Jan 11, 2016 - The demand for journey duration and reliability: Paris Region work ... by mode and sex, 2010-2011. ..... First car public free (8,9) at Orig 4OV1.

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11.

Introduction to this dataset

Any user of TRIO algorithms can produce tables of regression estimation results called «tablexes», each such table presenting statistics chosen in a menu. Each Tablex edition presents in columns the results requested for each regression run (called «variant») and splits the lines of the table in three sections: Part I. Presents for instance, for each explanatory variable, perhaps the following statistics: regression coefficient, elasticity (for any variable including a dummy variable, the code name of which will then be underlined twice), Student’s t (relative to 0) conditional on the Box-Cox transformation estimates and a flag to recall the identity of the Box-Cox transformation applied to the variable in question; Part

II.

Presents the estimated Box-Cox power, autocorrelation (and, heteroskedasticity) parameters and their Student’s t (relative to 0 and 1);

eventually

Part III. Presents general statistics: value of the Log-Likelihood, sample used, measures of fit, etc. We include here detailed editions in English of results obtained for the four selected optimal models: Base 2, Men, variants 17 (Public transit) and 22 (Private car, drive alone) ........................ 2 Base 3, Women, variants 31 (Public transit) and 35 (Private car, drive alone) ................. 11

The same tables of results can be found in French, along with many other model variant results drawn from the extensive French-language report: Gaudry, M. (2015). La demande de durée et de fiabilité des trajets de transport : tests d’une méthode à trois moments sur les durées domicile-travail constatées en Île-de-France. Publication AJD 153, Agora Jules Dupuit, Université de Montréal. 134 p. January. The four selected optimal models are from Column 3 of Appendices 4 & 5 (Men) and 7 & 8 (Women) of that document, also listed as a Dataset on ResearchGate.

Marc Gaudry, January 11, 2016.

1

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11.

Base 2, Men, variants 17 (Public transit) and 22 (Private car, drive alone) =================================================================== PART I. Presented statistics Model type L-1.6 L-1.6 Name of the variant DUREE DUREE Version number of the variant 17 22 Dependent variable in the variant DUREE DUREE =================================================================== -----------D = TRIP -----------THIRD TRIP ND3 (Dummy) === BETA coefficient -0.89D-01 -0.70D-01 Derivative of Y (sample value) -0.25D+01 -0.19D+01 Derivative of E(Y) -0.19D+01 -0.19D+01 Derivative of SIGMA(Y) -0.42D+00 -0.55D+00 Derivative of GAMMA(Y) 0.57D-02 0.48D-02 Elasticity of Y (sample value) -0.41D-01 -0.45D-01 Elasticity of E(Y) -0.44D-01 -0.45D-01 Elasticity of SIGMA(Y) -0.35D-01 -0.40D-01 Elasticity of GAMMA(Y) 0.84D-02 0.55D-02 Correlation (Y,X_k) original units -0.22D-01 -0.51D-01 Correlation (Y,X_k) Box-Cox transf. -0.46D-01 -0.57D-01 Conditional t-statistic for BETA ( -0.86) ( -0.39) MONDAY J1 (Dummy) == BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.21D-01 -0.59D+00 -0.44D+00 -0.99D-01 0.14D-02 -0.98D-02 -0.10D-01 -0.84D-02 0.20D-02 -0.73D-01 -0.76D-01 ( -0.38)

TUESDAY J2 (Dummy) == BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.16D-02 0.11D-02 -0.46D-01 0.29D-01 -0.35D-01 0.30D-01 -0.77D-02 0.85D-02 0.11D-03 -0.75D-04 -0.76D-03 0.70D-03 -0.81D-03 0.70D-03 -0.65D-03 0.62D-03 0.16D-03 -0.85D-04 -0.32D-01 -0.10D-02 -0.28D-01 0.39D-02 ( -0.03) ( 0.02)

WEDNESDAY J3 (Dummy) == BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.87D-01 0.24D+01 0.18D+01 0.41D+00 -0.56D-02 0.40D-01 0.43D-01 0.35D-01 -0.83D-02 0.21D-01 0.18D-01 ( 1.54)

-0.29D-01 -0.80D+00 -0.80D+00 -0.23D+00 0.20D-02 -0.19D-01 -0.19D-01 -0.17D-01 0.23D-02 -0.75D-01 -0.69D-01 ( -0.51)

0.28D-01 0.76D+00 0.77D+00 0.22D+00 -0.19D-02 0.18D-01 0.18D-01 0.16D-01 -0.22D-02 -0.82D-01 -0.96D-01 ( 0.52)

2

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11. THURSDAY J4 (Dummy) == BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.94D-01 0.26D+01 0.20D+01 0.44D+00 -0.60D-02 0.43D-01 0.46D-01 0.37D-01 -0.89D-02 0.66D-01 0.66D-01 ( 1.61)

