approaches," The Accounting Review (October 1985) pp. 714-723. Beck, P., I. Solomon and L. Tomassini, "Subjective Prior Probability Distributions and Audit Risk," Journal of Accounting Research (Spring 1985) pp. 37-56. Biggs, S. and J. Wild, "Aninvestigationof Auditor Judgment in Analytical Review," The Acconting Review (October 1985) pp. 607-633. Diaconis, P. and S. Zabell, "Updating Subjective Probability," Journal of the American Statistical Association (December, 1982) pp. 822-830. Felix, W., "Evidence on Altemative Means of Assessing Prior Probability Distributions for Audit Decision Making," The Accounting Review (October 1976) pp. 800-807. Felix, W., "The Beginnings of the Audit Logic Process: A Decomposition of Beliefs," paper presented at the Fourth Duke University Symposium (April, 1980). Felix, W. andR. Grimlund, "A Sampling Model for Audit Tests of Composite Accounts," Journal of Accounting Research (Spring 1977) pp. 23-41. Felix, W. and W. Kinney, "Research in the Auditor's Opinion Formulation Process," The Accounting Review (April 1982) pp. 245-271. Gibbins, M., "Propositions about the Psychology of Professional Judgment in Public Accounting," Journal of Accounting Research (Spring 1984) pp. 103-125. Hylas, R. andR. Ashton, "Audit Detection of Financial Statement Errors," The Accounting Review (October 1982) pp. 751-765. Kinney, W. and W. Uecker, "Mitigating the Consequences of Anchoring in Auditor Judgments," The Accounting Review (January 1982) pp. 55-69. Lichtenstein, S., B. Fischhoff and L. Phillips, "Calibrations of Probabilities: The State of the Art," in H. Jungermann and G. deZeeuw (eds.). Decision Making and Change in Human Affairs (D. Reidel: Dordrecht, 1977) pp. 275-324. Lichtenstein, S., B. Fischhoff and L. Phillips, "Calibrations of Probabilities: The State of the Art to 1980," in D. Kahneman, P. Slovic, and A. Tversky (eds.). Judgment under Uncertainty:Heuristics andBiases (Cambridge University Press: Cambridge, 1982) pp. 306-334. Scott, W., "A Bayesian Approach to Asset Valuation and Audit Size," Journal of Accounting Research (Autumn 1973) pp. 304-330. Scott, W., "Auditors' Loss Functions Implicit in Consumption-Investment Models," Journal of Accounting Research (Supplement 1975) pp. 98-117. Scott, W., "Scoring Rules for Probabilistic Reporting," Journal of Accounting Research (Spring 1979) pp. 156-178. Waller, W. and W. Felix, "Cognition and the Auditor's Opinion Formulation Process: A Schematic Model of Interactions between Memory and Current Audit Evidence," in S. Modarity and E. Joyce (eds.). Decision Making and Accounting: Current Research (University of Oklahoma Press: Norman, 1984) pp. 27-48. Winkler, R., "The Assessment of Prior Distributions in Bayesian Anaylsis," Journal of the American Statistical Association (September 1967) pp. 776-800. Winkler, R. and A. Murphy, "'Good' Probability Assessors," Journal of Applied Meteorology (October 1968) pp. 751-758.