0.59D-01 0.16D+01 0.16D+01 0.47D+00 -0.41D-02 0.39D-01 0.38D-01 0.34D-01 -0.47D-02 -0.82D-02 -0.98D-02 ( 1.06)

Entering Paris(GC_P+PC_P)AM Peak ENTRANTP (Dummy) ======== BETA coefficient 0.81D-01 -0.17D+00 Derivative of Y (sample value) 0.23D+01 -0.47D+01 Derivative of E(Y) 0.17D+01 -0.47D+01 Derivative of SIGMA(Y) 0.38D+00 -0.13D+01 Derivative of GAMMA(Y) -0.52D-02 0.12D-01 Elasticity of Y (sample value) 0.38D-01 -0.11D+00 Elasticity of E(Y) 0.40D-01 -0.11D+00 Elasticity of SIGMA(Y) 0.32D-01 -0.98D-01 Elasticity of GAMMA(Y) -0.77D-02 0.14D-01 Correlation (Y,X_k) original units 0.15D-01 0.15D+00 Correlation (Y,X_k) Box-Cox transf. 0.43D-01 0.14D+00 Conditional t-statistic for BETA ( 1.87) ( -2.45) Exiting Paris (P_GC+P_PC)AM Peak SORTANTP (Dummy) ======== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA ----------------------S = NETWORK SERVICE ----------------------Transit sum of itinerary utilities SUMTCTC (Quasi-dummy) ------BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.50D-01 0.14D+01 0.11D+01 0.23D+00 -0.32D-02 0.23D-01 0.25D-01 0.20D-01 -0.47D-02 -0.13D+00 -0.13D+00 ( 0.88)

-0.60D-03 -0.16D-01 -0.17D-01 -0.47D-02 0.42D-04 -0.39D-03 -0.39D-03 -0.34D-03 0.47D-04 0.56D-01 0.74D-01 ( -0.01)

-0.26D+00 -0.29D+05 -0.22D+05 -0.49D+04 0.67D+02 -0.76D-01 -0.81D-01 -0.65D-01 0.16D-01 -0.31D+00 -0.74D+00 (-31.97) EL1

3

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11. Car only trip time TPVPVP (Quasi-dummy) -----BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA Not transit pass holder NABONTC (Dummy) ======= BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.53D+00 0.81D+00 0.82D+00 0.23D+00 -0.21D-02 0.76D+00 0.75D+00 0.66D+00 -0.91D-01 0.78D+00 0.81D+00 ( 37.59) EL1

-0.17D+00 -0.48D+01 -0.36D+01 -0.80D+00 0.11D-01 -0.79D-01 -0.84D-01 -0.68D-01 0.16D-01 -0.99D-01 -0.11D+00 ( -2.64)

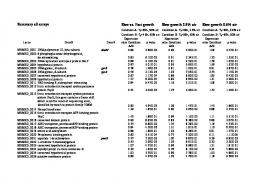

-----------------------PO = PARKING AT NIGHT -----------------------First car curb paying (1,2) at Orig 1OV1 (Dummy) ==== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.19D+00 0.52D+01 0.53D+01 0.15D+01 -0.13D-01 0.13D+00 0.12D+00 0.11D+00 -0.15D-01 -0.79D-02 0.13D-01 ( 1.64)

First car curb free (3) at Origin 2OV1 (Dummy) ==== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.79D-02 0.22D+00 0.22D+00 0.62D-01 -0.55D-03 0.52D-02 0.51D-02 0.45D-02 -0.63D-03 -0.23D-01 -0.23D-01 ( 0.18)

4

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11. First car public free (8,9) at Orig 4OV1 (Dummy) ==== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.11D-01 -0.29D+00 -0.29D+00 -0.83D-01 0.73D-03 -0.69D-02 -0.68D-02 -0.60D-02 0.83D-03 0.11D-01 0.70D-02 ( -0.05)

First car public paying (10,11) at 5OV1 (Dummy) ==== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.17D+00 0.46D+01 0.47D+01 0.13D+01 -0.12D-01 0.11D+00 0.11D+00 0.97D-01 -0.13D-01 -0.12D-02 0.84D-02 ( 0.52)

----------------------PD = PARKING AT WORK ----------------------Parking reserved at work Destinatio SResD (Dummy) ===== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.35D-01 -0.96D+00 -0.97D+00 -0.28D+00 0.24D-02 -0.23D-01 -0.23D-01 -0.20D-01 0.28D-02 0.40D-02 -0.44D-02 ( -0.75)

Curb paid (2,3) at Dest. 1DStat (Dummy) ====== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.23D-01 -0.63D+00 -0.64D+00 -0.18D+00 0.16D-02 -0.15D-01 -0.15D-01 -0.13D-01 0.18D-02 0.48D-01 0.45D-01 ( -0.26)

5

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11. Curb free (4,5) at Dest. 2DStat (Dummy) ====== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.11D+00 0.30D+01 0.30D+01 0.86D+00 -0.76D-02 0.71D-01 0.71D-01 0.62D-01 -0.86D-02 -0.36D-01 -0.49D-01 ( 1.71)

Public location free (12,13) at Des 4DStat (Dummy) ====== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.26D-01 0.70D+00 0.71D+00 0.20D+00 -0.18D-02 0.17D-01 0.17D-01 0.15D-01 -0.20D-02 -0.56D-01 -0.55D-01 ( 0.35)

Public location paying (14,15) at D 5DStat (Dummy) ====== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.36D+00 0.98D+01 0.99D+01 0.28D+01 -0.25D-01 0.24D+00 0.23D+00 0.21D+00 -0.28D-01 0.67D-01 0.51D-01 ( 1.17)

--------------------F = FAMILY STATUS --------------------Partner NP2 (Dummy) === BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.43D-01 0.30D-01 0.12D+01 0.82D+00 0.89D+00 0.83D+00 0.20D+00 0.24D+00 -0.27D-02 -0.21D-02 0.20D-01 0.20D-01 0.21D-01 0.20D-01 0.17D-01 0.17D-01 -0.40D-02 -0.24D-02 0.10D+00 0.99D-02 0.10D+00 0.13D-01 ( 0.72) ( 0.57)

6

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11. Child NP3 (Dummy) === BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.33D+00 0.91D+01 0.69D+01 0.15D+01 -0.21D-01 0.15D+00 0.16D+00 0.13D+00 -0.31D-01 0.65D-01 0.63D-01 ( 2.20)

-0.78D-03 -0.21D-01 -0.21D-01 -0.61D-02 0.54D-04 -0.51D-03 -0.50D-03 -0.44D-03 0.61D-04 0.47D-01 0.43D-01 ( -0.01)

Previous generation NP4 (Dummy) === BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.68D+00 0.19D+02 0.14D+02 0.32D+01 -0.44D-01 0.32D+00 0.34D+00 0.27D+00 -0.65D-01 0.68D-01 0.64D-01 ( 2.28)

-0.64D-01 -0.17D+01 -0.17D+01 -0.50D+00 0.44D-02 -0.42D-01 -0.41D-01 -0.36D-01 0.50D-02 -0.45D-01 -0.52D-01 ( -0.22)

AGE AGE BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.32D-02 0.91D-01 0.68D-01 0.15D-01 -0.21D-03 0.59D-01 0.63D-01 0.51D-01 -0.12D-01 0.53D-01 0.51D-01 ( 1.70)

-0.20D-04 -0.54D-03 -0.54D-03 -0.16D-03 0.14D-05 -0.54D-03 -0.54D-03 -0.48D-03 0.66D-04 0.40D-01 0.40D-01 ( -0.01)

2 Tradesperson, commerc., manager CSP2 (Dummy) ==== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.75D-01 0.54D-01 -0.21D+01 0.15D+01 -0.16D+01 0.15D+01 -0.35D+00 0.43D+00 0.48D-02 -0.38D-02 -0.35D-01 0.35D-01 -0.37D-01 0.35D-01 -0.30D-01 0.31D-01 0.72D-02 -0.43D-02 -0.44D-02 0.24D-01 0.40D-03 0.19D-01 ( -0.34) ( 0.43)

7

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11. 3 Management, higher professional CSP3 (Dummy) ==== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.10D-01 0.53D-01 -0.28D+00 0.14D+01 -0.21D+00 0.15D+01 -0.47D-01 0.42D+00 0.64D-03 -0.37D-02 -0.46D-02 0.35D-01 -0.49D-02 0.35D-01 -0.40D-02 0.30D-01 0.95D-03 -0.42D-02 -0.14D+00 0.98D-01 -0.14D+00 0.13D+00 ( -0.17) ( 0.83)

4 Intermediate professional CSP4 (Dummy) ==== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.24D-01 0.68D+00 0.51D+00 0.11D+00 -0.16D-02 0.11D-01 0.12D-01 0.97D-02 -0.23D-02 0.52D-01 0.57D-01 ( 0.39)

0.49D-01 0.13D+01 0.14D+01 0.39D+00 -0.34D-02 0.32D-01 0.32D-01 0.28D-01 -0.39D-02 -0.12D-01 -0.23D-01 ( 0.78)

6 Worker CSP6 (Dummy) ==== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.58D-02 0.16D+00 0.12D+00 0.27D-01 -0.37D-03 0.27D-02 0.29D-02 0.23D-02 -0.55D-03 0.10D+00 0.86D-01 ( 0.08)

0.26D-01 0.71D+00 0.72D+00 0.21D+00 -0.18D-02 0.17D-01 0.17D-01 0.15D-01 -0.21D-02 -0.98D-01 -0.11D+00 ( 0.37)

8 Other CSP8 (Dummy) ==== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.13D+00 0.37D+00 -0.36D+01 0.10D+02 -0.27D+01 0.10D+02 -0.60D+00 0.29D+01 0.83D-02 -0.25D-01 -0.59D-01 0.24D+00 -0.63D-01 0.24D+00 -0.51D-01 0.21D+00 0.12D-01 -0.29D-01 0.37D-02 0.64D-01 0.44D-02 0.49D-01 ( -0.17) ( 1.96)

8

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11. ----------------F = HOUSEHOLD ----------------Number of persons in household MNP BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.25D-01 0.16D-02 0.70D+00 0.44D-01 0.53D+00 0.44D-01 0.12D+00 0.13D-01 -0.16D-02 -0.11D-03 0.31D-01 0.30D-02 0.33D-01 0.30D-02 0.26D-01 0.27D-02 -0.63D-02 -0.37D-03 0.15D+00 0.18D-01 0.15D+00 0.21D-01 ( 1.71) ( 0.11)

Net income increasing level (1-10) ReNM1_10 (Quasi-dummy) -------BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.62D-02 0.47D-02 -0.17D+00 0.13D+00 -0.13D+00 0.13D+00 -0.29D-01 0.37D-01 0.40D-03 -0.32D-03 -0.20D-01 0.23D-01 -0.21D-01 0.22D-01 -0.17D-01 0.20D-01 0.41D-02 -0.27D-02 -0.33D-01 0.30D-01 -0.34D-01 0.46D-01 ( -0.61) ( 0.39)

Income unknown or other (11-12) ReNMetc (Dummy) ======= BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.11D+00 0.13D+00 -0.32D+01 0.34D+01 -0.24D+01 0.35D+01 -0.54D+00 0.99D+00 0.73D-02 -0.87D-02 -0.53D-01 0.82D-01 -0.56D-01 0.82D-01 -0.45D-01 0.72D-01 0.11D-01 -0.10D-01 -0.17D-01 0.85D-01 -0.13D-01 0.92D-01 ( -0.97) ( 1.01)

----------------ETC =ET CETERA ----------------REGRESSION CONSTANT BETA coefficient Conditional t-statistic for BETA

constant 0.34D+01 ( 25.83)

0.16D+01 ( 10.54)

=================================================================== PART II. Parameters t-statistic unconditional (=0) [=1] Model type L-1.6 L-1.6 Name of the variant DUREE DUREE Version number of the variant 17 22 Dependent variable in the variant DUREE DUREE =================================================================== Box-Cox transformations (estimated) ----------------------------------Lambda(y) ELY 0.188 0.114 ( 3.44) ( 2.81) [ -14.9] [ -21.7] Lambda(x) - group 1

EL1

0.051 ( 5.19) [ -95.9]

0.213 ( 2.81) [ -10.4]

9

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11. =================================================================== PART III. General statistics Model type L-1.6 L-1.6 Name of the variant DUREE DUREE Version number of the variant 17 22 Dependent variable in the variant DUREE DUREE =================================================================== Log-likelihood -4013.73 -3299.56 Degrees of freedom

23

31

Pearson R2 Pearson R2 adjusted for Degrees of freedom

0.560 0.549

0.617 0.602

Pseudo-(L)-R2 Pseudo-(L)-R2 adjusted for Degrees of freedom

0.566 0.556

0.658 0.645

Average probability (Y=limit observation)

0.000

0.000

- Number of observations

1830

1830

Estimation - Number of observations - First observation - Last observation

979 1 979

851 980 1830

21 1

29 1

0 0 1

0 0 1

0 1

0 1

0 0

0 0

0 0

0 0

0

0

0 24

0 32

Mean of observed Y Standard error of observed Y Skewness of observed Y

0.61D+02 0.24D+02 0.10D+01

0.42D+02 0.24D+02 0.15D+01

Mean of Y, estimated at the mean Standard error of Y, estimated at the mean Skewness of Y, estimated at the mean

0.43D+02 0.12D+02 0.68D+00

0.42D+02 0.14D+02 0.88D+00

Mean of estimated E(Y) Standard error of estimated E(Y) Skewness of estimated E(Y)

0.61D+02 0.18D+02 0.71D+00

0.42D+02 0.19D+02 0.98D+00

0.45D+01 0.22D+00 -0.33D+03 -0.31D-02 -0.73D+02 -0.14D-01

0.35D+01 0.29D+00 -0.40D+03 -0.25D-02 -0.11D+03 -0.88D-02

Sample

Total number of fixed or estimated parameters: - Beta .Estimated .Constant - Lambda(y) .Fixed .Estimated .Constrained .Distinct - Lambda(x) .Fixed .Estimated - Heteroskedasticity Delta .Fixed .Estimated Lambda(z) .Fixed .Estimated - Autocorrelation Rho .Estimated - Total .Fixed .Estimated

M.R.S. between Measures M1, M2 and M3 M1 / M2 M2 / M1 M1 / M3 M3 / M1 M2 / M3 M3 / M2

Elasticity of substitution between M1, M2 and M3 M1 / M2 0.12D+01 0.11D+01 M2 / M1 0.81D+00 0.88D+00 M1 / M3 -0.52D+01 -0.82D+01 M3 / M1 -0.19D+00 -0.12D+00 M2 / M3 -0.42D+01 -0.72D+01 M3 / M2 -0.24D+00 -0.14D+00 ===================================================================

10

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11.

Base 3, Women, variants 31 (Public transit) and 35 (Private car, drive alone) =================================================================== PART I. Presented statistics Model type L-1.6 L-1.6 Name of the variant DUREE DUREE Version number of the variant 31 35 Dependent variable in the variant DUREE DUREE =================================================================== -----------D = TRIP -----------THIRD TRIP ND3 (Dummy) === BETA coefficient -0.65D+00 -0.13D+00 Derivative of Y (sample value) -0.71D+01 -0.20D+01 Derivative of E(Y) -0.57D+01 -0.20D+01 Derivative of SIGMA(Y) -0.11D+01 -0.45D+00 Derivative of GAMMA(Y) 0.32D-01 0.92D-02 Elasticity of Y (sample value) -0.12D+00 -0.57D-01 Elasticity of E(Y) -0.14D+00 -0.57D-01 Elasticity of SIGMA(Y) -0.80D-01 -0.43D-01 Elasticity of GAMMA(Y) 0.57D-01 0.14D-01 Correlation (Y,X_k) original units -0.41D-01 -0.78D-01 Correlation (Y,X_k) Box-Cox transf. -0.42D-01 -0.73D-01 Conditional t-statistic for BETA ( -1.81) ( -1.25) MONDAY J1 (Dummy) == BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.12D-01 0.13D+00 0.10D+00 0.19D-01 -0.57D-03 0.21D-02 0.25D-02 0.14D-02 -0.10D-02 -0.76D-02 -0.13D-01 ( 0.09)

0.18D-01 0.27D+00 0.27D+00 0.61D-01 -0.12D-02 0.77D-02 0.76D-02 0.58D-02 -0.19D-02 -0.12D-01 -0.24D-01 ( 0.22)

TUESDAY J2 (Dummy) == BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.28D-01 0.31D+00 0.25D+00 0.46D-01 -0.14D-02 0.52D-02 0.60D-02 0.35D-02 -0.25D-02 -0.17D-01 -0.19D-01 ( 0.20)

0.93D-01 0.14D+01 0.14D+01 0.31D+00 -0.64D-02 0.40D-01 0.39D-01 0.30D-01 -0.95D-02 -0.40D-01 -0.42D-01 ( 1.30)

WEDNESDAY J3 (Dummy) == BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.12D+00 0.13D+01 0.11D+01 0.20D+00 -0.59D-02 0.22D-01 0.26D-01 0.15D-01 -0.11D-01 0.99D-02 0.17D-01 ( 0.80)

-0.34D-01 -0.51D+00 -0.52D+00 -0.11D+00 0.24D-02 -0.15D-01 -0.14D-01 -0.11D-01 0.35D-02 -0.40D-01 -0.43D-01 ( -0.44)

11

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11. THURSDAY J4 (Dummy) == BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.11D+00 0.10D+00 0.12D+01 0.15D+01 0.94D+00 0.15D+01 0.17D+00 0.34D+00 -0.52D-02 -0.70D-02 0.20D-01 0.43D-01 0.23D-01 0.43D-01 0.13D-01 0.33D-01 -0.94D-02 -0.10D-01 -0.57D-02 0.35D-01 -0.22D-02 0.32D-01 ( 0.74) ( 1.25)

Entering Paris(GC_P+PC_P)AM Peak ENTRANTP (Dummy) ======== BETA coefficient 0.12D-01 -0.20D+00 Derivative of Y (sample value) 0.13D+00 -0.31D+01 Derivative of E(Y) 0.11D+00 -0.31D+01 Derivative of SIGMA(Y) 0.20D-01 -0.69D+00 Derivative of GAMMA(Y) -0.59D-03 0.14D-01 Elasticity of Y (sample value) 0.22D-02 -0.88D-01 Elasticity of E(Y) 0.26D-02 -0.87D-01 Elasticity of SIGMA(Y) 0.15D-02 -0.66D-01 Elasticity of GAMMA(Y) -0.11D-02 0.21D-01 Correlation (Y,X_k) original units 0.24D-01 0.20D+00 Correlation (Y,X_k) Box-Cox transf. 0.34D-01 0.17D+00 Conditional t-statistic for BETA ( 0.13) ( -1.73) Exiting Paris (P_GC+P_PC)AM Peak SORTANTP (Dummy) ======== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA ----------------------S = NETWORK SERVICE ----------------------Transit sum of itinerary utilities SUMTCTC (Quasi-dummy) ------BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.34D+00 0.22D+00 0.38D+01 0.33D+01 0.30D+01 0.33D+01 0.55D+00 0.74D+00 -0.17D-01 -0.15D-01 0.63D-01 0.94D-01 0.72D-01 0.93D-01 0.42D-01 0.70D-01 -0.30D-01 -0.23D-01 -0.70D-01 0.50D-01 -0.55D-01 0.59D-01 ( 1.81) ( 1.50)

-0.12D+01 -0.30D+05 -0.24D+05 -0.45D+04 0.13D+03 -0.10D+00 -0.11D+00 -0.67D-01 0.48D-01 -0.30D+00 -0.72D+00 (-30.39) EL1

12

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11. Car only trip time TPVPVP (Quasi-dummy) -----BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA Not transit pass holder NABONTC (Dummy) ======= BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.65D+00 0.87D+00 0.88D+00 0.19D+00 -0.40D-02 0.75D+00 0.74D+00 0.56D+00 -0.18D+00 0.82D+00 0.82D+00 ( 39.32) EL1 -0.51D+00 -0.56D+01 -0.44D+01 -0.82D+00 0.25D-01 -0.93D-01 -0.11D+00 -0.63D-01 0.44D-01 -0.88D-01 -0.97D-01 ( -3.04)

-----------------------PO = PARKING AT NIGHT -----------------------First car curb paying (1,2) at Orig 1OV1 (Dummy) ==== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.37D-01 -0.55D+00 -0.56D+00 -0.12D+00 0.25D-02 -0.16D-01 -0.15D-01 -0.12D-01 0.38D-02 0.14D-01 0.20D-01 ( -0.10)

First car curb free (3) at Origin 2OV1 (Dummy) ==== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.52D-02 0.79D-01 0.79D-01 0.18D-01 -0.36D-03 0.22D-02 0.22D-02 0.17D-02 -0.54D-03 0.40D-01 0.67D-01 ( 0.08)

13

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11. First car public free (8,9) at Orig 4OV1 (Dummy) ==== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.23D-01 -0.35D+00 -0.35D+00 -0.78D-01 0.16D-02 -0.99D-02 -0.98D-02 -0.75D-02 0.24D-02 0.24D-01 0.25D-01 ( -0.06)

First car public paying (10,11) at 5OV1 (Dummy) ==== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.21D+00 -0.32D+01 -0.32D+01 -0.72D+00 0.15D-01 -0.91D-01 -0.90D-01 -0.68D-01 0.22D-01 -0.22D-01 -0.15D-01 ( -0.57)

----------------------PD = PARKING AT WORK ----------------------Parking reserved at work Destinatio SResD (Dummy) ===== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.47D-01 0.70D+00 0.71D+00 0.16D+00 -0.32D-02 0.20D-01 0.20D-01 0.15D-01 -0.48D-02 0.79D-01 0.79D-01 ( 0.63)

Curb paid (2,3) at Dest. 1DStat (Dummy) ====== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.45D+00 0.68D+01 0.68D+01 0.15D+01 -0.31D-01 0.19D+00 0.19D+00 0.14D+00 -0.46D-01 0.17D-01 0.40D-01 ( 2.03)

14

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11. Curb free (4,5) at Dest. 2DStat (Dummy) ====== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.35D-01 0.53D+00 0.54D+00 0.12D+00 -0.24D-02 0.15D-01 0.15D-01 0.11D-01 -0.36D-02 -0.11D+00 -0.11D+00 ( 0.40)

Public location free (12,13) at Des 4DStat (Dummy) ====== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.56D-01 0.84D+00 0.84D+00 0.19D+00 -0.38D-02 0.24D-01 0.23D-01 0.18D-01 -0.57D-02 0.22D-01 0.17D-01 ( 0.48)

Public location paying (14,15) at D 5DStat (Dummy) ====== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.15D-01 -0.22D+00 -0.22D+00 -0.50D-01 0.10D-02 -0.63D-02 -0.62D-02 -0.47D-02 0.15D-02 0.90D-01 0.78D-01 ( -0.04)

--------------------F = FAMILY STATUS --------------------Partner NP2 (Dummy) === BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.55D-01 0.27D-01 0.60D+00 0.41D+00 0.48D+00 0.42D+00 0.89D-01 0.92D-01 -0.27D-02 -0.19D-02 0.10D-01 0.12D-01 0.12D-01 0.12D-01 0.68D-02 0.88D-02 -0.48D-02 -0.28D-02 0.24D-02 0.28D-01 0.60D-02 0.16D-01 ( 0.47) ( 0.40)

15

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11. Child NP3 (Dummy) === BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.41D+00 0.68D-01 0.45D+01 0.10D+01 0.36D+01 0.10D+01 0.67D+00 0.23D+00 -0.20D-01 -0.47D-02 0.76D-01 0.29D-01 0.87D-01 0.29D-01 0.51D-01 0.22D-01 -0.36D-01 -0.70D-02 0.64D-01 0.61D-01 0.62D-01 0.66D-01 ( 1.25) ( 0.26)

Previous generation NP4 (Dummy) === BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.65D-01 0.71D+00 0.57D+00 0.11D+00 -0.32D-02 0.12D-01 0.14D-01 0.81D-02 -0.57D-02 0.40D-01 0.31D-01 ( 0.19)

-0.67D+00 -0.10D+02 -0.10D+02 -0.23D+01 0.46D-01 -0.29D+00 -0.28D+00 -0.21D+00 0.69D-01 -0.39D-01 -0.49D-01 ( -0.32)

AGE AGE BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.14D-01 0.15D+00 0.12D+00 0.22D-01 -0.67D-03 0.10D+00 0.12D+00 0.69D-01 -0.49D-01 0.14D-01 0.12D-01 ( 3.24)

-0.11D-02 -0.17D-01 -0.17D-01 -0.39D-02 0.79D-04 -0.21D-01 -0.21D-01 -0.16D-01 0.50D-02 -0.16D-01 -0.32D-01 ( -0.43)

2 Tradesperson, commerc., firm mana CSP2 (Dummy) ==== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.80D+00 -0.88D+01 -0.70D+01 -0.13D+01 0.39D-01 -0.15D+00 -0.17D+00 -0.99D-01 0.70D-01 -0.32D-01 -0.30D-01 ( -1.02)

-0.58D-02 -0.87D-01 -0.88D-01 -0.20D-01 0.40D-03 -0.25D-02 -0.24D-02 -0.19D-02 0.60D-03 0.30D-01 0.36D-01 ( -0.01)

3 Management, higher professional CSP3 (Dummy) ==== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.18D+00 0.36D-01 0.19D+01 0.54D+00 0.15D+01 0.55D+00 0.28D+00 0.12D+00 -0.85D-02 -0.25D-02 0.32D-01 0.15D-01 0.37D-01 0.15D-01 0.22D-01 0.12D-01 -0.15D-01 -0.37D-02 -0.16D+00 0.97D-01 -0.16D+00 0.11D+00 ( 1.25) ( 0.43)

16

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11. 4 Intermediate professional CSP4 (Dummy) ==== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.76D-01 0.83D+00 0.66D+00 0.12D+00 -0.37D-02 0.14D-01 0.16D-01 0.94D-02 -0.66D-02 0.47D-01 0.46D-01 ( 0.71)

-0.85D-02 -0.13D+00 -0.13D+00 -0.29D-01 0.59D-03 -0.36D-02 -0.36D-02 -0.27D-02 0.88D-03 -0.64D-01 -0.66D-01 ( -0.14)

6 Worker CSP6 (Dummy) ==== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.39D+00 -0.43D+01 -0.34D+01 -0.64D+00 0.19D-01 -0.72D-01 -0.83D-01 -0.49D-01 0.34D-01 0.36D-01 0.28D-01 ( -1.73)

0.16D+00 0.24D+01 0.25D+01 0.54D+00 -0.11D-01 0.69D-01 0.68D-01 0.52D-01 -0.17D-01 -0.22D-01 -0.29D-01 ( 1.20)

8 Other CSP8 (Dummy) ==== BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.85D-01 0.22D+00 -0.93D+00 0.33D+01 -0.74D+00 0.34D+01 -0.14D+00 0.74D+00 0.41D-02 -0.15D-01 -0.16D-01 0.95D-01 -0.18D-01 0.93D-01 -0.10D-01 0.71D-01 0.74D-02 -0.23D-01 -0.68D-02 0.98D-01 -0.48D-02 0.77D-01 ( -0.11) ( 0.00)

----------------F = HOUSEHOLD ----------------Number of persons in household MNP BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

0.81D-01 0.89D+00 0.71D+00 0.13D+00 -0.39D-02 0.37D-01 0.42D-01 0.25D-01 -0.18D-01 0.89D-01 0.81D-01 ( 2.04)

-0.23D-01 -0.35D+00 -0.35D+00 -0.78D-01 0.16D-02 -0.27D-01 -0.27D-01 -0.20D-01 0.65D-02 -0.33D-01 -0.44D-01 ( -0.95)

17

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11. Net income increasing level (1-10) ReNM1_10 (Quasi-dummy) -------BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.86D-01 -0.94D+00 -0.75D+00 -0.14D+00 0.42D-02 -0.10D+00 -0.12D+00 -0.69D-01 0.49D-01 -0.52D-01 -0.52D-01 ( -3.31)

-0.22D-01 -0.33D+00 -0.33D+00 -0.74D-01 0.15D-02 -0.67D-01 -0.66D-01 -0.50D-01 0.16D-01 0.66D-01 0.61D-01 ( -1.32)

Income unknown or other (11-12) ReNMetc (Dummy) ======= BETA coefficient Derivative of Y (sample value) Derivative of E(Y) Derivative of SIGMA(Y) Derivative of GAMMA(Y) Elasticity of Y (sample value) Elasticity of E(Y) Elasticity of SIGMA(Y) Elasticity of GAMMA(Y) Correlation (Y,X_k) original units Correlation (Y,X_k) Box-Cox transf. Conditional t-statistic for BETA

-0.98D+00 -0.11D+02 -0.86D+01 -0.16D+01 0.48D-01 -0.18D+00 -0.21D+00 -0.12D+00 0.86D-01 -0.38D-01 -0.38D-01 ( -3.33)

-0.16D-02 -0.25D-01 -0.25D-01 -0.55D-02 0.11D-03 -0.70D-03 -0.70D-03 -0.53D-03 0.17D-03 -0.23D-01 -0.26D-01 ( -0.01)

0.12D+01 ( 2.81)

0.20D+01 ( 11.41)

----------------ETC =ET CETERA ----------------REGRESSION CONSTANT BETA coefficient Conditional t-statistic for BETA

constant

=================================================================== PART II. Parameters t-statistic unconditional (=0) [=1] Model type L-1.6 L-1.6 Name of the variant DUREE DUREE Version number of the variant 31 35 Dependent variable in the variant DUREE DUREE =================================================================== Box-Cox transformations (estimated) ----------------------------------Lambda(y) ELY 0.415 0.239 ( 14.07) ( 5.31) [ -19.8] [ -17.0] Lambda(x) - group 1

EL1

0.097 ( 7.93) [ -73.7]

0.288 ( 4.09) [ -10.1]

18

Detailed econometric results found in Appendix 1 of: Gaudry, M. (2016). The demand for journey duration and reliability: Paris Region work trips by mode and sex, 2010-2011. Publication AJD 154, Agora Jules Dupuit, Université de Montréal. Jan. 11. =================================================================== PART III. General statistics Model type L-1.6 L-1.6 Name of the variant DUREE DUREE Version number of the variant 31 35 Dependent variable in the variant DUREE DUREE =================================================================== Log-likelihood -4909.07 -3008.27 Degrees of freedom

23

31

Pearson R2 Pearson R2 adjusted for Degrees of freedom

0.518 0.508

0.691 0.679

Pseudo-(L)-R2 Pseudo-(L)-R2 adjusted for Degrees of freedom

0.529 0.520

0.688 0.676

Average probability (Y=limit observation)

0.000

0.000

- Number of observations

2006

2006

Estimation - Number of observations - First observation - Last observation

1180 1 1180

826 1181 2006

21 1

29 1

0 0 1

0 0 1

0 1

0 1

0 0

0 0

0 0

0 0

0

0

0 24

0 32

Mean of observed Y Standard error of observed Y Skewness of observed Y

0.60D+02 0.24D+02 0.75D+00

0.35D+02 0.19D+02 0.14D+01

Mean of Y, estimated at the mean Standard error of Y, estimated at the mean Skewness of Y, estimated at the mean

0.42D+02 0.13D+02 0.56D+00

0.36D+02 0.10D+02 0.67D+00

Mean of estimated E(Y) Standard error of estimated E(Y) Skewness of estimated E(Y)

0.60D+02 0.17D+02 0.84D-01

0.35D+02 0.16D+02 0.13D+01

0.54D+01 0.19D+00 -0.18D+03 -0.56D-02 -0.33D+02 -0.30D-01

0.45D+01 0.22D+00 -0.22D+03 -0.45D-02 -0.49D+02 -0.20D-01

Sample

Total number of fixed or estimated parameters: - Beta .Estimated .Constant - Lambda(y) .Fixed .Estimated .Constrained .Distinct - Lambda(x) .Fixed .Estimated - Heteroskedasticity Delta .Fixed .Estimated Lambda(z) .Fixed .Estimated - Autocorrelation Rho .Estimated - Total .Fixed .Estimated

M.R.S. between Measures M1, M2 and M3 M1 / M2 M2 / M1 M1 / M3 M3 / M1 M2 / M3 M3 / M2

Elasticity of substitution between M1, M2 and M3 M1 / M2 0.17D+01 0.13D+01 M2 / M1 0.59D+00 0.76D+00 M1 / M3 -0.24D+01 -0.41D+01 M3 / M1 -0.42D+00 -0.24D+00 M2 / M3 -0.14D+01 -0.31D+01 M3 / M2 -0.71D+00 -0.32D+00 ===================================================================

19